Homebuyer demand for purchase mortgages slipped last week, even as rates were descending to a new 2025 low, with homeowners seeking to refinance accounting for most applications, the Mortgage Bankers Association (MBA) reported Wednesday.

Although the Fed is expected to continue cutting short-term interest rates this year and next, mortgage rates are unlikely to drop below where they are today, the MBA said in a separate forecast.

The MBA’s Weekly Mortgage Applications Survey showed applications for purchase loans were down by a seasonally adjusted 5 percent last week compared to the week before, but up 20 percent from a year ago.

TAKE THE INMAN INTEL SURVEY FOR OCTOBER

Requests to refinance were up 4 percent week over week and 81 percent from a year ago, accounting for 56 percent of all mortgage applications.

Joel Kan

“The lowest mortgage rates in a month spurred an increase in refinance activity, including another pickup in ARM applications,” MBA Deputy Chief Economist Joel Kan said in a statement. “The 30-year fixed rate decreased to 6.37 percent, and all other loan types also decreased.”

With rates on adjustable-rate mortgage (ARM) loans 80 basis points lower than 30-year fixed rate mortgages, requests for ARM loans were up 16 percent week over week and accounted for 11 percent of applications. A basis point is one hundredth of a percentage point.

Mortgage rates hit new 2025 low

Rates on 30-year fixed-rate conforming mortgages hit a new 2025 low of 6.15 percent on Monday, down 90 basis points from the high for the year of 7.05 percent registered on Jan. 14, according to lender data tracked by Optimal Blue.

At 6.02 percent on Tuesday, rates for FHA loans were near their 2025 low of 5.98 percent registered on Sept. 16.

Eric Hagen

“We’re tracking feeds like Optimal Blue to see if FHA rates cross below 5.75 percent as a key threshold for unlocking both refi and purchase demand,” BTIG analyst Eric Hagen said Wednesday in a note to clients. “Mortgage rates for FHA and VA loans have dropped 25 [basis points] in the last month, roughly in-line with the decline in conventional rates.”

Last year, 30-year fixed-rate mortgages bottomed out at 6.03 percent on Sept. 17, but climbed back above 7 percent when the Fed started cutting short-term rates and inflation flared up.

Central bank policymakers trimmed the federal funds rate by a full percentage point at the end of 2024, and mortgage rates went up by an equal amount as investors in mortgage-backed securities demanded higher yields.

The Fed resumed its easing of monetary policy on Sept. 17 with a quarter percentage point cut in the federal funds rate, the rate banks charge each other for overnight loans. Stephen Miran, a recent Trump appointee to the Federal Reserve Board, was the lone dissenter in the 11-1 vote, holding out for a bigger, half percentage point rate cut advocated by the president.

New worries about regional banks‘ exposure to commercial mortgages, falling oil prices and the continued federal government shutdown have some investors betting that the Fed will be compelled to approve a jumbo rate cut in December, analysts at Pantheon Macroeconomics noted in their Oct. 20 U.S. Economic Monitor.

“Investors are growing more worried that private credit lending standards have been too loose lately and that some regional banks’ capital will be wiped out if their loans to non-bank financial institutions sour,” Pantheon analysts said, citing the International Monetary Fund’s latest Global Financial Stability Report.

That report noted that U.S. and European banks have $4.5 trillion in loans and undrawn commitments to non-bank financial institutions (NBFI), with large regional banks and those with assets under $100 billion facing higher risk exposure.

The recent $10 drop in the price of a barrel of oil should ease inflation by about one-third of a percentage point, adding to the case that the Fed might approve a jumbo 50 basis point rate cut in December, Pantheon economists Samuel Tombs and Oliver Allen said.

Also, with the federal government shutdown “rumbling on with no end in sight,” some investors “seem to be betting a torrent of bad data will be released after the shutdown ends” — potentially just before the Fed’s Dec. 10 meeting, Tombs and Allen said.

But Pantheon is sticking with its forecast that the Fed will cut rates by 25 basis points in October, December, March, June and September, which would bring the federal funds rate down by a total of 1.25 percentage points, to a target range of 2.75 percent to 3 percent.

If more needs to be done, they said, the Fed could do another 25 basis point cut at its January or April meetings, they said.

The Fed doesn’t have direct control over mortgage rates, which are determined by investor demand for mortgage-backed securities (MBS).

With MBS investors having already priced in expectations for the Fed to continue cutting short-term rates, mortgage rates might have little room to keep coming down, MBA economists predicted in an Oct. 19 forecast.

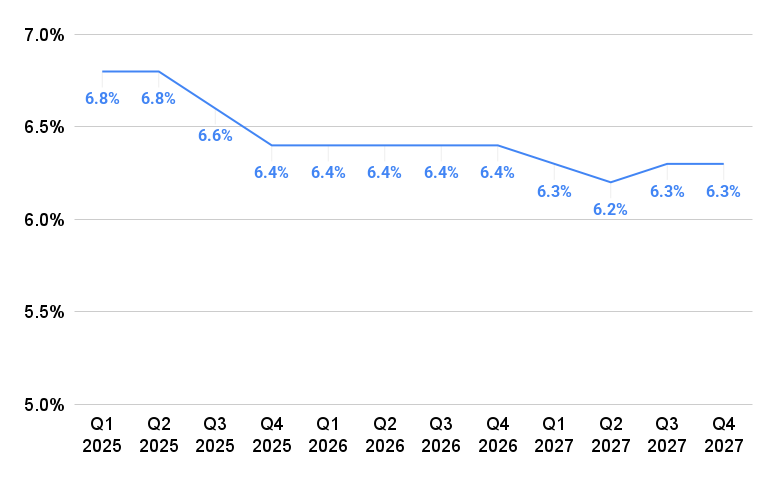

Will mortgage rates plateau?

Source: Mortgage Bankers Association Mortgage Finance Forecast, Oct. 19, 2025

MBA economists expect rates on 30-year fixed-rate mortgages to average 6.4 percent all next year before dipping to 6.2 percent by Q2 2027.

In a Sept. 11 forecast, economists at Fannie Mae were more optimistic about the prospect of lower mortgage rates, projecting rates on 30-year fixed mortgages will drop to 6.2 percent in Q1 2026 and 5.9 percent by Q4 2026. Fannie Mae’s October forecast had not been released to the public as of Wednesday.

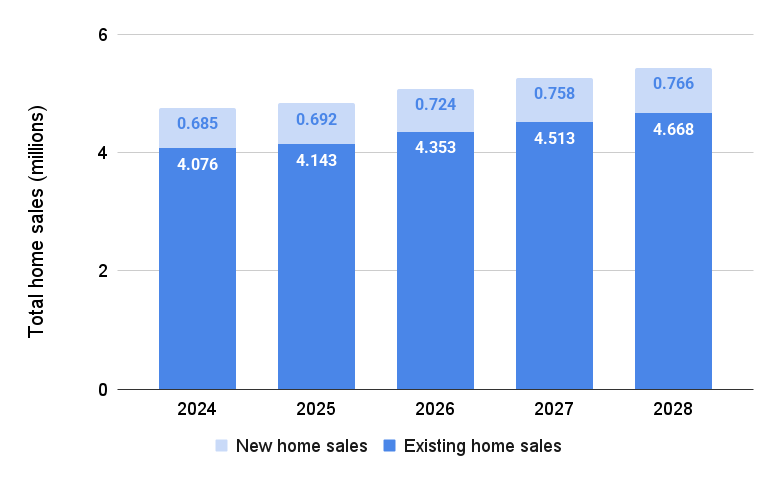

Steady growth forecast for home sales

Source: Mortgage Bankers Association Mortgage Finance Forecast, Oct. 19, 2025

The MBA forecasts home sales will grow 5 percent next year, to 5.08 million, and by another 3.8 percent in 2027 and 3.1 percent in 2028.

Sales of existing homes are projected to hit 4.67 million by 2028, with new home sales growing to 766,000.

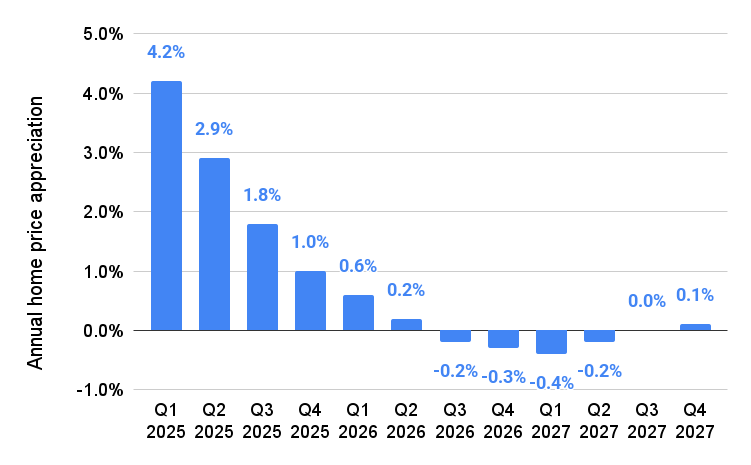

Home price appreciation to turn negative?

Source: Mortgage Bankers Association Mortgage Finance Forecast, Oct. 19, 2025

In addition to elevated mortgage rates, a dramatic surge in home prices during the pandemic has depressed sales. MBA economists expect annual home price appreciation will cool to less than 1 percent in the first half of next year and turn slightly negative until Q3 2027.

Another headwind for home sales has been consumer sentiment, which was down 22 percent from a year ago in October, according to preliminary results from the University of Michigan Index of Consumer Sentiment.

Joanne Hsu

“Pocketbook issues like high prices and weakening job prospects remain at the forefront of consumers’ minds,” Surveys of Consumers Director Joanne Hsu said, in a statement. “At this time, consumers do not expect meaningful improvement in these factors.”

But interviews “reveal little evidence that the ongoing federal government shutdown has moved consumers’ views of the economy thus far,” Hsu said.

Fannie Mae’s most recent National Housing Survey, fielded before the government shutdown between Sept. 2 and Sept. 22, found:

- 27 percent of Americans said it was a good time to buy, up from 19 percent a year ago

- 57 percent said it was a good time to sell, down from 65 percent in September 2024

- 40 percent expected prices to go up over the next 12 months, up from 39 percent a year ago

- 32 percent expect mortgage rates to go down in the year ahead, down from 42 percent a year ago

- 25 percent were concerned about losing their job, up from 22 percent a year ago

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.