The median U.S. homebuyer’s down payment has fallen for the first time in nearly two years, according to data released Monday by Redfin.

The 1 percent drop, to $62,468, is subtle but significant, according to the report, which tracked county records in the 40 most populous metro areas in the U.S.

“The buyers who are moving forward today are being very careful with their finances because with housing costs near record highs, they’re typically spending a big portion of their paycheck to buy a home,” Redfin Premier agent Fernanda Kriese, who is based in Las Vegas, said in the report.

“I’m seeing an uptick in first-time buyers looking for starter homes,” Kriese added. “Combine that with concerns about layoffs and a potential recession, and people are doing things like cross-comparing mortgage origination fees, shopping around for lenders and looking into down-payment assistance.”

Credit: Redfin

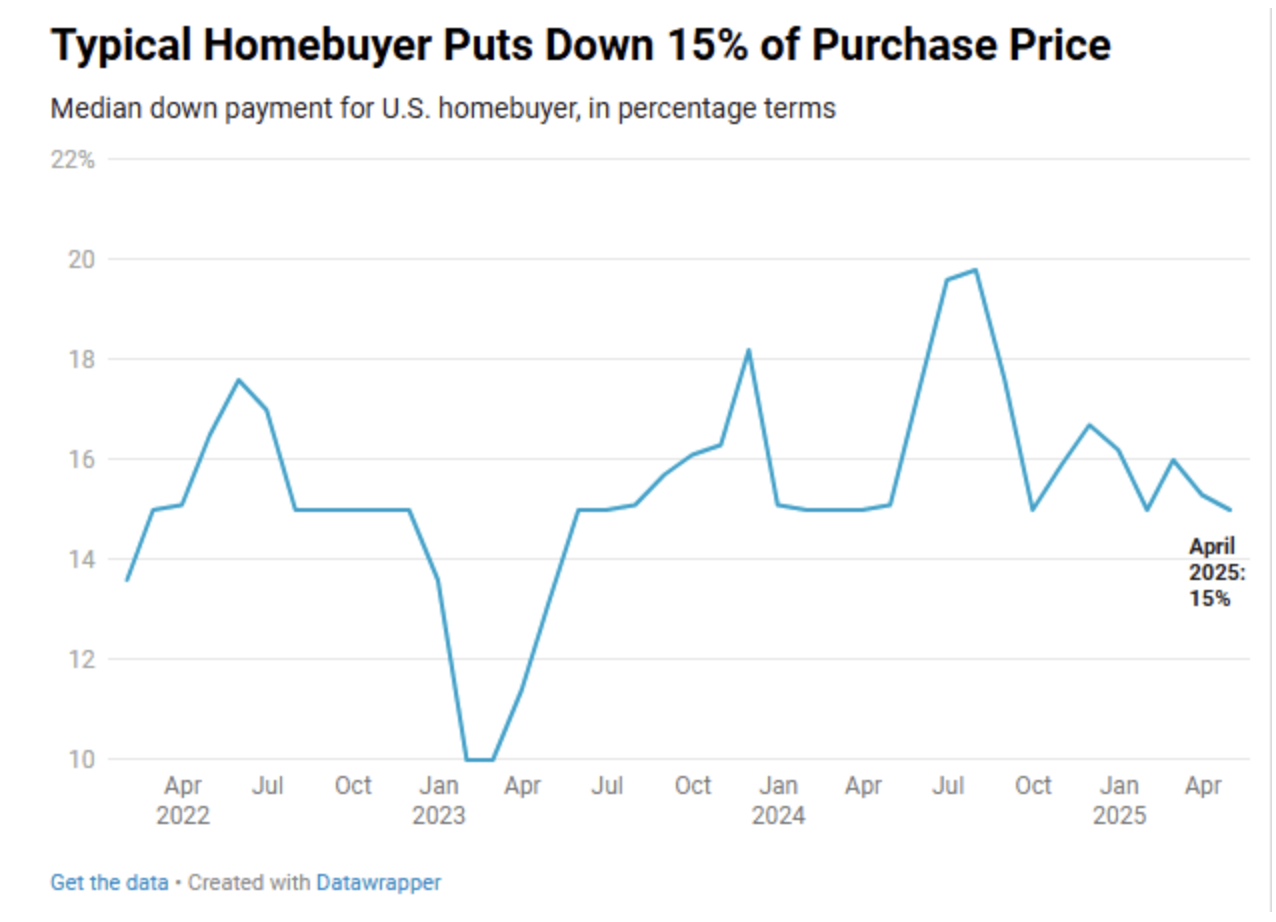

In terms of percentage, the typical homebuyer today puts down 15 percent of the purchase price, nearly equal to the 15.1 percent they put down at this time last year, Redfin’s report noted. And the median down payment for American homebuyers has hovered around that number for about the last four years, briefly dipping around 10 percent in early 2023. Pre-pandemic, a 10 percent down payment was more frequent.

But dollar-amount down payments have not fallen on an annual basis since the summer of 2023 when home-sales prices were also falling, according to Redfin. During that period, down payments were declining because of falling home prices.

Now, home prices are rising, although they are doing so more slowly. As of April, home prices were up 1.4 percent year over year, compared to the 4 percent they were up by during the same period in 2024.

The reason down payments are falling by dollar amount is because not all homebuyers make a down payment — one-third pay in all cash. And those that are financing a home are most likely buying less expensive homes, which also means a smaller down payment in terms of dollars, but not necessarily percentage terms.

Redfin said that a higher share of homebuyers are also using FHA and VA loans, which allow for smaller down payments, somewhere between 0 percent to 3.5 percent. In April, 15.3 percent of mortgage home sales used an FHA loan, up from 14.2 percent the year before. The share of mortgage home sales using a VA loan was 7.2 percent in April, up from 6.4 percent the year before and the highest April level seen since 2020.

With homebuyer affordability remaining difficult because of roughly 7 percent mortgage rates, many buyers may be purchasing lower-priced homes than they might otherwise. Economic uncertainty in the U.S. right now may also be driving buyers to reserve more of their money in their bank accounts for extenuating circumstances.

Meanwhile, there are now more homesellers than homebuyers in the U.S., tipping the market to favor buyers, which has meant concessions and sellers willing to accept lower down payments. Unfortunately, lower down payments might also be a sign of a buyer with less secure financial standing, and a deal that’s more likely to fall through.