The double-whammy of rapid home price appreciation and rising mortgage rates has created affordability challenges for many homebuyers that’s prompting some sellers to adjust their price expectations. But that doesn’t mean home prices are set to decline, First American Chief Economist Mark Fleming said in an analysis published Friday.

Historically, rising mortgage rates “may take the steam out of rising house prices, but they don’t necessarily trigger a decline,” Fleming said in a blog post. “In today’s housing market, demand for homes continues to outpace supply, which is keeping the pressure on house prices, so don’t expect house prices to decline.”

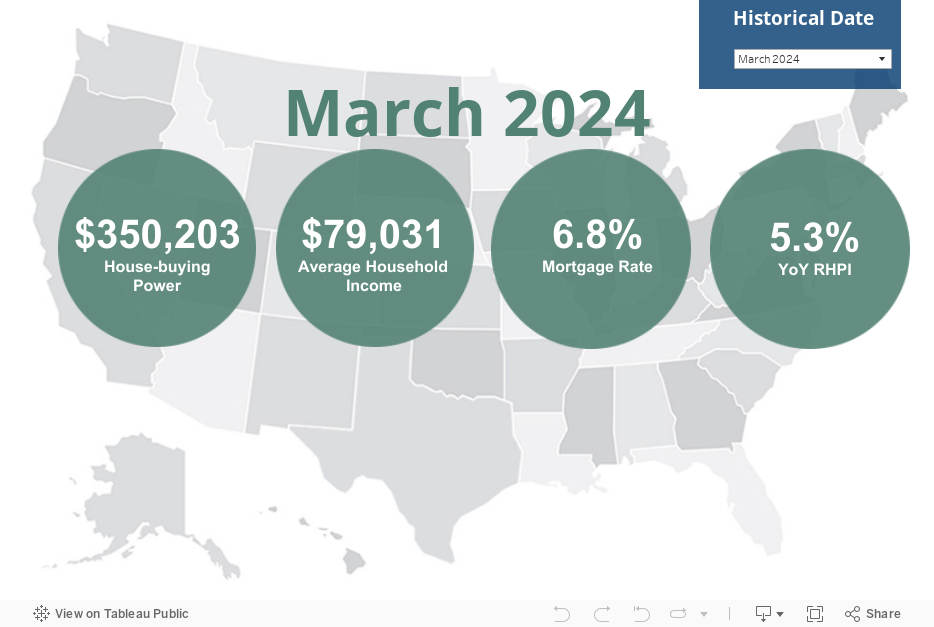

Fleming’s analysis notes that the First American Real House Price Index was up 32.5 percent in March. That’s the strongest annual growth in the history of the index, which adjusts for the impact of inflation when tracking home prices dating to 1990.

Not only were home prices up by a nominal 21.6 percent in March, but higher mortgage rates further eroded “house-buying power.” Even though average household income was up 4.9 percent from a year ago, to $70,961, higher mortgage rates meant “house-buying power” fell by 8.3 percent, to $421,463, First American estimated.

Those kinds of numbers have some people wondering if home prices are poised for a crash.

In March, researchers at the Federal Reserve Bank of Dallas who analyzed inflation-adjusted house prices relative to fundamentals like disposable income, rents and long-term interest rates said they found signs of a “brewing U.S. housing bubble.” Media coverage of that report got people talking, with Google searches for “housing bubble” spiking.

A new report from Redfin on Thursday found that 19 percent of sellers dropped their listing price during a four-week period ending May 22 — the largest share since October 2019.

But just because sellers are reducing their asking prices doesn’t mean home prices are beginning to drop. In their most recent forecast, economists at Fannie Mae said they expect national home price appreciation will decelerate, but remain in the double digits until next year.

Home price appreciation expected to trend down

Source: Fannie Mae housing forecast, May 2022.

However, if national home price appreciation does drop to 3.2 percent by the fourth quarter of 2023, as forecast, that “implies that some regions will likely experience price declines,” Fannie Mae economists said.

Fleming’s analysis looks at what impact rising mortgage rates have had on home prices in the past, and concludes that, “More often than not, house price appreciation has been resistant to rising mortgage rates.”

Exceptions include 1994, when house prices “declined slightly and briefly,” Fleming said, and the housing bubble of 2005-2006, which sent home prices in a tailspin in 2007 and 2008.

But in 1998-2000, as mortgage rates headed up during post-recession period “defined by tight labor markets, low inflation, and a higher minimum wage,” home prices appreciated by 14 percent. And home prices also kept going up as mortgage rates climbed from 2017 through 2018, Fleming noted.

“Rising mortgage rates do influence house prices, but broader economic conditions are often more influential,” Fleming said. “The Federal Reserve is purposely trying to slow the housing market in order to tame inflation, and early indications, based on our preliminary house price index, signal a normalizing housing market.”

Although this year’s runup in mortgage rates has been dramatic, there are signs that rates could be leveling off.

After rising more than two full percentage points this year — from 3.409 percent on Jan. 3 to a 2022 peak of 5.593 percent on May 6 — mortgage rates have been trending down. According to the Optimal Blue Mortgage Market Indices (OBMMI), rates on 30-year fixed rate mortgages have come down 31 basis points from their May 6 peak, falling to 5.286 percent Thursday. A basis point is one hundredth of a percent, meaning mortgage rates are down nearly one-third of a percentage point in the last three weeks.

Mortgage rates level off

Although the minutes of the Federal Open Market Committee’s most recent meeting suggest the Fed will implement at least two more 50 basis-point increases to the short-term federal funds rate this year, mortgage markets may already have priced those increases in.

The latest reading of a key inflation metric, the personal consumption expenditures (PCE) price index, suggests the tightening the Fed’s already undertaken this year may be helping tame inflation. The PCE price index rose by 6.3 percent in April, an improvement from the 6.6 percent reading in March and the first drop since November, 2020, the Commerce Department reported Friday.

Investors who buy mortgage-backed securities that fund most home loans can also take some comfort in the fact that so far, the Fed is not taking an aggressive stance in unloading more than $2.7 trillion in mortgage debt that it’s accumulated to help keep mortgage rates low.

Mortgage rates may have peaked

Source: Forecasts by Fannie Mae, the National Association of Realtors and the Mortgage Bankers Association.

While forecasters at the National Association of Realtors see rates continuing to inch up slightly in 2023, economists at Fannie Mae and the Mortgage Bankers Association are expecting mortgage rates to ease some next year.

Get Inman’s Extra Credit Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.