There’s an overwhelming amount of data and headlines circulating. This column is my attempt to make sense of it all for you, the real estate professional, from an overall economic standpoint.

Today, we are going to take a look at the economic and real estate announcements that came out last week as there were several of note and worthy of discussion. To start off with, we had the August retail sales numbers.

They were up 0.6 percent on the month, and up 2.6 percent year over year, but that isn’t the real story. Although you can clearly see growth pulling back significantly from where it was in May and June, I was actually rather pleased!

You see, the pullback should surprise no one. Why? Well, spending in May and June was heavily influenced by enhanced unemployment benefits and the $1,200 check that appeared for a lot of people across the country.

And although growth slowed, I was delighted to see that it didn’t turn negative — and that’s important because it demonstrates a somewhat solid base to build on.

What I see is that consumers are actually still in pretty good shape. That said, it will be interesting to watch what happens as we head into the holiday season which, by the way, is scheduled to start really early if we are to believe comments coming from many retailers across America. Oh joy!

Next up? The National Association of Home Builders Housing Market Index

And all I can say is — wow. The number came in at 83, which is the highest it has ever reached in its more-than-35-year history. And for those of you who don’t follow this index, any number above 50 is positive. Do you see the V?

When we look at the three components of the index, all rose to record levels, with the traffic index — which looks at prospective buyer visits to housing developments — up by a massive seven points versus August. Current sales conditions, as well as sales expectations for the next six months, are also looking extremely good.

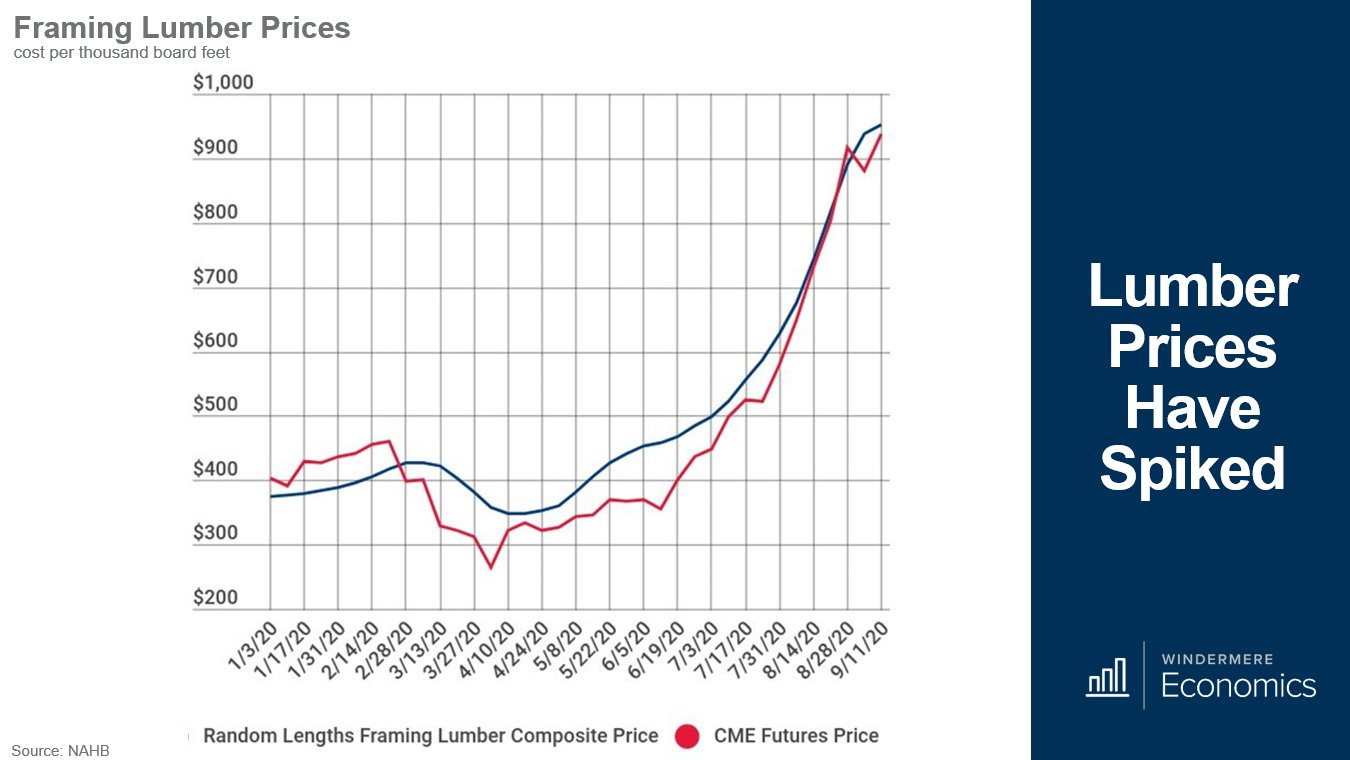

But before we all get carried away, there was a negative that was discussed in the report, and it’s regarding lumber prices.

Now, regular followers of mine will know that I’ve spent years moaning about the cost of building homes, but nobody could have expected to see this kind of increase. So, what’s going on?

Well, because of COVID-19-induced supply chain issues — and now with wildfires raging across the West — lumber prices have gone parabolic, with the cost of lumber rising by a massive 170 percent over just the past few months.

This remarkable increase has done one thing. It’s added approximately $16,000 to the cost of building an average-sized, single-family home in America.

I would add that one of our local companies Weyerhaeuser owns about 2.9 million acres of timberland in Oregon and Washington. It is now saying that the fires have reached some of its land, so I find the likelihood of costs pulling back any time soon to be remote.

What about building permits and starts?

Although the total number of permits dropped by 0.9 percent between July and August, I was really happy to see single-family permits jumping by 6 percent to an annual rate of 1.036 million units. This is really good news because it’s the first time the number has broken north of 1 million since May, 2007.

And if we look at housing starts, they showed a similar pattern, with total starts down by 5.1 percent month over month, but single-family starts up by 4.1 percent.

Starts rose the most in the West, where they’re up by 23.4 percent, and the Midwest, where they were 20 percent higher. Starts were lower in the Northeast, where they were down by 21.9 percent (but that’s a very small market), and they were 3.8 percent lower in the South.

Now, I do want to bring your attention to a little-discussed number inside the monthly report that looks at the number of homes actually under construction. You may ask about the difference between home starts and homes under construction, and it would be a good question.

The difference is that starts only look at homes where footings have been poured, but that’s it. Homes under construction are ones that have progressed beyond foundation work and into framing, but the home is not yet completed.

There were 521,000 units under construction in August. That’s up by 2 percent on the month, but it’s only a meager 1 percent higher than what was seen in August of 2019.

As I see it, the report shows continued strength in single-family development, which is unsurprising, given the strong demand. However, construction activity hasn’t risen to the levels I’m looking for and, given what we are seeing in regard to costs, I do wonder if we will see new home development increase significantly in the foreseeable future. You see, any cost increases will need to be passed on to the homebuyer, and I’m not sure how they are likely to react.

What is consumer sentiment looking like?

Finally, we got the provisional September number for consumer sentiment. It was a good one, with the overall index coming in at 78.9, and it’s now at its highest level since COVID-19 hit back in March when the index was measured at 89.1.

Most people don’t look too closely at the details, but there are two components to the index. There’s the present condition index, which measures how we’re feeling about the economy today. There’s also the future expectations index, which gauges how we believe the economy will be in six months.

As you can see, both rose quite nicely, but the greatest increase was seen in the expectations index. This tells me that we’re fairly confident that by next spring, we will be in a decent position when it comes to the U.S. economy.

So, there you have my thoughts on last week’s data releases. And on deck for this week is data on existing-home sales and prices in August, which comes out on Tuesday, the FHFA home price Index for September, which comes out on Wednesday, and the August data on new home sales, which comes out on Thursday.

To get the big picture including all of the data, watch the full video above.

Matthew Gardner is the chief economist for Windermere Real Estate, the second largest regional real estate company in the nation.