Are you set up for success in 2016? Join 2,500 real estate industry leaders Aug. 4-7, 2015, at Inman Connect in San Francisco. Get Connected with the people and ideas that will inspire you and take your business to new heights. Register today and save $100 with code Readers.

Reposted with permission from Smaulgld.

The homeownership rate is down.

New- and existing-home sales remain far below their 2005 peaks.

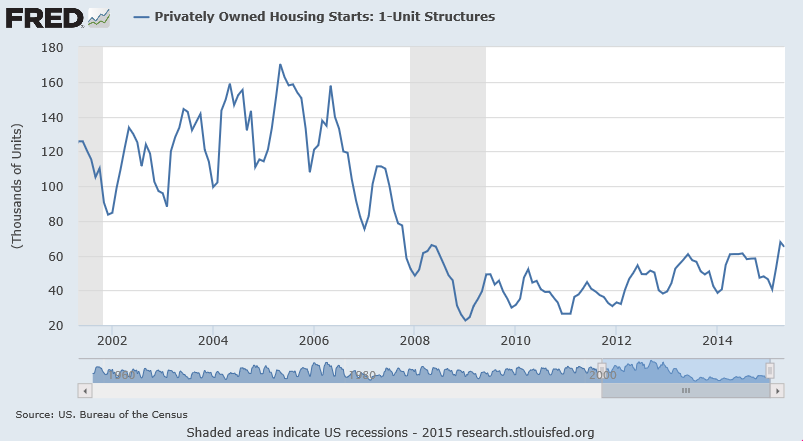

Housing starts for single-family homes are flat.

What went wrong?

For the past few years, the media has trumpeted a housing “recovery.” In the “False Housing Recovery of 2013” (and again in 2015), we noted that the recovery in housing was in price alone.

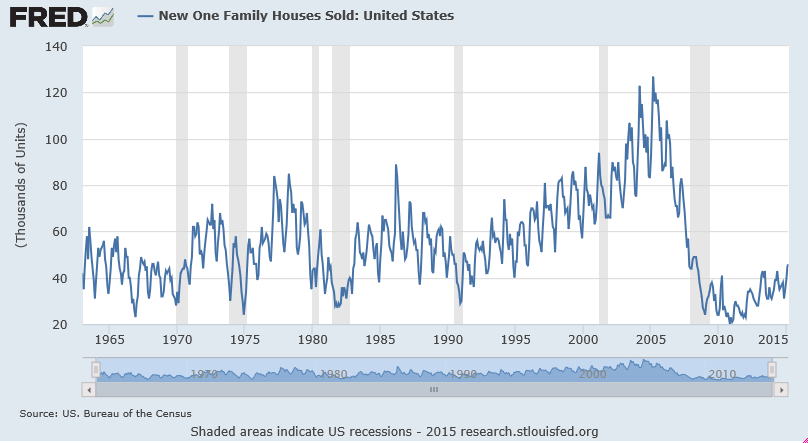

New-home sales and existing-home sales remain far below 2005 levels and are, indeed, at multi-decade lows.

New-home sales 1963-2015

New-home sales are at levels of the 1960s and ’70s, when the population of the United States was far lower.

Higher home prices may have lifted underwater homeowners into positive territory and made them feel richer and more confident about their economic circumstances, but there is a dark side to rising home prices:

1. Rising home prices make homes less affordable.

The Federal Reserve’s policy of artificially driving down interest rates to boost housing prices has had the unintended (but predictable) consequence of shutting out a good portion of millennials from homeownership. Through a zero interest rate policy (ZIRP) and a six-year quantitative easing (QE) program that involved printing $4.3 trillion out of thin air in order to purchase billions of dollars of mortgage-backed securities and U.S. Treasury bonds, interest rates were driven down and home prices driven higher.

The misguided goal of a policy designed to get home prices back to the bubble levels of 2005 and 2006 with ZIRP and QE has backfired by increasing home prices and lowering home sales.

The Fed’s goal of higher home prices has been achieved in many areas around the country. Indeed, in cities like San Francisco and New York City, home prices have exceeded their 2005-2006 peaks.

2. Generation Y = Gen Rent.

Household formation among millennials remains low. Many real estate cheerleaders projected a day in the not-too-distant future when millennials in their million hordes would emerge from their parents’ basements, form households and start buying homes.

It hasn’t happened.

Instead, many are emerging from their parents’ basements, forming households and … renting.

As a result of millennials not buying homes at the same rate as baby boomers, the homeownership rate has declined.

Homeownership rate 2001-2015

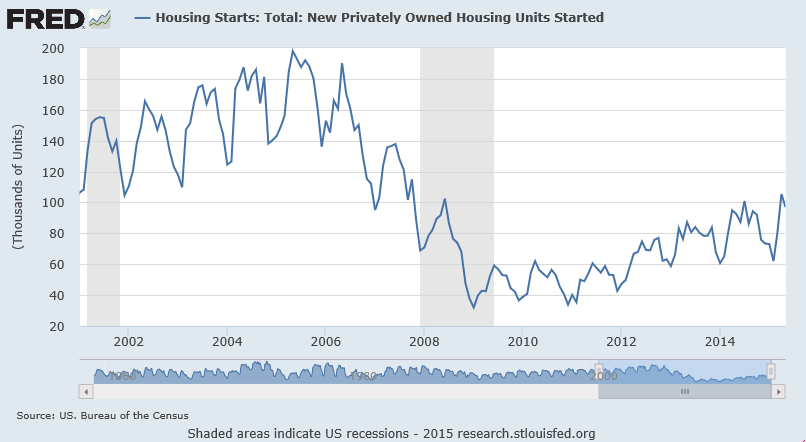

New housing starts 2001-2015

The June 2015 U.S. housing start data showed a 9.8 percent increase.

New single-family housing starts 2001-2015

New single-family home starts, however, have not participated in the upswing.

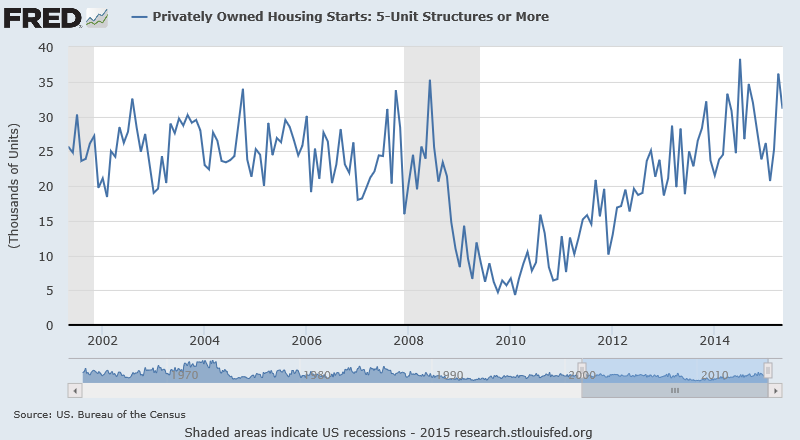

New rental unit housing starts 2001-2015

Nearly all of the growth in new home starts has come in housing with five units or more, reflecting the surging demand for rental housing.

Rental housing starts have rebounded nicely since the end of the Great Recession.

Perhaps the next generation of homebuyers will have better luck than millennials.

Louis Cammarosano is the author of Smaulgld, a blog that provides finance, economics and real estate market analysis, and marketing strategies and tips for real estate professionals.