Takeaways:

- Escalating rent prices are eating up a significant portion of renters’ income.

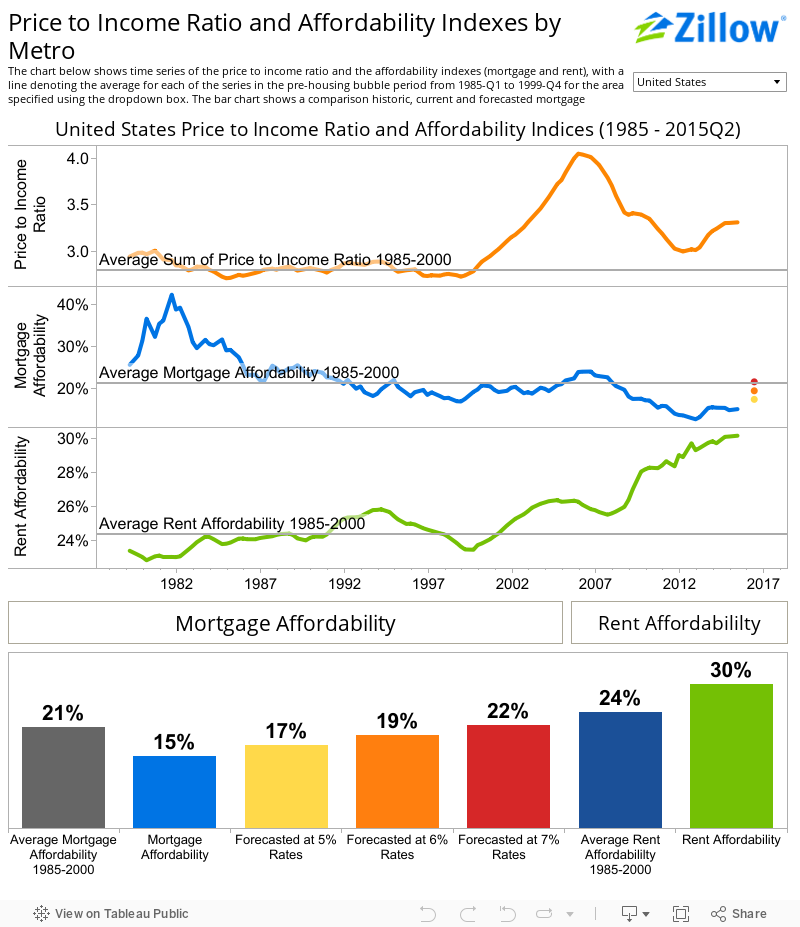

- Renters can expect to spend 30 percent of their income on rent — the highest percentage we have seen to date.

- Buyers can expect to spend 15 percent of their monthly income on a monthly mortgage payment.

Although renting an apartment or home makes a lot of sense for some people, escalating rent prices are eating up a significant portion of renters’ income, according to a Zillow analysis of U.S. rental and mortgage affordability in the second quarter.

Renters can expect to spend 30 percent of their income on rent — the highest percentage we have seen to date — while buyers can expect to spend 15 percent of their monthly income on a mortgage payment, Zillow said.

Prior to the real estate market collapse, renters could expect to pay about 24.4 percent of their incomes on rent. From 1985 through 2000, homeowners spent about 21.3 percent of their monthly income on mortgage payments, so homeowners are definitely making out better than renters at the present time.

Rental affordability worsened year over year in 28 of the 35 largest metro areas covered by Zillow. Compared to historic norms, rents are unaffordable in 77 percent of metropolitan areas, especially high-demand markets like Miami, San Francisco and San Jose.

At the same time, many markets are seeing relatively stagnant wage growth, and this likely won’t improve as rents keep climbing, Zillow noted.

Renters are not only missing out on a chance to lower their housing expenditure and build equity, but they are also unable to save up for a potential down payment on a home, and they are even putting retirement planning and health care on the back burner as they struggle to afford their rising rent payments, Zillow said.

“There are good reasons to rent temporarily — when you move to a new city, for example — but from an affordability perspective, rents are crazy right now. If you can possibly come up with a down payment, then it’s a good time to buy a home and start putting your money toward a mortgage,” said Zillow Chief Economist Dr. Svenja Gudell.

Mortgage payments will continue to be affordable, even if mortgage rates rise as expected, Zillow predicted. If rates reach 6 percent next year, homebuyers can still expect to spend 30 percent or less of their income on mortgage payments in 91.4 percent of the metros Zillow analyzed, and mortgage payments will be considered more affordable than in prebubble years in 72.1 percent of metros.