After decades of operating on the day-to-day transactional side of this industry as an agent and lender, I now enjoy a unique vantage point where the housing industry intersects — real estate, mortgage lending, quasi-governmental housing agencies, policymakers and nonprofit organizations, and, of course, the homebuyer. My observations over the past five years have reinforced some of my long-held beliefs while challenging and even altering others.

First, what hasn’t changed is my respect for real estate professionals who make an honest living in this crazy business. What has changed is my appreciation of how difficult it is for many people and organizations to shake outdated perceptions when opportunity calls.

Take, for example, the alarming drop in sales to first-time homebuyers. Student debt, the job market and the alleged desire by millennials to defer homeownership have all contributed to the downturn. But there’s much more at play.

Research data throughout 2014 proved beyond doubt that millions more millennials and boomerang buyers could afford a home than they themselves believed.

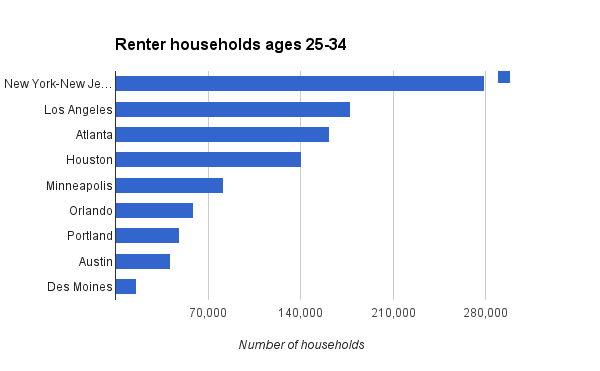

Our industry is not making the most of this grand opportunity. Here are the numbers of 25- to 34-year-old renter households who can afford a median-priced home in select markets, according to research by the Harvard Joint Center for Housing Studies and the American Community Survey at census.gov:

Now, consider that this same cohort is pessimistic about qualifying for a mortgage. Research by Zelman & Associates shows that 60 to 72 percent overestimate down payment requirements, believing that they need at least 11 to 15 percent of the sales price. In addition, 70 percent of U.S. adults are unaware that down payment help exists, according to a NeighborWorks America survey.

We know that there are billions of dollars in down payment help available across all markets. It’s not just for low-income households and low-cost homes. Households earning up to 120 percent or more of area median income can be eligible. Our data also show that more than 70 percent of all homes currently listed for sale are eligible for one or more programs. That includes large markets, small markets, high-cost, low-cost, coastal and inland.

Millions more people can become successful homeowners today — they simply don’t know they can or how to do it. I asked an executive at one of the major listing portals why they don’t share this type of information with the tens of millions of monthly visitors to their site. The answer: “Because they don’t ask for it.”

But how can you ask for help when you don’t know it exists?

Saving for a down payment has always been the No. 1 obstacle to homeownership, now so more than ever. (Please hold your “skin in the game” comments for a future column.)

This is a question for the entire industry — agents, brokers, lenders, homebuilders and their trade organizations. Remember the federal housing tax credit of 2009 and 2010? That program was wildly successful in large part because the National Association of Realtors, the Mortgage Bankers Association and the National Association of Home Builders used their substantial megaphones in harmony to educate and inform their members and the public. Today’s opportunities dwarf that program, but nary a peep.

Why, we’re frequently asked.

Why indeed?

There are significant challenges when it comes to affordability, but much more can be done with relative ease to educate homebuyers about their home financing options, including down payment programs. We’ll dig deeper throughout the year — provide commentary, pose solutions and highlight successful agents and best practices.

Rob Chrane is a former Realtor and broker with more than three decades of experience in real estate and mortgage finance. He is the president of Down Payment Resource.