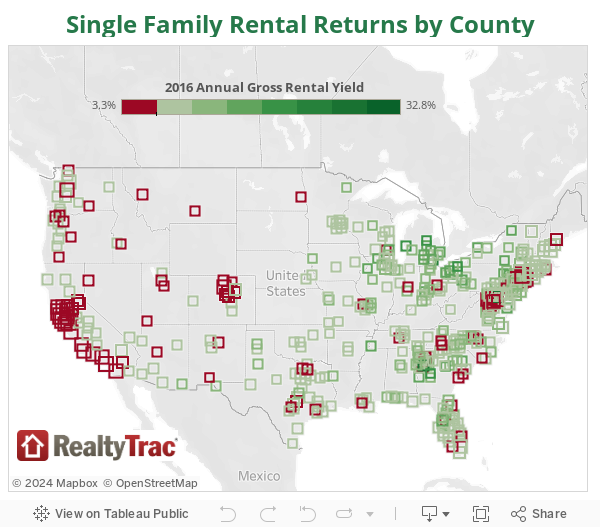

- Some of the nation’s most expensive for-sale markets trail the national average in single family rental returns.

- Home values outpace rents in 55 percent of the markets analyzed, which generally indicates a lagging rental market as compared to homeownership, yet wage growth surpasses rents in 43 percent of markets.

Rapidly rising home values combined with low national wage growth is thwarting profitability on single-family investment properties in markets like San Francisco, New York City and D.C.

Some of the nation’s most expensive for-sale markets trail the national average in single family rental returns, according to RealtyTrac’s first-quarter single-family rental market investing report.

Across the U.S., investors gross an average 9.4 percent rental revenue — a drop from 9.5 percent in the first quarter of 2015.

Home values outpace rents in 55 percent of the markets analyzed, which generally indicates a lagging rental market as compared to homeownership, yet wage growth surpasses rents in 43 percent of markets. RealtyTrac senior vice president Daren Blomquist suggests wage increases gives potential for yields on single-family investments down the road.

“More important than rent growth, although that does indicate demand, the key to me is wage growth. If you have the wage growth, then that’s an opportunity to raise rents in the future. And therefore, receive higher returns off rentals,” he said. “The rent growth is probably secondary — although still an important factor because it indicates pressure of demand is greater than supply, which is pushing the rents up.”

Buyer (and investor) beware: expensive coastal counties generate lowest returns

The lowest single-family returns are in Arlington County in the D.C. metro area, with 3.3 percent returns. In D.C., rent growth is not outpacing wage growth nor home price growth, but home values are on the higher end with a median sales price of $775,000. Average weekly wage growth is low at just 2.7 percent year-over-year, and 3-bedroom rent rates grew only 1.8 percent since last year.

San Francisco County came in second-to-last with just 3.4 percent yields. Rent growth for 3-bedrooms somewhat surprisingly beat home price growth, although slightly by 7.3 versus 7 percent.

As Blomquist notes, wages play a primary part in filling single-family rentals than rent growth alone. Rent growth outpaced wage appreciation in San Francisco County, which was a mere 1.5 percent.

Brooklyn landed toward the bottom of lowest single-family rental returns with just 4 percent average yield, down from 4.7 percent year-over-year. Rent growth did not outpace wage growth in Kings County.

“They [Kings County, San Francisco] are such high priced markets, it’s hard to have a rental property that gets a good return on that. It’s not necessarily that those are bad markets to buy properties, you just can’t expect to be getting a big return on rents,” said Blomquist.

In San Mateo, Marin, Santa Cruz and Santa Cruz, all within the Bay Area, single-family investors pulled average profits of 3.6 percent, 3.9 percent, 4 percent and 4 percent, respectively.

With the exception of Santa Cruz, all of the California markets above featured greater rent growth compared to wage growth.

“Probably more of the investor play is a combination of the rental income, and mostly the appreciation over time of that property,” said Blomquist. “If that’s you’re going for monthly cash flow, you’re not going to get that buying in Brooklyn or San Francisco – or in a lot of areas of DC., either.”

Where can single-family landlords profit?

In terms of counties, Baltimore City, Maryland, has the highest annual gross rental yield at 28.5 percent. The median sales price rose 6.1 percent last year to reach $70,000. Despite the home price rise, wages grew 2.4 percent. Moreover, 3-bedroom rent prices grew 5.7 percent year-over-year.

De Kalb County in the Chicago metro area has 11.3 percent annual gross rental yield and 8.9 percent annual wage growth. For rental returns profit, De Kalb county comes in at 85th in the country.

What’s more, 60419 in Cook County yields 51.1 percent annual gross profit, where the median sales price was $32,350 in the first quarter of 2016.

“Within one market there’s a lot of variance. In a market like Chicago, you’re going to find those lower priced properties. On paper, the returns can be very good. But you also have to look at the other factors, in terms of the neighborhood quality and the economy,” said Blomquist.

Miami metro ZIP hits lowest in nation

While Miami-Dade County managed to pace with national averages for potential single family rental returns at 8.4 percent, and rents rose 4 percent year-over-year, one zip in the Miami metro area is one of the lowest potential single family returns for 2016.

Second to last, 33480 in the Miami metro area had 0.6 percent potential single family rental returns for 2016, just behind 34102 in Naples. The other three ZIPs, 90210 at 0.9 percent potential growth, 90069 at 1.0 percent potential growth and 90402 at 1.1 percent potential growth, are all within the Los Angeles metro.

“South Florida and Miami — of all the markets in Florida — have the most outside buyers coming in propping up prices. You have to be picky and work harder in the Miami market to find good returns,” Blomquist said. “You’re not going to get a good return on rentals unless its a specialized group who are willing to pay potentially tens of thousands per month.”

When do high home values stop helping and start hurting the rental market?

HomeUnion, an online real estate investment company, released data this week revealing median investment home prices increased 5.1 percent year-over-year versus traditional, owner-occupied homes, which increased just 1.1 percent. While RealtyTrac did not differentiate between owner-occupied and investment home prices in its report, the average gross rental yield drop from 2015 could also be related to higher prices in the investment home category on a more narrow scope.

Overall, lagging profit in markets like San Francisco, Brooklyn, D.C. and parts of Miami is largely related to high home values that don’t reap large monthly returns on rentals. Nonetheless, the investment market is still a culmination of factors with ups and downs depending on how you position it, according to Blomquist.

“If home prices are rising faster than rents, that would actually be pushing more people to rent. For the most part, but on the downside as an investor, prices are rising faster which makes it tougher to acquire properties as rentals,” said Blomquist. “It’s a delicate balance. Ideally you want wages to outpacing rent growth and home price growth, but that’s not happening very often.”