This post has been republished with permission from Divvy Homes.

At Inman Connect New York, I spent some time chatting with Inman founder Brad Inman about how the real estate tech industry is evolving.

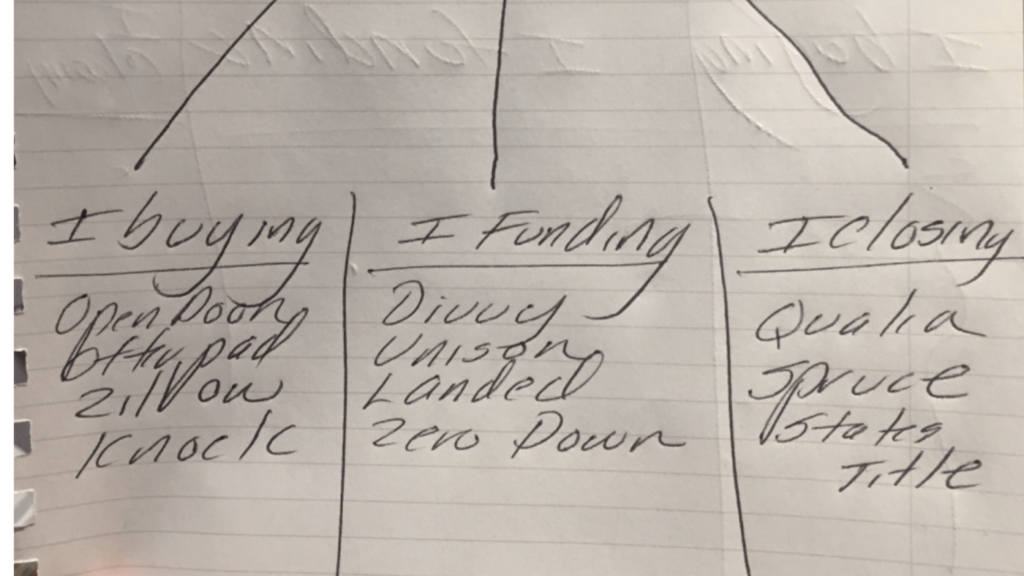

We spoke about how fix-and-flip companies have come to define the “iBuying” category and how that same evolution will occur for broad areas within real estate.

Brad coined the term “iFunding” for companies who put up capital to help people become homeowners, and together we broke down the industry into three sectors, as shown above in our very scrappy drawing: iBuying, iFunding and iClosing.

In this post, I explain what an iFunder is, what iFunding means and what its implications are for consumers, homebuyers and the industry as a whole.

What’s the problem?

Over the last decade, buying a home has gotten increasingly difficult. More and more people are being shut out from the dream of homeownership.

In response, innovative companies have created new ways to help fund a home purchase for people who are underserved or shut out by the traditional mortgage industry.

The new companies behind these innovative ways to help fund a home purchase can collectively be referred to as the iFunding industry.

As CEO of Divvy Homes, one of the leading players in this emerging industry, I believe these new home financing options will result in more options for consumers and an expansion of homeownership across the country.

What is iFunding?

An “iFunder” or “iFunding company” uses technology and data science to create a new model of home funding beyond the traditional mortgage model.

These companies fund home purchases in tandem with — or on behalf of — consumers.

In most cases, these new business models align the companies’ interests with those of their customers. This results in the customer getting some of the benefits of homeownership, such as building equity savings, enjoying price appreciation and having the freedom to use the space as they see fit.

It also leads to better returns for the company.

In practice, iFunding can take many forms:

- Shared equity investment: Companies provide downpayment funding to homebuyers and share in the appreciation of the home. No interest or monthly payment is paid by the consumer; instead, when the home is sold or the investment is cashed out the company receives a share of the proceeds.

- Empowered rent-to-own: Companies purchase homes on behalf of consumers who then build up equity savings with monthly payments while living in the home. The equity savings can later be used to buy back the home. A downpayment may also be required, which can later go toward the purchase of the home. The company charges market rent in addition to the monthly equity savings payments.

- Home trade-in with cash offer: Companies float financing for consumers who are preparing to sell their old home. The consumer uses the company’s financing to put in a cash offer on their new home, rather than waiting for the sale of the old home. The company charges a fee similar to a traditional real estate agent commission.

Why was iFunding created?

Buying a home has been part of the American dream for decades.

It has served as a primary wealth-building tool for millions of families who’ve seen appreciation of their home increase their net worth. In fact, a 2016 Harvard University study found that for most households, homeownership was associated with significant gains in household wealth — among the homeowners in the study, the median gain in wealth was $91,900 over 14 years.

Urban planners and local officials also view homeownership as a positive factor in building strong, stable communities. According to a report by realtor.com, homeowners are far less likely to move, while also being more likely to vote in local elections and volunteer in the community. Even today, when homeownership rates are down, most young people still want to buy a home. A survey by ApartmentList found that 9 out of 10 millennial renters dream of becoming homeowners.

The problem is that the financial hurdles to homeownership have become too high for many consumers to overcome. In the wake of the 2008 global financial crisis, many lenders tightened their criteria for approving mortgage loans, meaning that borrowers with less-than-stellar credit scores would often be rejected.

One of the reasons I leapt at the challenge of starting Divvy Homes is that I know how poorly the traditional mortgage industry serves Americans who’ve faced adversity and worked hard to overcome it.

I also know that housing prices and rents in most major metro areas have increased significantly, which has put pressure on consumers who try to save up for a down payment. As prices go up, a larger downpayment is required, but rental rates have also increased, making it harder for people to save.

Because iFunding is meant to solve some of the problems mentioned above, most of the companies in this new industry open up homeownership to a larger segment of the population by working with those who have lower credit scores and smaller downpayment savings.

With that said, different business models appeal to different types of customers. While some companies focus on higher-priced homes and customers with more savings, others focus on moderately priced homes and customers with little or no savings.

As the industry matures, these different business models will also evolve to better serve each segment of the population.

How does iFunding work for consumers?

From the perspective of a consumer, iFunding gives you more options than you otherwise would have had.

Here is an example from my company, Divvy Homes:

- Andrew and Heather want to buy a home in Atlanta, but their credit scores are not high enough.

- They partner with Divvy, which buys their preferred home for them.

The couple puts down a 2 percent down payment while Divvy takes care of all the other costs associated with the home purchase. - Soon after, they move into the home and get to enjoy it as if it was their own.

- Every month, they pay Divvy a monthly payment that includes rent and equity savings.

- After three years, they use their down payment and equity savings to buy back the home from Divvy at a previously agreed-upon price.

If all goes well, our customers get to live in their preferred home from the beginning of their partnership with us while strengthening their financial situation. When they buy back the home, they get to enjoy all the benefits of homeownership for the rest of their lives if they so choose.

Aspiring homeowners like Andrew and Heather are not the exception; they have come to be the norm in America.

Today, Divvy serves a wide variety of individuals: small business owners, 1099 workers, those with high student debt, individuals who recently changed jobs and more.

Is iFunding better than a traditional mortgage?

Mortgages in general are often a cheaper option than iFunding, but iFunding has several unique benefits, such as: serving a larger population than mortgages, empowering people to buy a home sooner, allowing for a very quick home close, bringing a more competitive offer and being more flexible than a mortgage on terms.

With that said, a mortgage will often be the best choice for those who qualify. And in the vast majority of cases, iFunding companies are not competing with traditional lenders but rather working alongside them to help consumers achieve their goal of homeownership.

At Divvy, we don’t see ourselves as a replacement to mortgages. We see Divvy as a bridge to a traditional mortgage. It’s important to us to work closely with established companies in the industry.

Other business models within the iFunding industry don’t replace mortgages either.

For example, with shared equity investments, the homebuyer typically uses the company’s financing to stack on top of their own down payment as they take out a mortgage to buy a home.

Ultimately, the relationship between iFunding and traditional mortgage companies in a transaction depends on the circumstances of the prospective homebuyers and their needs.

Will iFunding cause the next recession?

With the last recession, mortgage lenders gave out debt in a risky manner.

However, a key difference with iFunding companies is that they are sharing in the equity of a home, not issuing debt to customers. With Divvy, our company owns the home, and the renter is buying up equity — or investing in their savings.

We are not issuing them debt of any kind or taking mortgage foreclosure risk. This is a fundamental and important difference in the model, and this is shared by most other companies in the iFunding industry.

This post first appeared on Divvy’s website. It has been lightly edited for style.

Adena Hefets is the co-founder and CEO of Divvy Homes in San Francisco. Connect with her on Facebook or Instagram.