If you asked 53 real estate economists and analysts what they see in the future of the housing economy, what do you think they’d say?

Thankfully, you don’t have to guess; Urban Land Institute released its semi-annual Real Estate Consensus Forecast today.

Rental rates, home starts and prices

“The apartment sector has performed very well the past several years,” stated the report.

Vacancy rates were 7.1 percent in 2009; then they hit 4.6 percent in 2015 before bumping up to 4.9 percent last year.

They’re expected to grow in the next few years, hitting 5.2 percent this year, 5.3 percent in 2018 and 5.4 percent in 2019.

Forecasted rental rates have also been adjusted to lower than previously forecasted. Rental rate growth slowed in 2016; it grew 0.2 percent “after six straight years of growth over 3 percent,” according to the report.

In 2017, rental rate growth is expected to hit 2.0 percent and stay there in both 2018 and 2019.

What about that pesky problem everyone is talking about — low housing inventory?

Here’s some good news: There was more growth in housing starts for single-family housing (for the fifth straight year) in 2016, and growth is expected to continue, says ULI.

Economists expect growth to increase to 845,000 in 2017, 892,500 in 2018 and 920,000 in 2019. “The 2019 level brings starts to within 10 percent of the 20-year average for the first time since 2007,” stated the report.

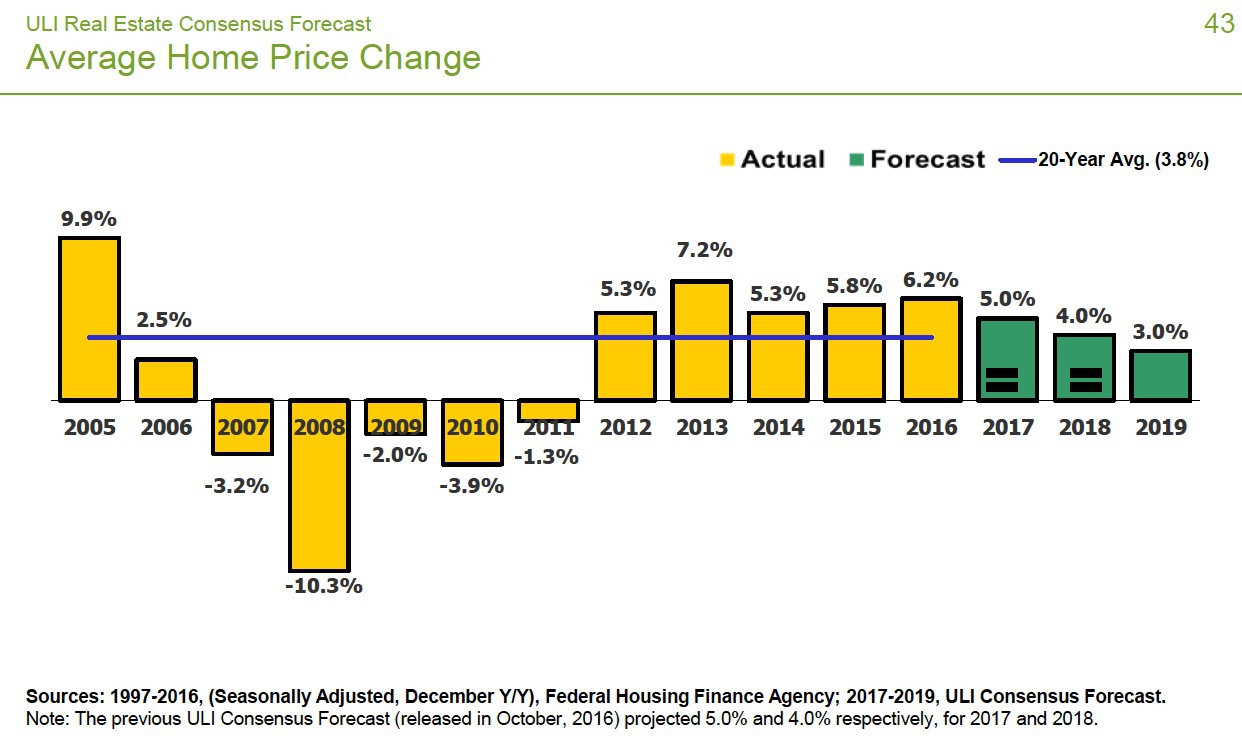

And of course, low inventory means higher prices. The Federal Housing Finance Agency (FHFA) estimates that existing home prices grew by 6.2 percent in 2016. That growth is expected to moderate to 5.0 percent in 2017, according to ULI, then 4.0 percent in 2018 and 3.0 percent in 2019.

The overall economy

In general, this outlook is more favorable than six months ago.

Economists expect gross domestic product (GDP), one measure of overall economic health, to grow over the next three years. However, continued decline in unemployment rates mean that employment growth and the employment rate will probably plateau “as the economy approaches full employment,” according to the report.

GDP growth in 2015 was 2.6 percent, but it was only 1.6 percent in 2016. The economists forecast GDP growth rates to increase to 2.3 percent this year, 2.6 percent in 2018 and then drop to 2.0 percent in 2019.

Unemployment is expected to reach 4.6 percent by the end of this year and 4.5 percent by 2018. Economists expect it to shift back up to 4.6 percent by the end of 2019.

Employment growth is expected to continue at 2.20 million jobs this year, 1.90 million jobs in 2018 and 1.55 million jobs in 2019.

So the economy will be ticking along, and people will have jobs while homes are being built and price growth is moderating somewhat. How does that translate to homeownership?

Those darn millennials

It’s probably not news that people are concerned about the millennial homeownership rate. The homeownership rate has fallen among all age groups, but for Americans ages 20 to 29, it’s gone from a historically “normal” 30 percent to a measly 20 percent.

Moderator Timothy Savage, senior managing economist at CBRE Econometric Advisors, asked a panel of experts: What would happen if that rate returned to normal historic levels? Would there be an exodus from the cities — is multifamily housing overbuilt?

“No, not yet,” opined Melissa Reagen, head of real estate and agricultural research at MetLife. “We continue to have pretty strong renter demand.”

However, she emphasized the yet, noting that in a few years when marriage and procreation becomes a looming reality for this age group, they will probably want to leave their apartments.

She added that in some classes, there is a very strong case of undersupply. “Not everyone can afford a luxury apartment,” she noted.

Focusing on homeownership rates at all when it comes to millennials is a mistake, said K.C. Conway, senior vice president of credit risk management at SunTrust Banks. “This is a generation that doesn’t seem to see the value proposition in homeownership, but that doesn’t mean they don’t occupy housing,” he pointed out. “We may see a generation that tends to rent more.”

In addition, their behaviors will likely affect what’s offered in housing in the future.

“I think we’ve overplayed” the idea that millennials don’t want to buy, countered Mary K. Ludgin, managing director at Heitman. “Reports are coming in that the turkey ‘doneness’ button has popped out and people are indeed taking the economic expedient — a home further out from the city.

“A lot of millennial behaviors are more about economic reality than they are actually indicative of preferences,” she added. And she doesn’t see a drop in occupancy or rental rates as millennials decide to buy — “the generation behind the millennials is the same size,” she noted, so demand will probably continue as this group ages into renting.

The forecast is “based on a survey of 53 real estate economists and analysts at 39 of the nation’s leading institutions,” according to ULI. Economists are asked about:

- GDP

- Employment

- Inflation

- Interest rates

- Capitalization rates

- CMBS issuance

- Property transaction volumes and price growth

- REIT returns

- Investment returns for four property types

- Vacancy/occupancy rates and rents for five property types

- Housing starts and price growth

Like me on Facebook! | Follow me on Twitter!