As more cities push to ditch single-family zoning in an effort to create more affordable housing, the unique New York City housing market is dealing with another issue too: A lot of the new housing built after 2013 is unaffordable for the city’s residents, according to a new study from the Zillow-owned listing portal StreetEasy.

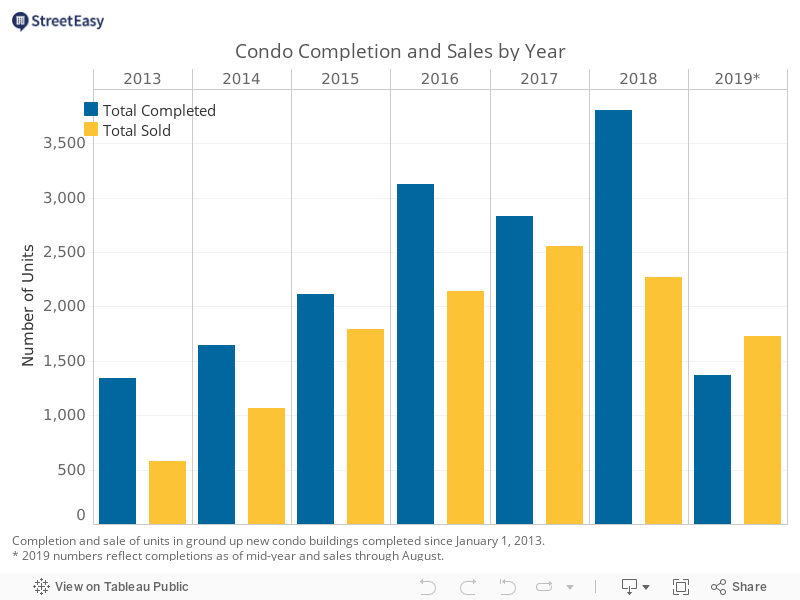

Of the 16,242 new condos built in New York City since the start of 2013, more than 25 percent remain unsold, according to the study.

“New York City has seen a boom in condo building over the last half-decade,” the study reads. “But even as glitzy new units continue to hit the market, a worrying number of homes created in this boom remain unsold.”

This so-called “condo boom” has lined the pockets of developers, producing massive revenue with the total value of condos sold, reaching an estimated $32 billion, according to the study. Among those new developments are some of the most expensive units ever sold, putting the condos out of reach for most New Yorkers.

“Some 4,109 condos, or just over 25 percent of all new stock, remain sitting on the market, forming a backlog that has grown steadily since 2013,” the study says. “And with a median price of $1.1 million citywide, and more than $2.3 million within Manhattan, these new condos remain out of reach of most New York home buyers.”

In the wake of the economic recovery following the recession, with borrowing rates low, the construction of new condos rose precipitously in New York.

An estimated 30 percent of these condos are finding themselves on the rental market, according to StreetEasy, meaning many of the actual sales are going to investors, versus New Yorkers using these homes as their primary residence. The study says that the presence of investors should raise alarms.

“Though evidence suggests that the return on rental income for these purchases is low, many buyers are presumably speculating on their ability to sell the units for higher prices in the future,” the study reads. “But this prospect has darkened further in recent months, as prices on many new condos have tumbled downward.”

“That so many buyers are placing heavy bets on their future ability to sell at a profit raises big questions about the sustainability of the current building boom,” the study continues. “How long do buyers plan to hold on to these condos, and what will happen to prices if too many look to sell at once?”

New York City has undergone a substantial economic recovery since the housing crash, but fears of a coming recession may have people flocking to safer assets or more modest homes, according to StreetEasy. The fact that so many condos remain unsold could also be a harbinger of a future recession or economic slowdown, according to the study.

Still, more condos are on the way. StreetEasy’s study also found that 63 buildings with more than 5,617 units already have listings on StreetEasy but are yet to finish construction.

Reserve your spot at Luxury Connect here. Thinking of bringing your team? There are special onsite perks and discounts for team who register together. Just contact us to find out more.