The median home sale price soared 11 percent year over year during the week ending July 26, bringing that figure up to a record-high of $315,000, according to a market report issued by Redfin. The price jump also marks the largest annual increase in median sale price since 2014.

The significant price growth can be attributed to strong homebuyer demand, which is up 27 percent from pre-pandemic levels in January and February, according to Redfin’s seasonally adjusted homebuyer demand index. Prices have seen a rise as homebuyers compete for limited inventory, with new listings down 0.7 percent year over year and active inventory down 30 percent as of the four weeks ending July 26.

Buyer competition has also been reflected in the median sale-to-list price ratio, which rose to 99 percent — its highest point in at least six years.

“One of the first things I have to do with many of my buyers here in Houston is educate them on the reality that most houses are selling for more than asking,” Houston Redfin agent Melanie Miller said in Redfin’s report. “You can’t wait around for a price drop. Rather, homes that are priced right are receiving offers at or above full price within three days of being listed, so serious buyers need to be ready to act quickly.”

Sellers’ hesitancy seems to have left more cautious homebuyers wondering if they should wait for a more plentiful market with less competition, but it’s unclear when that time may arrive.

“The shortage of homes for sale makes people think, ‘Maybe I should wait until things get cooler,’ but unless we start to see a huge surge of new listings, things aren’t going to cool down much,” Salt Lake City Redfin agent Campbell Dosch said in the report. “Even new construction is selling out faster than it is being built. The shortage has extended into rentals too. A lot of people are living with family and friends now because it’s too hard to enter the market.”

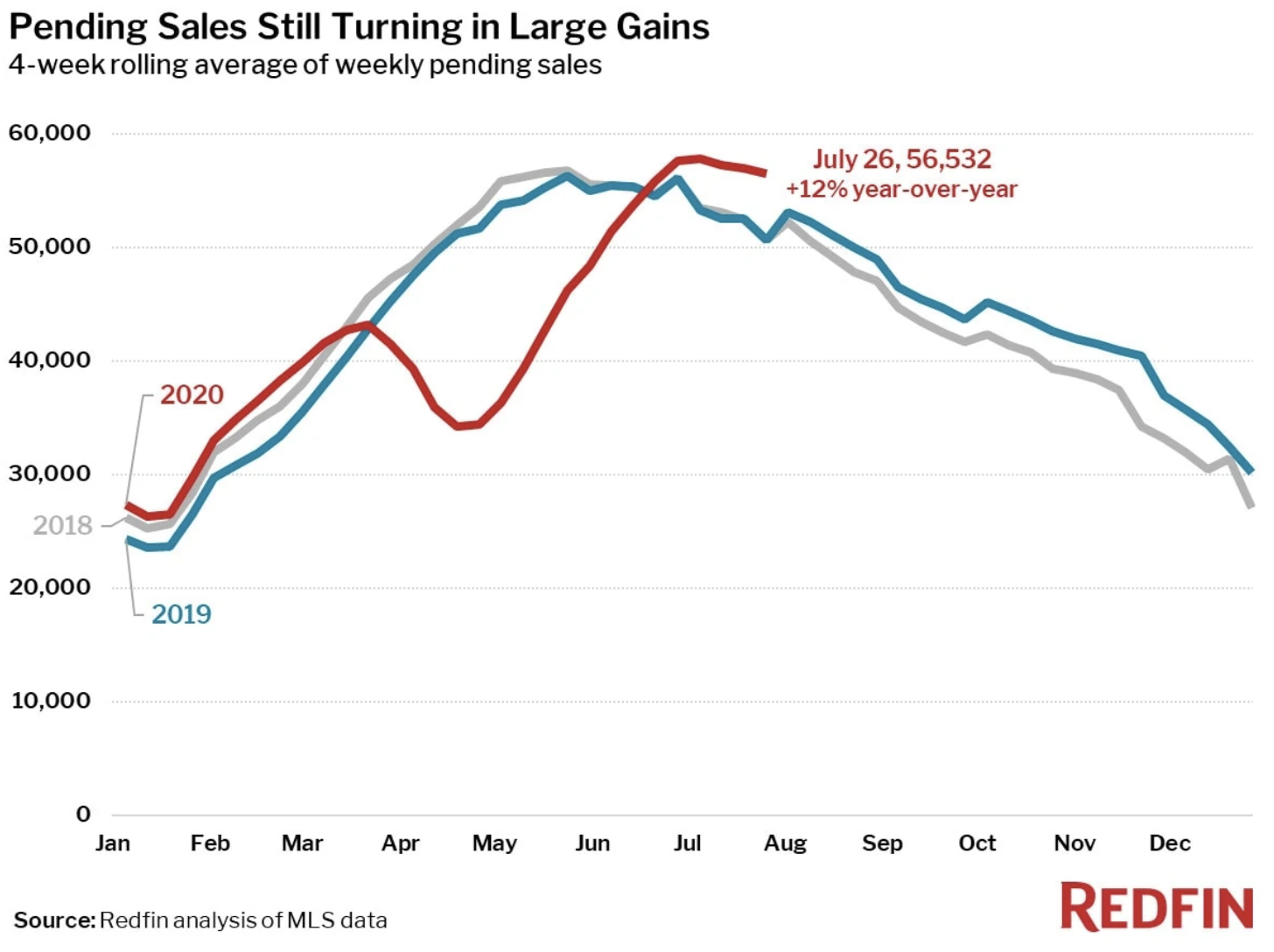

Many buyers have not yet been deterred by low inventory, though, as pending home sales were up 12 percent year over year during the four weeks ending July 26. However, Redfin reports that pending sales have gradually slowed on a weekly basis over the past three weeks, signaling that those figures may have peaked in early July. Pending sales are now about 2 percent lower than they were for the week ending July 5.

Although the housing market has stayed relatively strong over the past few months, now that we’ve hit August and unemployment benefits through the CARES Act have expired with no current plan in place to reinstate them, the financial status of many renters and homeowners may be much more uncertain, a fact that may soon impact the market.

“The economic pain of the pandemic has so far mostly been borne by those with lower incomes who were not as likely to be participating in the for-sale housing market,” Daryl Fairweather, chief economist at Redfin, said in a statement. “However, the expanded unemployment benefits being given to these workers has helped to keep the overall economy on stronger footing during a very uncertain time.”