It’s been a long haul since the housing bubble burst in 2006 but there’s growing evidence that the foreclosure crisis is quickly winding down even as a stubborn batch of bad loans originated during the height of the housing bubble continues to pollute the real estate ecosystem.

First, let’s look at evidence the foreclosure crisis is truly over.

U.S. foreclosure activity dropped to a 74-month low in April, with 144,790 properties with foreclosure filings. Although still about twice as high as the average 75,000 per month in 2005, it was 60 percent below the monthly peak of more than 367,000 in March 2010.

Given the much tighter lending standards of the past few years and recently rising home prices, the downward trend in new foreclosure activity at the national level should continue for the foreseeable future, until monthly foreclosure activity is back to that “normal” level of about 75,000 properties with foreclosure filings a month.

The inventory of homes stuck in the foreclosure process was still up 4 percent in May from a year ago, caused primarily by elongated foreclosure timelines in judicial foreclosure states, but those inventory numbers should also turn a corner and start heading down in the relatively near future at the national level — although there will certainly be some states with longer foreclosure timelines where this trend will lag.

Loans originated during the most inflated years of the housing bubble account for the bulk of foreclosure inventory in 2013, even seven years after the bubble burst. Nearly three-fourths of loans in foreclosure (74 percent to be exact) as of May were originated between 2004 and 2008, according to RealtyTrac data, while 12 percent were originated after 2008 and 14 percent were originated before 2004.

At the current pace of bank repossessions (a little more than 40,000 a month so far this year) and third-party foreclosure sales (a little less than 30,000 a month so far this year), the approximately 850,000 loans now in the foreclosure process will be flushed out in about a year. It will take an additional six months for the bank-owned homes to be sold to third parties.

Bad news on bad loans

Unfortunately, loans already in the foreclosure process do not represent the totality of potentially toxic loans that need to be cleaned up. RealtyTrac data show that 37 percent of all outstanding mortgages not in foreclosure were originated between 2004 and 2008, representing more than 14 million loans. Furthermore, based on an 80 percent sample where interest rate data was available, approximately 88 percent of the 14 million at-risk loans have an interest rate of 6 percent or higher — indicating that the homeowners attached to those loans could benefit from a refinancing but have not done so.

One reason that some of these 14 million loans have not been refinanced is because they are seriously underwater. RealtyTrac data shows 47 percent have a loan-to-value ratio of 125 percent or higher, meaning the combined loan amount is at least 25 percent higher than the estimated market value of the home securing the loans. By comparison, 15 percent of the loans originated after 2008 are seriously underwater, and 23 percent of loans originated before 2004 are underwater.

Rising home prices will help lift some of these underwater loans into positive equity, allowing the homeowners to sell or more easily refinance to avoid foreclosure. Additionally some homeowners will finally take advantage of the Home Affordable Refinance Program and refinance even if they are underwater.

But some of those 14 million higher-risk loans still lingering from the 2004 to 2008 era will eventually end up in foreclosure. At the historically normal rate of 1 percent, that adds up to an additional 1.4 million foreclosures likely spread out over the next five years. That five-year horizon is the point at which home prices should have risen enough to give virtually all homeowners with these loans the escape hatch of selling with equity to avoid foreclosure.

Good news on newer loans

The good news is that about 42 percent of all outstanding mortgages were originated after 2008, when lending standards tightened up dramatically. Among that group of more than 15 million newer loans, only 11 percent are estimated to have an interest rate of 6 percent or above, and only 15 percent are seriously underwater.

Even loans guaranteed by the Federal Housing Administration — potentially the most risky loans still around because of the low down payment requirement — appear to be performing markedly better since 2010.

The FHA has banked more than $20 billion in additional reserves during the past three years. New FHA loans are generating surplus funds. These funds are being used to offset losses from past loans, especially from mortgage products the FHA no longer insures such as financing with “seller-assisted” down payments.

While the last three years of tighter lending standards ensure that the U.S. housing market is no longer in the midst of a foreclosure crisis, massive cleanup is still needed to clear out the wreckage left behind by the housing bust.

This cleanup phase requires that those in the housing and mortgage industry — not to mention policymakers — remain diligent and alert to another crisis. Nevertheless, similar to a natural disaster, the cleanup phase of this man-made disaster brings with it a sense of optimism that stands in stark contrast to the fear that often permeates in the midst of a crisis.

Prime time to buy and sell foreclosures

The rising optimism in the housing market, and the rising home prices that go with it, translate into a good opportunity time to buy a foreclosure. This may seem counterintuitive because foreclosures are now harder to find, but they are still selling at an average price point that is more than 30 percent below the average price point of a nondistressed home.

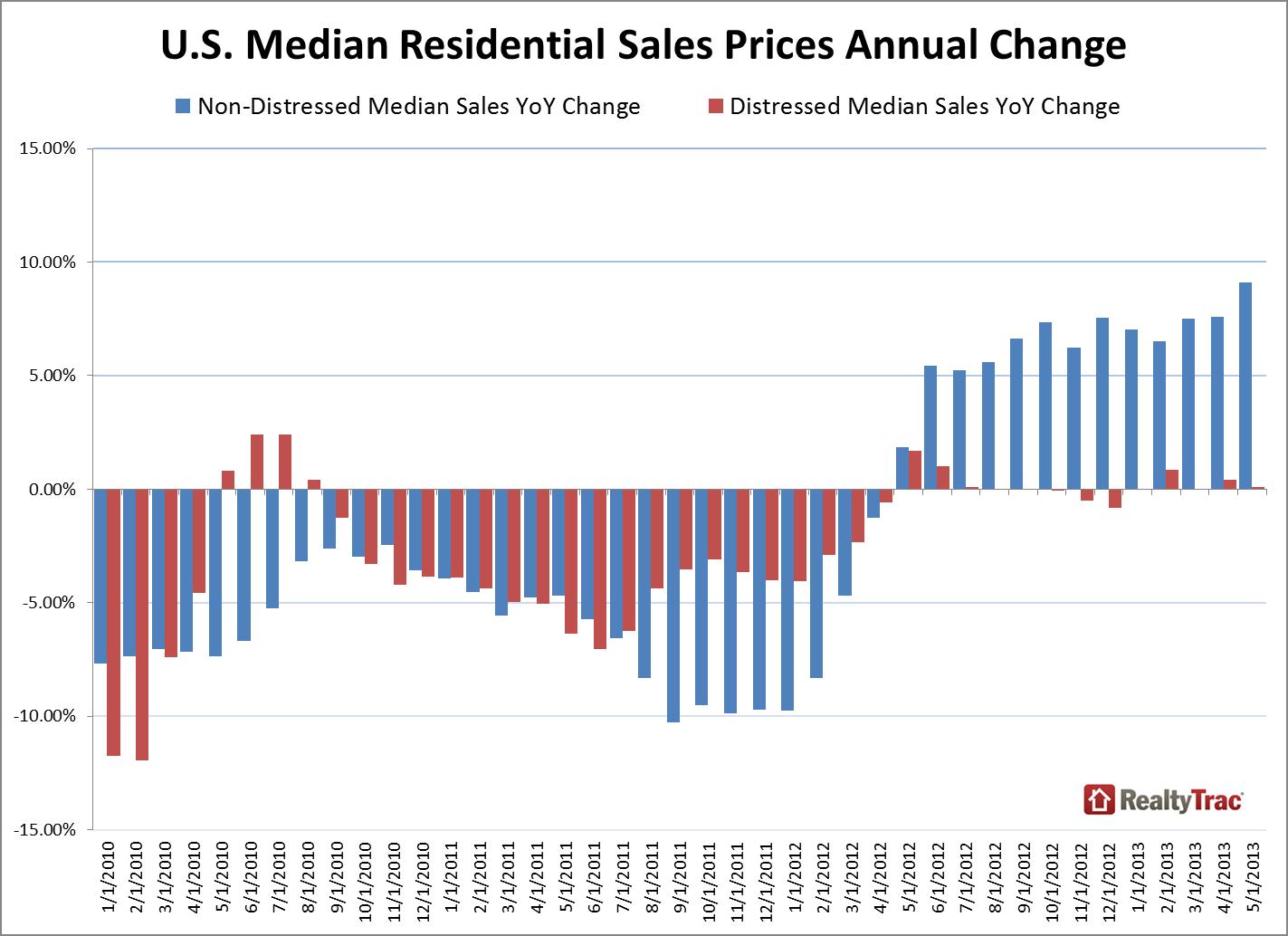

And while nondistressed median home prices are 13 months past bottom (see chart), distressed median home prices are just beginning to show signs of bottoming out, with prices flat or rising from a year ago for five consecutive months. That means foreclosures offer much more upside potential in terms of appreciation going forward than do nondistressed homes.

The rising appreciation on foreclosures also makes it a good time to sell — both for banks looking to unload REO inventory, and for homeowners in foreclosure looking to sell to avoid foreclosure. In some cases, the rising appreciation may even mean those distressed homeowners no longer need to sell via short sale.

Daren Blomquist is vice president at RealtyTrac. This article was co-authored by Jake Adger, chief economist at RealtyTrac.