Very few agents know how to explain the impact of soaring home prices, inflation and increasing interest rates on the consumer’s ability to purchase. Consumers feel the impact of rising prices, but don’t realize how it translates into dollars and cents and the cost of a home.

Your ability to explain the cost of waiting to transact can help you turn that reluctant buyer or seller into someone who is willing to buy or sell now. Here are the three key areas to cover.

Increased housing prices

According to The National Association of Realtors (NAR), the median existing-home price for all housing types in August was $356,700, up 14.9 percent from August 2020 ($310,400).

In a recent article, Zillow forecasted a 11.7 percent appreciation in home values for 2022. That’s on top of a 17.7 percent increase in prices over the last 12 months.

Reason No. 1 to transact now:

Since so many consumers follow Zillow, using these numbers can be very persuasive, especially if you frame it like this:

Agent: According to the most recent data from Zillow, a home that cost $300,000 in January of 2021, is now valued at $353,100. By the end of 2022, Zillow is predicting it will go up in value an additional 11.7 percent, placing its value $394,413.

Putting it a little differently, if Zillow’s prediction that property values will increase by 11.7 percent in 2022 is correct, the cost of waiting to purchase that median priced property will is $3,478 per month.

Increasing interest rates translate into less buying power for buyers

Assuming the interest rates increase by one percent, here are the two concerns to discuss with your clients:

- How much more they will pay in interest overall for the loan.

- How much more they will need to qualify at a higher interest rate as opposed to purchasing now.

Most agents have never discussed the impact of increased interest rates on their client’s ability to transact. The reason is simple: With the exception of a tick up in interest rates from July 2016 to October 2018, interest rates have steadily trended down since May of 2000, hitting an all-time low in December, 2020 of 2.67 percent.

That trend is about to be reversed. In their latest quarterly forecast, Freddie Mac economists project that 30-year fixed-rate loans will rise from a low of 2.67 percent to an average of 3.7 percent by the end of 2022.

While a one percent increase in interest rates doesn’t seem like much, the two charts below illustrate the real costs to the borrower.

As you can see from the arrows in the chart above, an interest rate increase from 2.7 percent to 3.7 percent results in additional interest payments ranging from $26,986 to $31,475 during the first 10 years of ownership. If the borrower stays in the property for 30 years, those numbers range from $55,595 to $66,019.

According to the U.S. Department of Housing and Urban Development (HUD), the national median income for 2021 is $79,900. Unless a borrower has 20 percent down, even at an interest rate of 2.7 percent, over half the borrowers would be unable to qualify for a median-priced property in today’s market.

The real problem: qualifying for the loan

In addition to the long-term extra interest costs outlined above, a more pressing problem for buyers is qualifying for the loan. The following chart illustrates the amount of income required on average to qualify for a median-priced home in the U.S.

(Please note, the income required to qualify includes one percent of the loan amount for PMI where applicable, an average of U.S. property tax rate of $2,471 plus an average of $1,312 for insurance, for a total of $3,783.)

If the rates increase to 3.7 percent as predicted, the amount needed to qualify for a median priced home increases by roughly 10 percent, yet wages and salaries for private industry workers only rose 4.3 percent (annualized) over the six-month period ending June 2021.

Reason No. 2 to transact now:

You have two options in terms of how you present this data to your clients. You can use the charts provided in today’s column or better yet, have your mortgage professional calculate the exact costs of waiting to purchase for your buyer.

Assuming a $356,700 purchase price with a 90 percent fixed-rate loan for 30 years, here’s how to explain this:

Agent: Currently, the best 30-year fixed mortgage rate available for your purchase is 2.625 percent. Interest rates for 2022 are predicted to increase by one percent to 3.7 percent. Assuming you stay in your home for 10 years before selling, purchasing with an interest rate of 3.7 percent means you will pay an extra $30,360 in interest.

Qualifying for a 3.7 percent loan also means you will have to show an extra $7,525 in annual income. Given that wages are only increasing at a rate of 4.3 percent, is that something you will be able to do a year from now?

Inflation rears its ugly head

Consumers are experiencing soaring prices everywhere. According to the Washington Post, meat, poultry, fish and eggs are up 15.7 percent, and gasoline prices have increased 43.9 percent on average from $2.274 per gallon in September 2020 to $3.272 per gallon in September 2021.

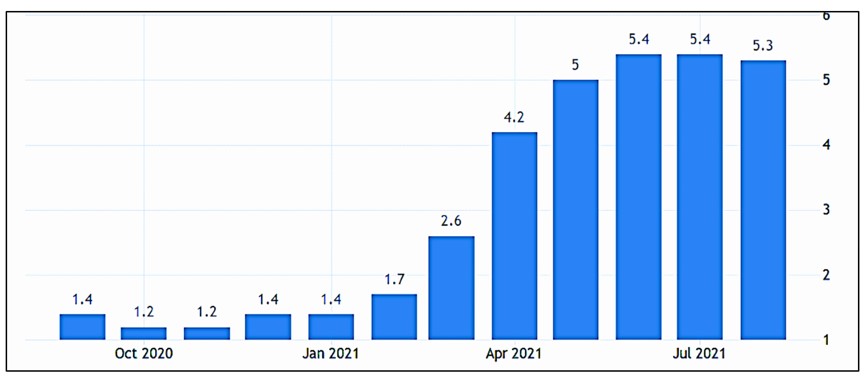

The overall inflation rate has increased from 1.2 percent in October 2020 to 5.3 percent today as indicated in the following chart:

Reason No. 3 to transact now:

Assume your client can afford a median priced home of $356,700 today. Based on the current 5.3 percent inflation rate, in October 2022, the buyer could only afford to purchase a home that cost $337,795.

In other words, the 5.3 percent inflation rate shrinks the buyer’s purchasing power on that property by $1,545.83 per month. Here’s how to explain the cost of waiting to your client:

Agent: It seems like the cost of everything is going up and up, not only for houses, but for food, gasoline, heating, cars, etc. The problem is when inflation drives prices up, it’s like having a tax on your income.

To illustrate how this works, assume you earn a $100,000 per year. With a 5.3 percent inflation rate, your $100,000 today will be worth $94,700 a year from now. Instead of being able to afford a $356,700 median priced house, you would only be able to afford a home that cost 5.3 percent less a year from now, i.e., $337,795.

In other words, the 5.3 percent inflation rate shrinks your ability to purchase that $356,700 home by $1,546 each month you wait to purchase.

The cost benefit of transacting now

Assuming a $356,700 price and using the data above, here’s the cost benefit to a buyer who purchases now rather than waiting a year to purchase.

- According to Zillow’s prediction of a 11.7 percent increase in home prices in 2022, the $356,700 home today will be valued at $398,434 a year from now, i.e., an increase of $41,374.

- If the buyer places 10 percent down and obtains a 90 percent fixed-rate mortgage at one point higher than today (2.7 percent to 3.7 percent) and stays in the property for 10 years, the buyer will pay $30,360 LESS in additional interest. They will also need $7,525 less to qualify for that loan.

- By transacting now rather than a year from now, the buyer can afford a $356,700 median priced home as opposed to only being able to afford a $337,795 priced home a year from now due to inflation. That’s $18,905 less than what the buyer can afford today.

- The grand total for transacting now as opposed to waiting: $41,373 + $30,360 + $18,905 = $90,638.

Shrinking the qualified buyer pool translates into lower prices for sellers as well

Due to the factors above, now may be the best possible time for homeowners to sell due to surging prices outpacing the growth of wages, the increased interest rates making it harder for buyers to qualify, plus the inflationary pressures shrinking the buying power of everyone’s dollars. Each of these factors reduces demand, which will eventually result in lower prices.

The bottom line is: We have already experienced a major uptick in both inflation and interest rates as compared to 2020. The probability is high there will be even more increases in the future. Familiarize yourself with the concepts in this article, and educate your clients about the financial benefits of transacting now as opposed to waiting.

While purchasing today may mean moving further away or compromising on what they want, the cost of waiting is so substantial it’s better to transact now. Moreover, even if prices go down, it seems highly unlikely that a house priced at $356,700 today would drop over $90,638 in price!

Bernice Ross, President and CEO of BrokerageUP and RealEstateCoach.com, is a national speaker, author and trainer with over 1,000 published articles. Learn about her broker/manager training programs designed for women, by women, at BrokerageUp.com and her new agent sales training at RealEstateCoach.com/newagent.