There’s an overwhelming amount of data and headlines circulating. This column is my attempt to make sense of it all for you, the real estate professional, from an overall economic standpoint.

Almost exactly four months ago, the U.S. declared a national emergency because of COVID-19. So, I thought that now would be a good time to take a look at how the U.S. housing market has fared over the past 16 weeks and also let you know what you might expect to see as we move through the balance of the year.

So, let’s get straight to it. The charts in today’s video show the monthly and annual change in the number of homes for sale in America, and the data supports what I’m sure many of you are seeing in your respective markets — there’s nothing for sale.

You’ll see that total listing inventory was down by over 6 percent in June versus May, and it was off by 27.4 percent when compared to June of 2019. But what’s much more interesting is that “new” listings in June were up significantly versus May, though they were well below the level seen a year ago.

I’m sure some of you are scratching your heads and wondering how that can be. How can overall inventory be lower if new listings are that much higher?

Well, I’m afraid it can. Although we did see a lot of new listings coming online last month, they didn’t add to total inventory as these new homes simply sold too quickly!

And this makes one thing clear to me. Although the housing market is certainly not back to normal, we are definitely seeing some “green shoots,” with sellers starting to, albeit slowly, return to the market.

Now, we all know that a lot of people held off listing their homes when the pandemic hit and that many are still sidelined. But these numbers suggest that some sellers are feeling a little more confident, and I think that it’s becoming more likely that we’ll see more homes come online as economies across the nation continue to reopen.

But … (you know there’s always a but, right?)

But that said, we also know that infection rates are rising dramatically in several areas across the nation, and owners in those markets may delay selling. So, a broad resurgence of listing activity across the whole of the country is certainly not guaranteed.

And if you are wondering which markets I’m worried about, well, I’m keeping a close eye on several in Florida, Arizona, Idaho, Georgia, California and Tennessee.

But on a brighter note, there are some markets that have seen significant increases in the number of homes for sale. Here, I’m specifically thinking about Honolulu, San Francisco and San Jose, as well as Denver and Colorado Springs.

How did limited inventory affect list prices?

So, we know that supply remains tight. Now, let’s look at what effect limited inventory has had on list prices.

The numbers here are not surprising. When the pandemic hit in mid-March, the effects were seen in the April numbers with the annual change in median list price registering its lowest rate of growth since the burst of the housing bubble. And you will also see that there was essentially no increase in list prices when compared to prior month.

Well that was then, and this is now. You will also see that we snapped back in May. I would tell you that the pace of increase we saw in June represented the largest month-over-month increase in list prices that the country has seen in over a year.

What about the demand side of the equation?

Inventory levels are tight, and that’s driving list prices higher — really a rather simple supply-demand imbalance. Let’s take a look at that demand side of the equation.

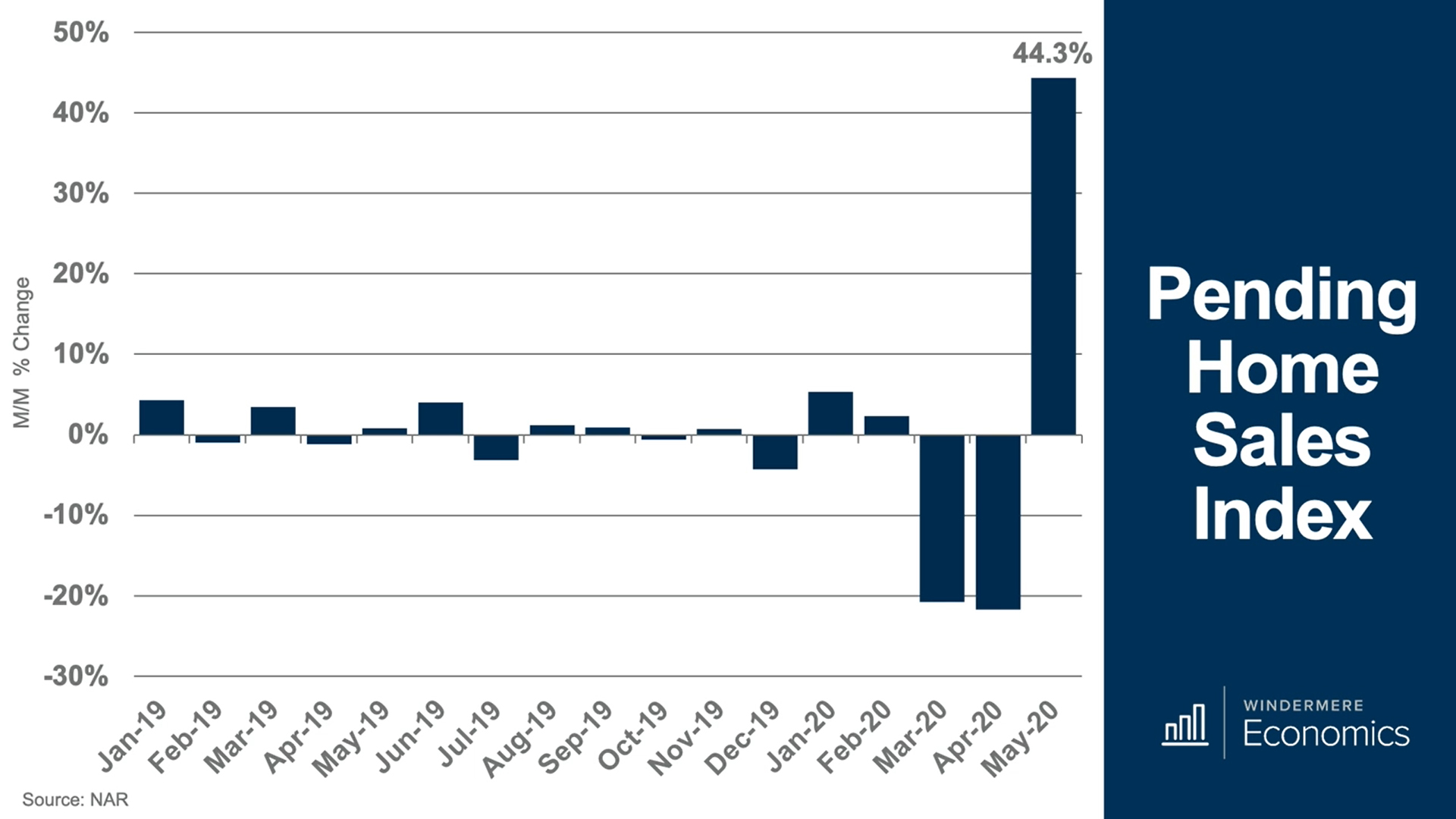

Here, the Pending Home Sales Index pretty much tells you all you need to know. Newly agreed contracts to buy homes tanked in March and April (again, no surprise), but look at the extraordinary bounce-back in May.

Now, I saw this jump and took a look back through the data and couldn’t find a single month in almost 20 years that had a larger month-over-month increase. Demand is back.

So, with list prices picking back up, it’s very reasonable to believe that this will lead to sale prices rising as well.

Unfortunately, we don’t yet have the June numbers yet, but the chart below shows the annual growth in home prices through May.

We can see that May’s increases were pretty small. In fact, at 2.3 percent, it was the smallest annual price increase since early 2012 and, on a month-over-month basis, prices actually dropped by 0.7 percent relative to April.

The monthly drop in sale price was a COVID-19-induced anomaly. I’ll tell you that raw sales price data that I’ve seen suggests that June will show a turnaround with sale prices rising again, albeit modestly.

Also, I’m still optimistic that sale prices in 2020 will be higher than seen in 2019, but it’s likely that the increase will be the smallest seen since U.S. home prices turned positive in 2012, following the housing bubble burst.

Now, I will say that there are other economists out there who are forecasting U.S. home prices dropping, and you may wonder why I’m less pessimistic.

Of course, as an economist it’s not in my DNA to have just one reason for anything, but if I were forced to give just one reason for my optimism, it would be these two words: mortgage rates.

If we can find any positives at all coming out of the COVID-19 pandemic, it’s that it caused mortgage rates to tumble — so much so that rates are breaking record lows on an almost weekly, if not daily, basis. And, believe it or not, that’s not too surprising.

As you all know, mortgage rates tend to track lower with bad economic news, and they tend to rise when the outlook is good.

Although we have seen some good economic numbers recently — particularly the June jobs report — it’s not enough to offset concerns over rising COVID-19 infection rates, and I would say that, until new infections start to tangibly drop in every state, it’s likely that mortgage rates will remain extremely low. This will benefit the housing market and allow home prices to continue to rise.

The final thing that I would like to bring up is forbearance

The positive news here is that the number of homes in the forbearance program is stable. We actually saw 105,000 homes coming out of forbearance in the most recent weekly survey.

The forbearance program is performing, and you should also know that most owners currently in forbearance can extend it beyond the initial three-month period. So, I don’t expect to see any sort of significant jump in foreclosures in the second half of this year as has been suggested by some forecasters

So there you have it. We are exactly 120 days into this pandemic and, as much as there were some who fully anticipated that the U.S. housing market would have collapsed already, it simply hasn’t happened — and won’t happen.

Of course, we are still in very unusual times, and the timing of any return to normal — whatever normal might look like — remains very uncertain, but I stand by my theory that housing will be a leader, and not a laggard, as we move through the balance of this year and into 2021.

To get the big picture including all of the data, watch the full video above.

Matthew Gardner is the chief economist for Windermere Real Estate, the second largest regional real estate company in the nation. Listen to him speak at Inman Connect Now.