Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Homes are sitting on the market longer than they have in years, and it’s not just high mortgage rates that are to blame. According to a new Redfin report, concerns over affordability, economic uncertainty and tariff threats under a second Trump administration are giving buyers serious pause.

TAKE THE INMAN INTEL SURVEY FOR APRIL

As of March, the typical U.S. home took 47 days to sell, the longest stretch in six years. Those longer stretches on the market tend to discourage competition, often signaling buyers to either wait or negotiate.

Redfin analysis of MLS data

Redfin Senior Economist Elijah de la Campa says that sellers must lower their expectations to adapt to today’s market.

Elijah de la Campa | Redfin Senior Economist

“There’s a growing disconnect between what sellers think they can get for their homes and the direction the market is actually moving,” Redfin Senior Economist Elijah de la Campa said in a statement. “Tariff fears and widespread economic uncertainty are making homebuyers nervous, so if sellers don’t lower their price expectations, home sales may slow in the coming months.”

The hesitation is showing up most sharply in Fort Lauderdale, Florida, where homes spent 88 days on the market, up 24 days from the previous year. Miami and West Palm Beach, Florida, followed with increases of 19 days each on the market. San Francisco was the only metro where Days on Market decreased — though only by one day.

Even as demand slows, inventory is climbing, which could cool price growth in the months ahead. Active listings in March rose 0.1 percent month over month and 14.1 percent year over year, reaching the highest level in five years. New listings also climbed 0.7 percent month over month and 6 percent year over year.

The largest inventory gains were seen in Oakland, California (38.4 percent), Denver (37.7 percent) and Las Vegas (32 percent), while new listings grew fastest in Los Angeles (23.5 percent), Boston (23.4 percent) and Anaheim, California (23.3 percent).

Houston-based Redfin Premier agent Alicia Grifaldo has noticed the shift firsthand as many pandemic-era homebuyers re-enter the market.

“Many people who bought homes in 2021 and 2022 are selling now, some of them because they can’t afford their property taxes and insurance payments. Because they bought at the peak of the market, they’re overpricing their homes to try to recoup their investment,” she said. “Sellers are competing with one another, and buyers are sparse, so pricing your listing reasonably is everything right now.”

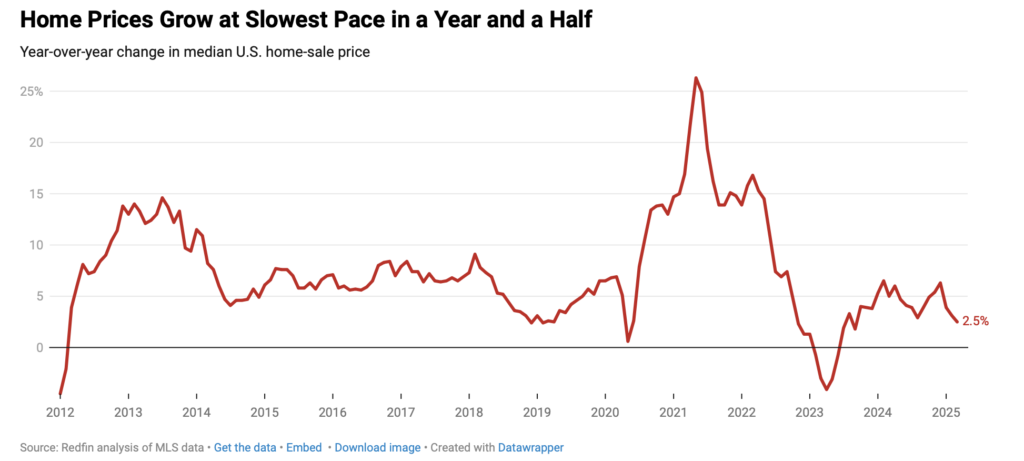

That pricing mismatch is reflected in the numbers. In March, the median home-sale price was $431,057, a modest 2.5 percent increase from the previous year and the slowest pace of price growth since September 2023. However, list prices are rising faster than sale prices, which is a sign that sellers are still hoping to push for more than the market is willing to give.

Redfin analysis of MLS data

However, the market is pushing back. The typical home that sold in March closed for about 1 percent below its list price.

Price trends varied widely by region, with the biggest increases in Cleveland (11.8 percent), Nassau County, New York (9.8 percent) and Newark, New Jersey (9.5 percent). The largest decreases were seen in Jacksonville, Florida (-3.8 percent), San Francisco (-2.6 percent) and Austin (-1.6 percent).

Sales activity also sent mixed signals. Pending home sales rose 1.7 percent month over month in March, but closed sales and existing sales fell by roughly 1 percent, remaining below pre-pandemic levels.

Pending sales grew the most in Montgomery County, Pennsylvania (13.7 percent), Denver (6.9 percent) and Sacramento, California (5.7 percent). Closed sales rose most in San Francisco (13 percent), Oakland (11.7 percent) and New York (5.3 percent).

One major headwind remains: mortgage rates. While the average 30-year-fixed mortgage rate dipped 6.65 percent in March, it’s still more than double the record lows seen during the pandemic, and that is keeping many buyers on the sidelines.