New markets require new approaches and tactics. Experts and industry leaders take the stage at Inman Connect New York in January to help navigate the market shift — and prepare for the next one. Meet the moment and join us. Register here.

Mortgage lenders kicked off 2022 knowing that with rates likely to continue heading up, they’d need to shift their footing from refinancing existing homeowners to serving homebuyers.

But few anticipated that mortgage rates would rise so quickly and go so high — triggering mass layoffs as purchase lending not only failed to cushion the massive decline in refis, but added to lenders’ woes when home sales also slowed.

The mortgage industry has so far managed to dodge the kind of chaos created by the subprime mortgage meltdown that triggered the Great Recession of 2007-09. But the turmoil stirred by rising rates stressed some business models more than others and helped crown a new leader in home lending.

Looking ahead to next year, there’s a chance mortgage rates will surprise again — but this time, by falling more rapidly than many forecasters had envisioned when they were peaking in October.

As was the case in 2022, the companies that come out on top may be those that are most adept at adjusting to unforeseen circumstances.

- Mortgage rate shock

- Rushing to ‘right size’

- A slowdown, not a meltdown

- A new leader is crowned

- Harnessing tech and local connections

- The outlook for 2023

Mortgage rate shock

Fed policymakers began the year by approving a modest, 25-basis point interest rate hike in March aimed at curbing inflationary pressures driven largely by the lingering impacts of pandemic-induced supply chain disruptions and tight labor markets.

But Russia’s February invasion of Ukraine was not just the beginning of an ongoing human tragedy. It also threw a monkey wrench in the Fed’s inflation-fighting plans, by sending energy prices soaring. With key inflation indicators worsening, the Fed started ratcheting up the federal funds rate in 50- and 75-basis point increments.

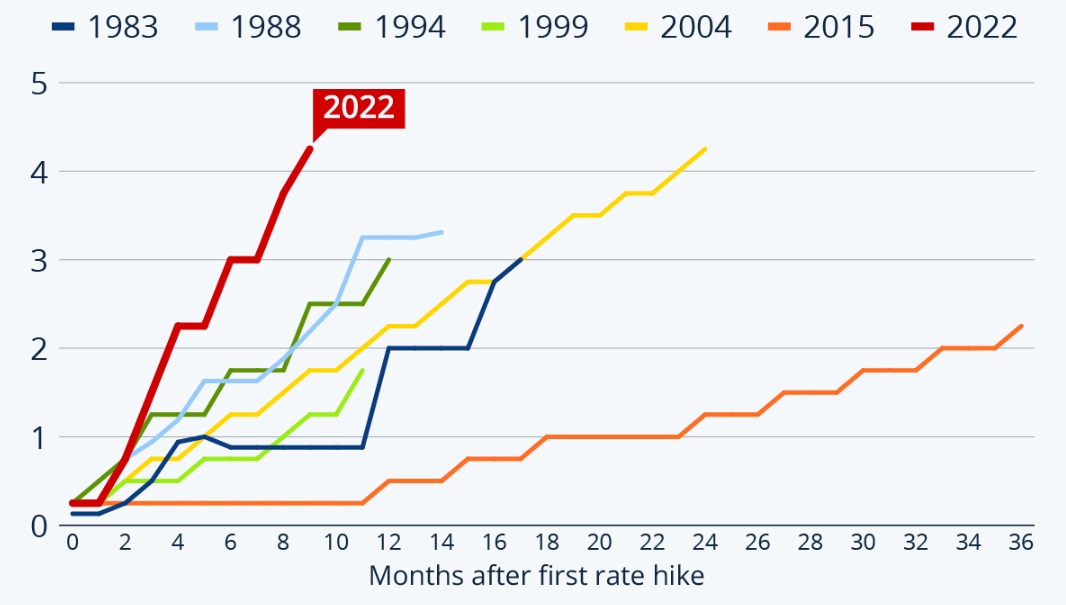

The Federal Reserve hiked rates in record time in 2022

Changes in federal funds target rate in past tightening cycles (in percentage points) | Source: Analysis of Federal Reserve data by Statista

By the end of the year, the Fed had raised its target for the benchmark short-term interest rate seven times in eight months, by a total of 4.25 percentage points — the fastest run-up in Fed history.

Mortgage rates had already started climbing in the fall of 2021, as the Fed provided plenty of advance warning that it would withdraw support it had provided to mortgage markets during the pandemic through “quantitative easing.” As the central bank raised short-term rates at an unprecedented pace, it also shifted to “quantitative tightening,” trimming its $9 trillion balance sheet by letting $60 billion in Treasurys and $35 billion in mortgage debt roll off the books each month.

Mortgage rates more than doubled, with rates on 30-year fixed-rate mortgages hitting a 2022 peak of 7.16 percent on Oct. 24, according to the Optimal Blue Mortgage Market Indices.

Mortgage rates hit 2022 peak in October

While mortgage lenders were preparing for their profitable refinancing business to dry up in 2022, they hoped to fill in much of that lost business by pivoting to make more purchase loans to homebuyers. But mortgage rates went up so quickly — more than doubling from pandemic lows — the boom in purchase lending failed to materialize.

Return to table of contents

Rushing to ‘right size’

The first inkling of the trouble that lay ahead for mortgage lenders in 2022 took place before the year even kicked off when end-to-end mortgage, title and closing services provider Better Holdco Inc. laid off 900 employees just before Christmas 2021 on a Zoom call.

After the departure of senior executives, including Christian Wallace, the head of Better’s real estate brokerage subsidiary Better Real Estate LLC, Better cut another 3,000 workers from the payroll in March. By May, Better employed 2,900 workers, down 72 percent from 10,000-plus employees at the end of 2021.

It wasn’t long before some of the biggest names in the business were following suit and announcing plans to “right size” in response to the shrinking demand for mortgages. Companies making headlines included household names like Wells Fargo, Rocket Mortgage and loanDepot.

LoanDepot mortgage originations by purpose

Source: LoanDepot regulatory filings

After loanDepot founder Anthony Hsieh handed off the CEO reins in April to CoreLogic veteran Frank Martell, the company proceeded to shed 5,200 workers through layoffs and attrition in 2022, as purchase loan and refi production posted double-digit declines.

In August, Martell announced that loanDepot was getting out of the wholesale mortgage lending business altogether and would no longer accept loans originated by independent mortgage brokers.

Frank Martell

“Like other mortgage companies, we scaled our organization during 2020 and 2021 to meet the demands of unprecedented mortgage volumes, especially refinancing transactions,” Martell said on a second-quarter earnings call with investment analysts. “After two years of record-breaking volumes, the market has contracted sharply and abruptly so far this year.”

While Wells Fargo hasn’t been willing to provide specifics on how many workers it has shed from its mortgage operations, the bank laid off thousands of workers company-wide in 2022 and closed hundreds of branches.

Even as mortgages originated by branch offices shrank, Wells Fargo reportedly weighed exiting the correspondent lending business, with executives said to be concerned about the financial and reputational risk of buying mortgages from third parties.

Wells Fargo closed out the year by agreeing to pay $3.7 billion to settle allegations by federal regulators that it harmed millions of consumers through widespread mismanagement of mortgages, auto loans and deposit accounts.

Charlie Scharf

“We have made significant progress over the last three years and are a different company today,” Wells Fargo CEO Charlie Scharf said of the settlement. “We remain committed to doing the right thing for our customers and working closely with our regulators and others to deal appropriately with any issue that arises.”

In a bid to avoid layoffs, Rocket Mortgage’s parent company, Rocket Companies Inc., made buyout offers in April to about 2,000 workers. If accepted, the buyouts were expected to save Rocket about $180 million per year, executives said.

Other lenders downsizing in 2022 include some companies that may not be household names, but that have significant market share.

Mr. Cooper — better known to many consumers as a loan servicer — laid off 18 percent of the 8,200 employees it started the year with in three rounds of layoffs totaling about 1,470 workers. Pennymac laid off 236 workers from six locations in California in May, citing falling demand for home loans.

Smaller lenders, including startups employing technology to minimize costs, weren’t immune from the impacts of rising rates.

Tomo, a mortgage fintech launched by former Zillow executives with an exclusive focus on purchase loans, cut its workforce by nearly one-third in May. But by the end of the year, Tomo was in expansion mode again in December announcing launches in Maryland, New Jersey, Oregon, Pennsylvania, Virginia and Washington, D.C.

While real estate brokerages with mortgage arms might have hoped they’d have an edge in the pivot to serving homebuyers, in the end, some were forced to downsize.

As part of its bid to expand its presence in mortgage lending by acquiring San Francisco-based Bay Equity Home Loans for $135 million, Redfin issued pink slips to 121 workers at its existing mortgage business. Redfin cut another 13 percent of its staff in November when it announced that it was ending RedfinNow, the company’s iBuying program.

Real estate franchise giant Keller Williams started laying off workers at its lending arm, Keller Mortgage, in October 2021 with more pink slips going out in May and October 2022. Even as it laid workers off, Keller Mortgage said it was committed to long-term growth and is currently advertising openings for local loan officers and sales managers.

Companies providing services to mortgage lenders were also affected by the slowdown in lending with Blend, Doma and Notarize among those announcing layoffs.

Power buyers and iBuyers — potential partners or competitors of mortgage lenders — downsizing this year include Knock, Offerpad, Opendoor, Orchard and Ribbon.

Return to table of contents

A slowdown, not a meltdown

Unlike the subprime mortgage meltdown that precipitated the 2007-09 recession, the slowdown in mortgage lending has yet to reveal significant cracks in the foundation of the mortgage business.

When home prices started to reverse from their 2005-06 peaks, fears of a wave of homebuyer delinquencies and foreclosures left subprime lenders without access to capital markets. The sudden tightening of mortgage credit exacerbated home price declines, and millions of homeowners lost their homes to foreclosure in the recession that followed.

As the pandemic homebuying boom came to an end, some lenders who offered “non-Qualified Mortgages” not eligible for purchase by Fannie Mae and Freddie Mac had trouble selling those loans to investors at a profit.

But the main problem for lenders like First Guaranty Mortgage and Sprout Mortgage wasn’t that investors were worried that the loans they were selling were at a high risk of default. It’s that mortgage rates went up so fast, the yields on those loans quickly became less attractive to investors — in some instances forcing lenders to take “haircuts” and sell the loans at a loss.

The vast majority of loans made today meet strict underwriting standards set by Fannie Mae, Freddie Mac and the Federal Housing Administration. While rising interest rates have made adjustable-rate mortgage (ARM) loans more popular, stricter underwriting standards have limited their availability and made them less risky.

According to a recent analysis by the Urban Institute, ARM loans accounted for 12 percent of mortgage applications in November, up from 3 percent in 2021. But ARM loan share climbed as high as 35 percent in 2005 during the last housing boom, before stricter regulations limited their use.

Before those regulations kicked in, ARM loans would typically reset after one to three years, in many cases causing payment shock for borrowers facing substantially larger monthly payments. Today, an ability-to-repay rule requiring lenders to qualify borrowers at the highest rate they could experience in the first five years means few ARMs have a reset period shorter than five years.

Another factor that could help prevent a meltdown is that the dramatic home price appreciation seen during the pandemic has left most homeowners with comfortable equity cushions. However, recent homebuyers who may have bought at the peak of the market could be at risk in the future — particularly if they purchased their homes with little or no money down.

Recent home price declines in many markets have left about 450,000 homeowners underwater — owing more on their mortgages than their homes are worth — according to data and analytics provider Black Knight.

Homeowners with little or no home equity are at higher risk of foreclosure if they encounter financial difficulties like job loss or health issues, because it’s harder for them to pay off their mortgages by selling their homes. Black Knight’s data shows more than 20 percent of homebuyers who took out FHA or VA purchase mortgages this year are underwater and two-thirds have less than 10 percent equity.

But at 0.84 percent, negative equity rates among all mortgaged properties remain “extremely low” by historical standards. And at 2.91 percent in October, the national delinquency rate remains well below the historical average of 4.54 percent.

Return to table of contents

A new leader is crowned

If rising mortgage rates curbed demand for home loans, it also gave homebuyers who were determined to forge ahead with their plans a greater incentive to shop around for the best rate.

The nation’s biggest wholesale lender, United Wholesale Mortgage, seized the opportunity, launching a “Game On” pricing initiative in June to boost market share and promote the mortgage brokerage business model.

Not only did UWM slash rates by 50 to 100 basis points (0.5 to 1 percentage point), but it rolled out new services for mortgage brokers as part of a campaign to persuade loan originators who work for banks and other retailers to defect to independent mortgage brokerage shops.

Mat Ishbia

Retail mortgage loan originators “have always known it’s hard for them to compete on price and rates with brokers and with service and technology support brokers have today,” UWM CEO Mat Ishbia told investment analysts in August. UWM’s Game on pricing initiative, he said, was designed to be “the last nudge that we believe retail loan officers need to convert to being a loan officer broker shop or start their own broker shop.”

The gambit worked, helping UWM boost purchase mortgage production to record levels and surpass Rocket Mortgage as America’s biggest provider of home loans during the third quarter.

UWM’s record Q3 purchase originations

Source: Inman analysis of UWM regulatory filings

UWM’s third-quarter refinancing production was down 84 percent from the same time a year ago to $5.8 billion. But UWM’s $27.7 billion in third-quarter purchase loan originations exceeded Rocket Mortgage’s total loan production — both purchase and refinancing.

To Ishbia, it was vindication of not only the mortgage broker model but UWM’s controversial decision to stop doing business with mortgage brokers who send loan applications to rivals Rocket Mortgage or Fairway Independent Mortgage. After Ishbia took to Facebook in March 2021 to announce the “All In” initiative, UWM faced criticism and was entangled in litigation as both a defendant and a plaintiff.

“We told you when we launched ‘All In’ in March of 2021 that this decision would help the broker channel grow and ultimately our share of the channel,” Ishbia said in November of UWM’s third-quarter results. “Some questioned us and thought we would lose brokers and market share. However, the exact opposite has happened.”

Ishbia promptly celebrated by negotiating a deal to acquire a majority stake in the Phoenix Suns and its sister WNBA team, the Phoenix Mercury. The deal, announced Dec. 20, sets the stage for UWM to continue its rivalry with Rocket Mortgage on the basketball court — Rocket Mortgage co-founder Dan Gilbert is the majority owner of the Cleveland Cavaliers.

Return to table of contents

Harnessing tech and local connections for growth

If mortgage rates remain elevated next year that could provide an edge to other lenders employing the mortgage broker business model. Mortgage brokers often have good connections with local real estate agents and past clients, and because they work with multiple lenders, they’re often able to help borrowers find lower rates.

RE/MAX’s mortgage subsidiary, Motto Franchising LLC, provides technology, compliance, training and marketing for mortgage brokers, making its “mortgage brokerage-in-a-box” services available not only to RE/MAX affiliates but to any qualified real estate brokers or entrepreneur.

After helping Motto Mortgage franchisees open 60 new offices in 2021 and more than a dozen more this year, Motto Franchising is now supporting more than 200 offices in 39 states. In September, Franchise Business Review ranked Motto Mortgage as a Top Recession-Proof Franchise based on an assessment of its potential to outperform competitors during challenging economic times.

Some smaller lenders who are focused on providing purchase loans to homebuyers have also been using technology and local connections to grow their market share. Tech provider SimpleNexus singled out Hometown Lenders as “a model for how enterprise lenders can maximize their success and achieve astonishing growth with a great team and great technology.”

Atlanta-based Silverton Mortgage, which last year began offering hybrid e-closings using Remote Online Notarization (RON) capabilities provided by the digital closing platform Snapdocs, is another example of a lender that has been expanding its national footprint while others are downsizing.

The outlook for 2023

If the rapid ascent of mortgage rates this year took many by surprise, the potential for rates to come back down next year should not.

At their final meeting of the year, Federal Reserve policymakers signaled their readiness to dial back the pace of short-term interest rate hikes. The realization that the Fed is nearing the end of its rate-hike campaign has had a stabilizing effect on long-term rates like Treasury yields and mortgages.

There’s also room for the abnormally wide primary mortgage spread — the difference between 10-year Treasury yields and rates for 30-year fixed-rate conforming mortgages — to narrow.

Economists at Fannie Mae now think rates on 30-year fixed-rate loans peaked during the fourth quarter of 2022 and could dip below 6 percent by the first quarter of next year. In a Dec. 19 forecast, economists at the Mortgage Bankers Association projected rates will fall to 5.2 percent by the end of next year and average 4.4 percent during the second half of 2024.

Mortgage rates expected to fall

Source: Fannie Mae December 2022 housing forecast, MBA housing forecast

Lower rates aren’t expected to keep home sales from continuing to decline next year; however, with a recession looming and many would-be sellers feeling locked in by the even lower rates on their existing mortgage.

Fannie Mae forecasters are predicting the U.S. will enter a recession in the first quarter of 2023 and post negative 0.5 percent GDP growth next year before going into expansion mode again in 2024 with a 2.2 percent annual growth rate. MBA economists are expecting a recession in the first half of 2023, with unemployment jumping from 3.7 percent to 5.5 percent by the end of 2023.

Mortgage originations projected to decline again next year

Projected mortgage originations in trillions of dollars. Source: Fannie Mae December Housing Forecast

Economists at Fannie Mae expect mortgage origination dollar volume to fall 28 percent next year to $1.7 trillion, with refis tumbling by 47 percent to $366 billion and purchase loan volume falling by 20 percent to $1.33 billion. MBA forecasters are predicting a 15 percent decline in mortgage origination volume next year to $1.9 trillion.

“This has been a very rough time for many lenders as not only have they been challenged by this decline in dollar volume, but with bigger average loan sizes over the past two years, the drop in unit volume has been even larger,” MBA economists Mike Fratantoni and Joel Kan noted in commentary accompanying their latest forecast.

“We do expect that the housing market will lead the U.S. out of this recession, just as it has led the way into one,” Fratantoni and Kan concluded. “While we expect that 2023 will be a tough year for the broader economy as well as the housing and mortgage markets, it should ultimately bring lower mortgage rates and a return of housing demand as millennial first-time buyers enter the market in earnest.”

In November, Fannie Mae and Freddie Mac’s regulator gave the mortgage giants a green light to back mortgages of up to $726,200 in most parts of the country next year. Fannie and Freddie’s conforming loan limit will exceed $1 million in 105 counties and Census areas concentrated in nine metro areas where home prices are far above the national average.

To make sure Fannie and Freddie continue to serve homebuyers of limited means, the Federal Housing Finance Agency also ordered the mortgage giants to eliminate upfront fees on many purchase loans.

Sandra Thompson

“As I often say, improving access and fostering safety and soundness are twin pillars of our work,” FHFA Director Sandra Thompson said in October. “It is not a choice between the two. Instead, they can — and do — complement each other.”

Get Inman’s Extra Credit Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.