Reposted with permission from Mike DelPrete.

The first part of this series took a detailed look at Compass’ growth strategies, fueled by over $1.1 billion in venture capital.

The company often refers to itself as a tech company and a tech-enabled brokerage, which is part of the lure of the Compass vision — and the underpinning of its massive $4.4 billion valuation.

Now we turn to that fundamental question: Is Compass a tech company, or a traditional brokerage?

Ingredients of a tech company

A real estate technology company that operates as a brokerage (representing buyers and sellers in a real estate transaction) is nothing new.

There are tech-enabled brokers around the world: Redfin, Purplebricks, Duproprio and dozens of smaller players. The defining characteristic of these companies is how technology provides an efficient platform to scale — at rates much faster and at lower cost than traditional brokerages.

A real estate technology company should have the following three attributes:

- Tech staff: A technology company should employ technologists.

- Efficiency: By leveraging technology, operational efficiency should be higher than the industry average.

- Scalability: Technology should enable the business to scale in a non-linear manner.

This analysis focuses on these key attributes and compares Compass to its industry peers, both technology companies like Zillow and Redfin, and traditional brokerages like NRT (Realogy) and HomeServices of America.

Tech staff

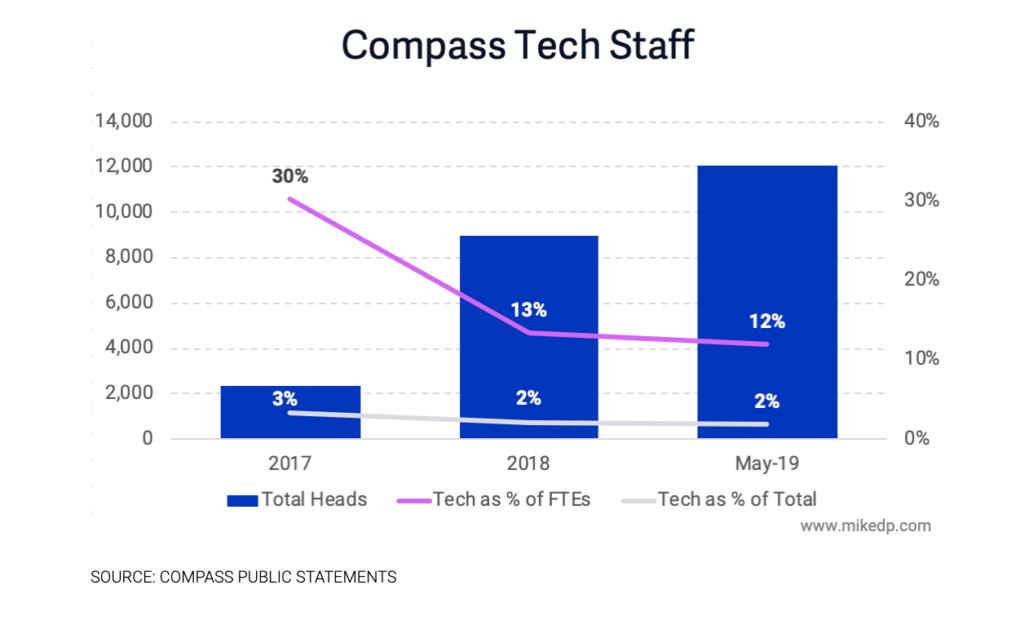

The first clue that a company may be a technology company is the number of software engineers it employs, both in absolute numbers and as a percentage of its total full time equivalent (FTE) headcount.

Readers that follow my work may recall a previous analysis where I benchmarked the percentage of tech staff at various real estate companies.

At the time, I observed that the most successful technology-enabled brokerages around the world (Redfin, Purplebricks and Duproprio) had around 10 percent technical staff. Compass was the outlier at four percent.

Compass is clearly staffing up and aggressively building a tech team. Compared to total headcount, including agents, the percentage of tech staff is still quite low (reflecting the central role of agents). However, Compass’ tech team represents a significant portion of its salaried, full-time employees.

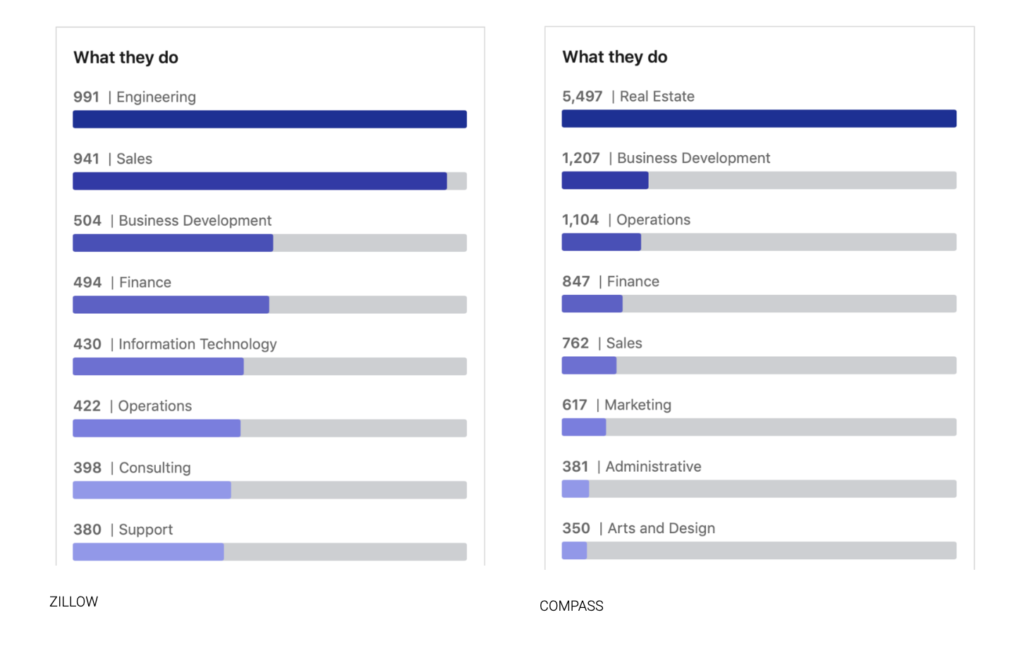

Many real estate technology companies, including Zillow, Redfin and Purplebricks, don’t publicly disclose the size of their tech teams. This is where LinkedIn comes in handy. While its employee data is not an absolute representation of the truth, it does provide a helpful comparison between companies.

Looking at software engineering staff as a percentage of the total shows a relatively accurate comparison between companies. (Note: Software engineers are just one part of a successful tech team.)

Backing out agents (independent contractors or otherwise) from the same calculation shows another way to look at the same data. Remember, this is just software engineers, and not the entire product team.

LinkedIn also shows the largest employee categories for each company. The top category for Zillow, which among its peer group is undoubtedly the most tech of the tech companies, is engineering.

The same engineering category is ranked No. 4 for Opendoor, No. 6 for Redfin and doesn’t appear until No. 11 for Compass.

Raw numbers help paint a complete picture. During a Bloomberg interview in April 2019, Compass stated that it currently employs 200 engineering staffers and wants to have 400 by the end of the year.

At the time of its IPO in 2017, Redfin had “more than 200 engineers and product managers” (or 9 percent of its staff), and today has nearly 200 engineers. And according to LinkedIn, Zillow has an engineering team approaching 1,000.

On the one hand, Compass is clearly outgunned by tech powerhouses like Zillow and Opendoor. On the other hand, it’s backing up its claims by aggressively hiring a sizable engineering team.

Efficiency

A classic measure of business model efficiency is revenue per person. More efficient and lucrative business models — typically technology companies — are able to generate higher revenues with a smaller staff.

The chart below looks at revenue per person (including agents, which are the drivers of revenue) during 2018. Since Zillow, Redfin, and Compass each grew their headcount rapidly during the year (from 2,600 to 9,500 at Compass), I’ve used a midpoint headcount number to reflect a more accurate representation (6,050 for Compass).

It’s worth noting that Compass’ target market is the luxury space, with an average home price well over $1 million. Given that a brokerage derives its revenues as a percentage of the sale price, overall revenues will correlate closely with average sale price. The average sale price of a Compass home is about double that of Redfin, yet Redfin still generates more revenue per person than Compass.

Organizational efficiency can be measured by looking at the average number of transactions an agent is able to close each year, called “production.” One would expect a technology company, or a technology-enabled brokerage, to provide its agents greater efficiency through the smart application of technology. Those efficiency gains should translate to the ability to work on and close more transactions.

The chart below compares the average agent production for Compass, Redfin, Purplebricks in the U.K, and the industry average in the U.S.

For this calculation I’ve again used the 2018 midpoint agent count for Compass, raising its average from four to seven transactions per agent, identical to the overall industry average. Redfin’s agents, on the other hand, are 4.5 times more efficient than the industry average — an exponential efficiency gain resulting from technology combined with a novel operating model.

Another way to look at efficiency is not by total agent count, but by total headcount. This method considers the entire organization that, directly and indirectly, supports agents in closing transactions.

Two interesting things happen in this analysis. First, Compass drops slightly below the industry average (represented by NRT). Second, Redfin’s efficiency lead drops to 2.5 times the industry average, a reflection of how important its non-agent support staff is to its overall model.

Looking at agent efficiency of the top 20 U.S. brokerages shows Compass right in the middle of the pack (which, incidentally, is led by Redfin).

Yes, Compass is more efficient than some brokers, but its agents are considerably less efficient than a number of others, many of which don’t even style themselves as “tech-enabled brokerages.” Even agents at traditional industry stalwart HomeServices of America are more efficient.

Overall sales volume (the total value of houses sold) per agent shows another angle. Not all houses are created equal, and by being in the luxury space (average home value of $1.3 million), Compass is near the top of the pack when it comes to agent sales volumes.

Its agents can sell less homes and still make a considerable amount of money.

Combining both average transactions closed and sales volume per agent shows a more holistic view of agent efficiency.

Redfin, the clear outlier, operates a model that is exponentially more efficient than the industry average. Compass is clustered with other luxury brands due to its high average sales price.

When evaluating Compass, the evidence shows a business whose agents are no more efficient than the industry average — by a number of different factors.

Overall business model efficiency, as evidenced by revenue per person, is singularly driven by being in the luxury market where home prices are high.

Technology and product development efforts in 2019 and beyond may deliver on efficiency promises, but for the time being, it remains simply that — a promise.

Scalability

Technology businesses should scale non-linearly. They should be able to grow revenues faster than expenses and leverage technology to become more efficient over time — especially when compared to traditional peers.

Between 2016 and 2018, each of the following businesses grew revenue and added headcount, but all at different rates. Each new hire at Zillow corresponded to around $300,000 of additional revenue, compared to around $80,000 for each new hire at Compass (slightly below the traditional industry average, as represented by NRT).

Measuring revenue per FTE over time gives another sense of business scalability. One would expect a scalable technology business to see efficiency improve over time.

The chart below shows the changing revenue per full time equivalent over the span of three years, again using a midpoint FTE count for 2018 due to the rapid headcount growth in all three businesses.

The evidence shows a clear trend: Each business is generating revenue more efficiently as it scales. That trend is more pronounced at Zillow and Redfin, and it is the hallmark of a scalable business model.

Compass is scaling differently, and less efficiently, than its peers. This does not mean that Compass is any better or worse than Zillow or Redfin — there are a variety of business models, each with their own merits — just that it is a different type of business.

The valuation quandary

Is Compass worth $4.4 billion? Should Compass be valued as a traditional brokerage or a technology company?

The disruptive companies leading the pack in real estate — Zillow, Redfin, Opendoor and Purplebricks — all combine technology with a novel operating model different than a traditional brokerage. It is this combination that leads to exponential gains in efficiency.

Regardless of whether Compass is a technology company, it unquestionably needs to be a technology company — both to support its massive valuation of $4.4 billion and to be a lasting sustainable business.

This topic will be explored further in the third part of this series, which will cover valuation.

Check out:

- Part 1: How has Compass grown so fast? A look at the numbers

- Part 2: Is Compass a tech company or a traditional brokerage?

- Part 3: Traditional brokerage or tech company: How is Compass being valued?

Editor’s note: Some of this story and the graphs have been updated upon further analysis.

Check out part one of this series: “How has Compass grown so fast? A look at the numbers.”

Mike DelPrete is a strategic adviser and global expert in real estate tech. Connect with him on LinkedIn.