Reposted with permission from Mike DelPrete.

Part 1 of this series took a detailed look at Compass’ growth strategies, while part 2 examined if Compass is a tech company or a traditional brokerage. Irrespective of the answer, Compass unquestionably needs to be a technology company — both to support its massive valuation and to be a sustainable business.

Is Compass worth $4.4 billion, and is it being valued as a traditional brokerage or a technology company?

Valuation overview

Compass has raised over $1.1 billion in venture capital, starting with $8 million back in 2012. Its latest $400 million round in September 2018 valued the company at $4.4 billion, up from $2.2 billion in December of 2017. Compass’ rising valuation is matched by its impressively growing revenue.

Compass’ peers in the real estate technology space, both public and private, feature an exciting range of valuations.

In general, technology companies like Zillow, Redfin and Opendoor have higher valuations, while traditional brokerages like Realogy and RE/MAX have lower valuations. Investors clearly favor technology companies.

(Both Realogy and Purplebricks have recently released news and earnings results that resulted in a significant drop in valuation. I’ve used numbers from April in an effort to provide a more fair, “moving average” valuation.)

Revenue multiples

One way to determine a company’s value is by using a revenue multiple. That multiple — say 1x or 2x — is multiplied by current revenues to establish a valuation. The higher the multiple, the more optimistic investors are about future growth prospects, and the more that company is worth.

Compass sports a relatively high revenue multiple — rivaled only by tech company Zillow. While its business model is most similar to peers like Redfin, RE/MAX, eXp Realty and Realogy, investors are significantly more optimistic about Compass’ future prospects.

Growth rates significantly factor into a company’s valuation; investors are generally more optimistic the faster a business is growing. This cohort of real estate tech businesses are growing revenues at vastly different rates.

However, a high revenue growth rate does not necessarily correlate to a high revenue multiple, as evidenced by the following chart.

Of the fastest growing companies — Compass, eXp Realty and Opendoor — Compass boasts the highest revenue multiple, more similar to Zillow and Redfin. (Bubble size denotes overall valuation.)

Over the past three years, Compass’ valuation has been closely tied to its revenue, which is growing exponentially. As discussed in Part 1 of this series, that growth has come from an aggressive acquisition strategy. The revenue multiple for each of Compass’ recent capital raises has remained consistent: 5x-6x. Investor sentiment has remained consistently optimistic.

Transaction volumes

Another metric to consider when valuing companies — especially real estate tech companies that are involved in the transaction — is transaction volume.

A number of the biggest companies in real estate, including those discussed here, are newly obsessed with building end-to-end transaction platforms. And an important part of that platform strategy is offering ancillary services such as mortgage and title.

Another angle is the predictive and educational power of data. Whether it’s Zillow, Redfin, Compass or Keller Williams, all are talking about the power of data in their end-to-end platforms. Many companies consider it a potential competitive advantage and are making heavy investments to build out enhanced data capabilities.

To fully realize its value, a platform needs to be used. The up-sell opportunity around ancillary services and the predictive power of data all require transactions flowing through the platform, and the more the better.

Similar to the benefits of network effects, more activity on a platform makes it more valuable. Thus, the more transactions a brokerage facilitates, the stronger position it should have in the overall ecosystem.

A transaction volume metric for company valuations is not typically used nor talked about in the industry. The number of transactions each company conducts, and the number of consumers they touch, again varies wildly.

Despite so much potential future value being attributed to ecosystems that touch consumers and facilitate transactions, it does not correlate to company value. In fact, it is exactly the opposite. The following chart shows company valuations divided by transaction volumes — or the “value per transaction.”

Even though Realogy and RE/MAX have, by far, the most transactions flowing through their systems, investors are ascribing very little value to them.

Agent count

Part 1 of this analysis looked at how much Compass was paying for its brokerage acquisitions. Since the start of 2018, Compass’ agent count has increased from roughly 2,000 to 10,000.

Of those 8,000 new agents, around 4,200 came from acquired brokerages. Assuming a total of $230 million spent to acquire 14 brokerages with 4,200 agents, that’s a cost (or value) of $55,000 per agent.

When Compass raised its latest round in September 2018, it was valued at $4.4 billion, and at the time, had around 10,000 agents. Using the same methodology, each of Compass’ agents was worth — or valued — at $440,000.

If brokerage valuations were driven entirely by the number of agents — which, incidentally, are the primary revenue drivers — investors are valuing Compass agents eight times higher than what Compass itself is paying other brokerages through acquisition.

What about profit?

There’s one word missing from this analysis so far: profit. What role does the ability of a company to operate profitably play in its valuation? Not much.

Out of the companies mentioned in this analysis — Compass, Zillow, Redfin, RE/MAX, Opendoor, eXp Realty, Purplebricks and Realogy — collectively worth over $20 billion — only two are profitable: RE/MAX and Realogy.

Realogy, the company with the absolute lowest revenue multiple of 0.2x, is profitable. Together, RE/MAX and Realogy are worth $2 billion, less than half that of Compass. Clearly, the potential of future profits trumps the certainty of current profits for investors.

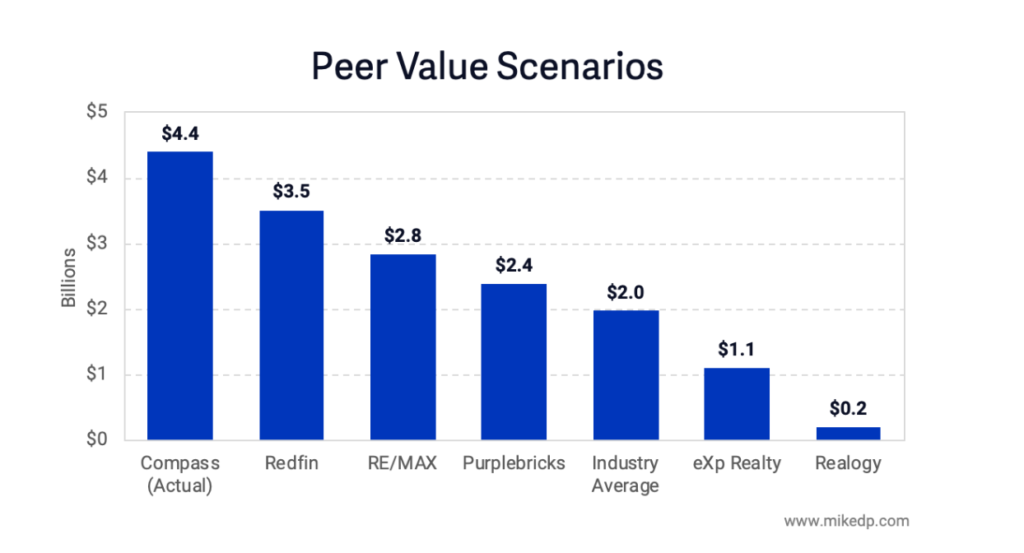

Peer valuation scenarios

What would Compass be worth if it were valued like some of its peers (using their revenue multiples)? It’s already at the high end of the range for those with similar business models: RE/MAX, Purplebricks, Realogy, eXp Realty and Redfin.

Compass is valued far and ahead of its peers, even those in the same class of technology-enabled brokerage. If it were valued similarly to Redfin, which is a public company, it would be worth $3.5 billion — a $900 million discount to its current valuation. Clearly investors see something more in the company.

If Compass were valued at Realogy’s revenue multiple, it would only be worth $200 million — over 20 times less than its current valuation.

Remember: Realogy is profitable, sees over 40 times the transaction volume and has over six times the revenue of Compass. This stat alone highlights the massive opportunity investors see for Compass, contrasted starkly with the bleak future forecast at Realogy.

A sustainable model?

Investors clearly see something more in Compass — something that massively sets it apart from its peers. Its valuation is being driven by a combination of massive growth fueled by an aggressive acquisition strategy and the promise of a tech-powered platform to give it a competitive advantage over peers.

It’s fair to say Compass is being valued as a tech company. In fact, Compass is being valued more optimistically than any other traditional or tech-enabled brokerage by a wide margin; it’s valuation more closely matches Zillow, a tech company with a completely different business model.

Having raised over $1.1 billion, Compass is unequivocally causing a revolution in the traditional real estate industry. But how sustainable is its model? Can it keep up its aggressive — and expensive — acquisition strategy and achieve profitability?

And will agents, without whom Compass wouldn’t generate any revenue, remain happy and stay under the Compass banner? Stay tuned: These topics will be explored in the next part of this series.

Check out:

- Part 1: How has Compass grown so fast? A look at the numbers

- Part 2: Is Compass a tech company or a traditional brokerage?

- Part 3: Traditional brokerage or tech company: How is Compass being valued?

How do you stay ahead in a changing market? Inman Connect Las Vegas — Featuring 250+ experts from across the industry sharing insight and tactics to navigate threat and seize opportunity in tomorrow’s real estate. Join over 4,000 top producers, brokers and industry leaders to network and discover what’s next, July 23-26 at the Aria Resort. Hurry! Tickets are going fast, register today!

Thinking of bringing your team? There are special onsite perks and discounts when you buy tickets together. Contact us to find out more.

Mike DelPrete is a strategic adviser and global expert in real estate tech. Connect with him on LinkedIn.