There’s an overwhelming amount of data and headlines circulating. This column is my attempt to make sense of it all for you, the real estate professional, from an overall economic standpoint.

Today, I am going to be taking about the June report on U.S. existing-home sales that was released by the National Association of Realtors last week. And I’m also going to give you the first view of my updated U.S. housing forecast for 2020.

So, let’s get straight to it.

Starting out with sales — the chart above shows the seasonally adjusted annual rate for transactions and, with a few exceptions in 2013 and 2016, the trend was positive. Well, it was, until COVID-19 hit.

You can see the massive drop in sales that occurred in April and May, but we saw an equally significant snap back in June with total sales rising to an annual rate of 4.72 million units — up from 3.91 million in May.

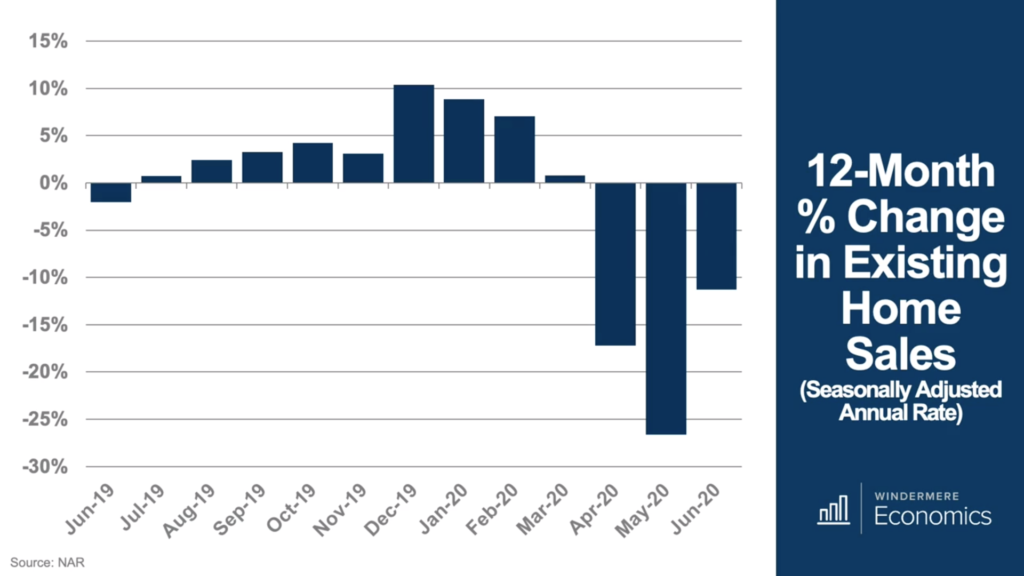

But it isn’t that easy to see here so let’s look at it in a slightly different way.

Above, you see same data, but I have tightened up the timeframe, and it shows the 12-month percentage change in the number of sales.

The market slowed significantly in March, and April and May were where we truly saw sales dry up. But take a look at the June number.

Can you see a V?

Annualized sales growth is still down by 11.3 percent, but it’s far better than it was. Month over month, we saw a 21 percent jump in sales — that’s the biggest monthly increase since NAR started collecting the data back in 1968.

And when we look at sales by price range, you can see the high-end market took a major hit in May, but there were significant drops across all price ranges.

But in June, the contraction was far less pronounced, and we actually saw transactions grow in that sweet spot between $250,000-$500,000, and we are also getting closer to seeing sales between $500,000-$750,000 turning positive, too.

Well, with the first half of the year behind us, I have now updated my forecast for existing-home sales in 2020, and you are the first to see it.

So, I guess that you can take this forecast in one of two ways. You can look at it and think we’re still going backward, or you can take the glass-half-full approach and realize that people are still buying and selling.

Of course, the second quarter was ugly with sales tracking at an annual rate of just over 4.3 million units, but it could have been much, much worse.

I believe that sales will continue to pick back up as we move though the second half of 2020, but they will still end up down by 6.4 percent from 2019 levels.

COVID-19 has impacted sales — the numbers don’t lie — however, what we need to consider is what the real reason for the drop in sales was. You can either believe that it’s a lack of demand with buyers not going ahead because they are worried about keeping their jobs or they are worried the economy will take longer to recover than is currently forecast.

Or you can believe that, though there was some pullback from the demand side of the equation, the biggest culprit was, and is, supply.

And if you’re thinking that it’s a supply side issue rather than a demand side problem, you’re right.

Twenty years of data shows current listing activity not just at a two-decade low, but at its lowest level in a generation. In June, there were just 1.5 million homes for sale in the U.S. And I looked back over data going back to 1999 and couldn’t find a single year with lower inventory levels in June than we saw last month.

Again, when we look at it a little differently, the 12-month change in listings shows a market that’s even tighter than we saw back in 2017 — and I remember you all moaning about how bad it was back then, but it’s even worse now.

Sales were hit because there were fewer buyers, yes, but of greater consequence is the fact that there was nothing to buy. But even with little choice, 510,000 homes closed in June — the greatest number of monthly closings since last August.

Now let’s take a look at sale prices — and what a difference a month makes. Sale prices dropped in April and May but bumped back in June. However, I really don’t like looking at price shifts on a monthly basis, as the data is simply too busy, so I concentrate on year-over-year price changes.

And as you can see, even though the pandemic, annual U.S. home price growth never turned negative, even if the monthly drop in May led to annual price growth coming in at its lowest level since we emerged from the housing recession in 2012. However, June did show a solid rebound — but at 3.5 percent, it’s still the lowest pace of price growth than we have seen in over a year.

And my current forecast for price appreciation in 2020, and I’m showing prices rising by 4.3 percent this year. And I will tell you the truth: When I ran the model and this number came out, even I was a little surprised at how high it was.

Of course, when this happens, the first thing that us economists do is to take a look at what others are saying. And when I looked at the most recent forecasts from other analysts, I was actually pleasantly surprised to see that they were pretty much in the same ballpark:

- NAR is saying 3.6 percent

- The Mortgage Bankers Association is at 4.9 percent

- Fannie Mae is at 5.2 percent

Now there was an outlier, CoreLogics, which is showing a 6-plus percent drop, but I just don’t see it.

Finally, I want to touch briefly on different product types.

And the chart below shows the breakout of listings by housing type, again looking at the year-over-year change, and what I found interesting was that we really didn’t see much improvement in the number of single-family homes for sale, but there was improvement in the multifamily arena.

Now, whether this is a function of COVID-19 concerns about living close to other people or just because most multifamily units are in denser, more urban markets is unclear. However, I will be watching to see if this is a trend that will continue, and I will be sure to report back to you if there’s anything interesting that happens.

Of course, nobody can deny that we are still in very unique times, and significant uncertainty remains, but housing is performing relatively well and, as I have said to you for the past few months, I stand by my position that housing will lead us out of the current economic contraction.

Sales will continue to recover in most markets and will only be held back because of a lack of supply.

Of course, there will be some who will say that we have yet to see a massive increase in foreclosed homes that is sure to happen.

But I am saying the same thing as I have over the past several months — that forbearance is working, and homeowners in forbearance who aren’t working now because of COVID-19-related layoffs will be back at work again before the term of their forbearance programs expires.

Matthew Gardner is the chief economist for Windermere Real Estate, the second largest regional real estate company in the nation.

Editor’s note: Fannie Mae and the Mortgage Bankers Association both upped their forecast numbers between the time the video published and this article. The article reflects the most current numbers at the time of publication.