We’ll add more market news briefs throughout the day. Check back to read the latest.

Most recent market news

Tuesday, June 27

- The 30-year fixed mortgage rate on Zillow Mortgages is currently 3.67 percent, down one basis point from this time last week. The 30-year fixed mortgage rate rose to 3.71 percent on Friday, then hovered there before falling to the current rate on Tuesday.

- The rate for a 15-year fixed home loan is currently 2.95 percent, while the rate for a 5-1 adjustable-rate mortgage (ARM) is 2.96 percent.

- Below are current rates for 30-year fixed mortgages by state.

“Mortgage rates were flat last week and we expect the relative calm to continue leading up to the Fourth of July holiday,” said Erin Lantz, vice president of mortgages at Zillow. “Lenders are likely to price conservatively going into the holiday weekend. A couple of Fed speeches midweek could push small movements in rates, but overall we expect another quiet week.”

- The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported a 5.5 percent annual gain in April, down from 5.6 percent last month.

- The 10-City Composite annual increase came in at 4.9 percent, down from 5.2 percent the previous month.

- The 20-City Composite posted a 5.7 percent year-over-year gain, down from 5.9 percent in March.

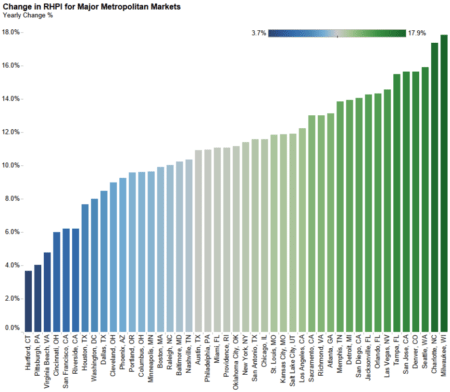

- Seattle (12.9 percent), Portland (9.3 percent) and Dallas (8.4 percent) reported the highest year-over-year gains among the 20 cities.

“As home prices continue rising faster than inflation, two questions are being asked: why? And, could this be a bubble?” said David M. Blitzer Managing Director and Chairman of the Index Committee at S&P Dow Jones Indices. “Since demand is exceeding supply and financing is available, there is nothing right now to keep prices from going up. The increase in real, or inflation-adjusted, home prices in the last three years shows that demand is rising. At the same time, the supply of homes for sale has barely kept pace with demand and the inventory of new or existing homes for sale shrunk down to only a four- month supply. Adding to price pressures, mortgage rates remain close to 4% and affordability is not a significant issue.”

CoreLogic Housing Credit Insights, Q1 2017

- In Q1 2017 the HCI increased to 105.6, up 3.6 percent from the prior year. While underwriting slightly loosened, the underlying risk factors in Q1 remain in the same range as the last four years when loans exhibited very good mortgage performance.

- The slight loosening in the credit index was partly due to a shift in the mix of loans to purchase originations which exhibit higher risk than refinances.

- The average credit score for homebuyers increased 7 points year over year between Q1 2016 and Q1 2017, rising from 734 to 741.

- Holding steady at 36 percent, the average DTI for homebuyers in Q1 2017 was similar to Q1 2016.

- The LTV for homebuyers fell by 1.7 percentage points between Q1 2016 and Q1 2017 from 87.6 percent to 85.9 percent.

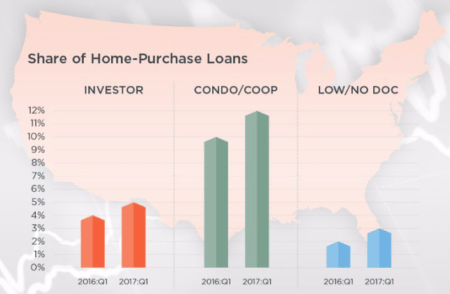

- The investor share of home-purchase loans increased from 4 percent in Q1 2016 to 5 percent in Q1 2017, and the share of home-purchase loans secured by a condominium or a co-op building increased from 10 percent in Q1 2016 to 12 percent in Q1 2017.

- The five states with the highest average original credit score of borrowers was District of Columbia (758), Hawaii (754), New York (750), California (749) and Colorado (749).

- Applications in the lower credit score range are almost non-existent in 2016 when compared to 2006. Applicants may be “self-removing” themselves from the applicant pool. This may explain some of the decline in new-loan credit risk.

“Mortgage rates during the first quarter of 2017 were up about 0.5 percentage points from a year earlier,” said Frank Nothaft, chief economist at Core Logic. “Since 2009, for every one-half percentage point increase in mortgage rates, the average credit score on refinance borrowers has dipped by 9 points, and this pattern will likely continue if mortgage rates move higher. That is because when rates rise, applications drop off and loan officers spend more time with the applicants that have less-than-perfect credit scores, require more documentation or have unique property issues.”

News from earlier this week

Monday, June 26

- Real house prices decreased -1.6 percent between March and April.

- Real house prices increased by 11.0 percent year-over-year

- Consumer house-buying power, how much one can buy based on changes in income and the interest rate, increased 0.4 percent between March and April, and fell 4.5 percent year-over-year.

- Real house prices are 33.6 percent below their housing-boom peak in July 2006 and 10.8 percent below the level of prices in January 2000.

- Unadjusted house prices increased by 5.7 percent in April on a year-over-year basis and are 2.6 percent above the housing boom peak in 2007.

“Despite the monetary tightening policies of the Federal Reserve, a dip in the average rate for a 30-year, fixed-rate mortgage and wage gains increased consumer house-buying power sufficiently to offset the gain in unadjusted house prices. The decline in real, purchasing-power adjusted house prices between March and April was the largest month-over-month decline since July 2016,” said Mark Fleming, chief economist at First American. “While this is welcome news for home buyers, the number of homes listed for sale is not meeting consumer demand and markets are getting tighter. As a result, affordability declined 11 percent on a year-over-year basis. That’s a bigger drop in affordability than the 5.7 percent caused by unadjusted house-price appreciation alone and reflects the impact of rising interest rates and tightening supply.”

Email market reports to press@inman.com.