- Luxury markets across the country's major metros are still increasing, just not as fast as 2013.

- Overall, luxury housing markets across the globe saw 16 percent sales growth in 2014 and 8 percent growth in 2015.

- In a surprising twist, Jackson Hole, Wyoming landed the number six spot in Christie’s “Luxury Thermometer.

What is the cost of luxury real estate? In New York City, it’s $5 million and up. In Miami, the threshold drops to $2 million. The price of high-end comfort fluctuates across local markets, international borders and, most certainly, years.

So the first thought of slowing sales in the multi million-dollar real estate club might be troublesome, but not so fast.

Christie’s International Real Estate Luxury Defined report says the luxury market across the globe has indeed shifted. While 2013 posted strong sales volume for luxury markets in various cities, pace eased through 2014 and 2015. Sales in the more prominent markets, NYC included, even plateaued into early 2016 due to concerns facing the global economy and political uncertainties.

“Markets like New York rebounded first coming out of the crisis and had meteoric growth for a while,” CEO of Christie’s International Real Estate Dan Conn said. “You can’t have massive double-digit growth numbers and think those can be sustained over time — the numbers get too big.”

Despite the ambiguity of the stock market and oil prices, which Christie’s says recently impacted the buying power of many wealthy individuals who typically invest in luxury real estate across the world, many are likely to continue investing in property as a safe bet.

Comparing the Case-Shiller Home Price Index to the S&P 500 over a 14-year period led Conn to conclude that equities have more volatility than real estate investments.

“While there is a bit of a pause in buying [in New York], the dynamics are still reasonably favorable,” he said. “Real estate is fairly attractive when high net worth investments when they are thinking of portfolio diversification.”

2014 vs. 2015 at a glance

Christie’s separates luxury markets into two categories: primary and resort. Primary markets are your cities and pricey suburban towns, while resort markets are lifestyle destinations with populations under 500,000.

Sales in primary markets grew 9 percent in 2014 and 7 percent in 2015. Resort markets pumped the breaks a little harder, with 24 percent growth in sales in 2014 and only 10 percent growth in sales in 2015.

Still, while both experienced declines from previous years, overall growth means the sky hasn’t started to fall yet.

Overall, luxury housing markets across the globe saw 16 percent sales growth in 2014 and only 8 percent growth in 2015 — half the growth, but still a solid year-over-year lift.

U.S. luxury sales growth tapers in top markets

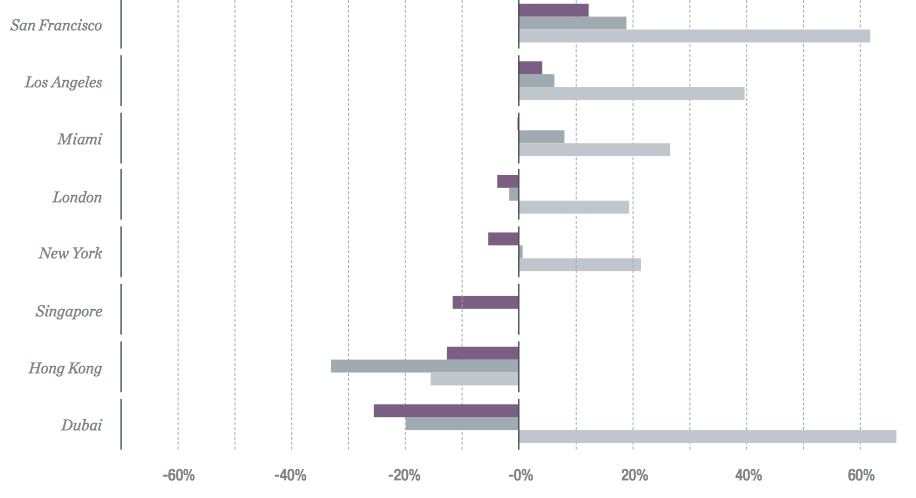

In 2013, San Francisco posted 62 percent year-over-year growth on luxury home sales (categorized as $1 million and up), still accelerating rapidly off the tailwinds of the housing crisis. In 2014, sales growth in the high-end tier dropped to 19 percent. San Francisco’s luxury home sales growth was 12 percent last year.

Not pictured above San Francisco (ascending order): Toronto, Paris and Sydney

San Francisco came in at no. 5 on hottest luxury housing markets due to strong interest from international and local buyers alike.

Los Angeles grew by 5 percent in 2015, far below 2013, when the market had almost 40 percent growth in luxury home sales. But, L.A. benefitted from 82 sales above $10 million in 2014 and 2015 combined.

“Five years ago, I wouldn’t have said L.A. was the center of the road map in terms of the super-high-end trophy properties, but prices weren’t trading like in New York,” Conn said. “Now, six out of 27 properties over $100 million worldwide are in L.A..”

Miami luxury sales were robust in 2013, revealing over 30 percent growth. Then in 2014, luxury sales slowed to under 10 percent and in 2015, year-over-year sales fell below the previous year’s figures.

Over the past few years, luxury development soared in Miami. But a sharp decline in international demand due to a strengthening U.S. dollar left supply to sit. For Brazil, the U.S. exchange rate soared 35 percent between Jan. 2015 and March 2016. For Mexico, the exchange rate rose 17 percent.

“When Miami peaked, the market was at 40 percent foreign buyers. It’s now at 33 percent. If you’re taking away 7 percent of your demand, sales volume is going to be affected,” Conn said.

New York’s high-end annual growth fell last year, and Big Apple real estate was quickly branded as troubled. In 2013, NYC had over 20 percent luxury home sales growth, and in 2014, growth stabilized at just over 0 percent year-over-year.

But as leading Manhattan brokers substantiate, Manhattan’s slowing sales pace isn’t due to lack of demand, but rather, oversupply.

Over 6,500 homes came on the market in 2015 in NYC, the largest flood of units since before 2008. Much of the supply fell into the super luxury category, allowing Manhattan’s median price to skyrocket and simultaneously slowing the sales of apartments over $10 million by 14 percent.

Picking up the speed in unexpected places

In a surprising twist, Jackson Hole, Wyoming landed the number six spot in Christie’s “Luxury Thermometer,” as more domestic buyers find this resort retreat a good place to invest in secondary or retirement properties. Sales increased in Jackson Hole 45 percent last year.

Portland also made the list at no. 8, with wealthy tech buyers flocking to the Pacific Northwest — although inventory still remains an issue, Conn says.

Growth pace aside, the four U.S. cities synonymous with grandeur still topped the 10 most luxurious cities worldwide: NYC (3), L.A. (4), Miami (7) and San Francisco (8).

The top 10 most luxurious markets are defined by the Luxury Index and the Luxury Thermometer, or the health of the $1 million-plus market, which compares both primary and resort housing markets.

“If you consider the variables — exchange rates, the global economy, etc. — and compare those to the growth numbers, they look even better,” Conn said. “You have all of these headwinds, yet still see a decent market.”