- NAR wants Congress to extend the National Flood Insurance Program beyond its September 2017 expiration date.

- The association also wants to ban guarantee fees, place restrictions on energy efficiency loans and "responsibly reform our nation's secondary loan market."

- Tax reform is needed, but NAR says it "must not dilute the current real estate tax provisions vital to the housing market and the economy."

What kind of influence could 1 million Realtors have if they all spent a few minutes to contact their legislative representatives about the same key issues?

The National Association of Realtors (NAR) has just unveiled its three main legislative talking points for the 2017 Realtors Legislative Meetings & Trade Expo, which starts May 15 and continues through May 20 in Washington, D.C.

These are the issues that NAR is hoping that expo attendees and their colleagues at home will raise with legislators — issues that could affect homeownership now and for years to come.

National Flood Insurance Program

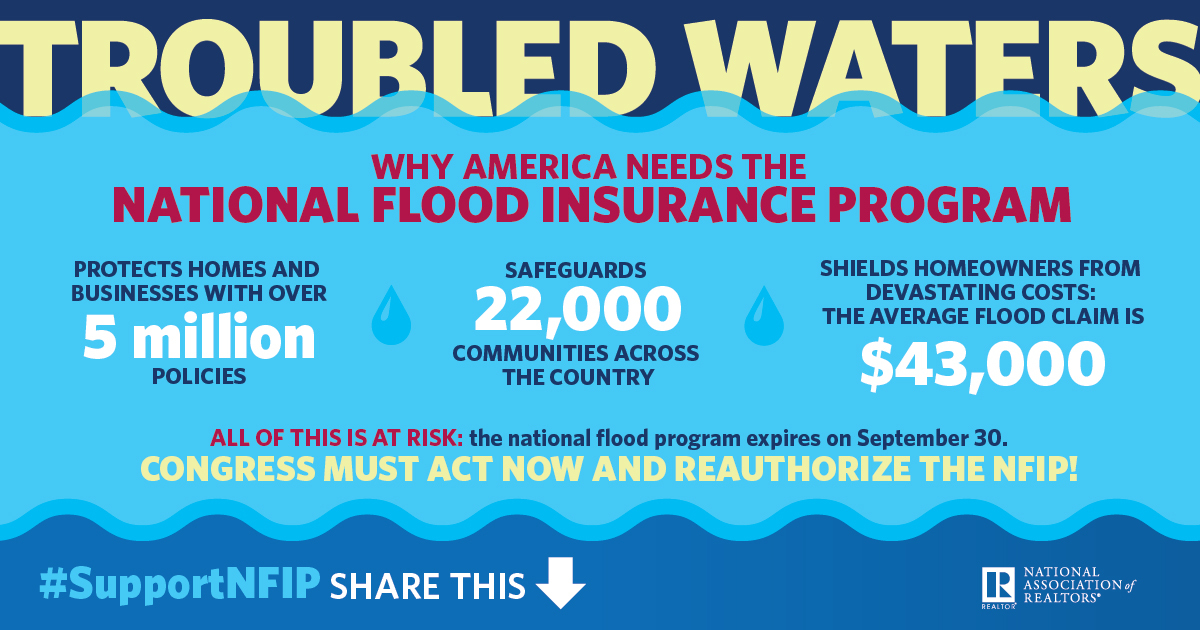

The National Flood Insurance Program (NFIP), which was created in 1968, was crafted to “reduce the impact of flooding on private and public structures,” according to the program’s official government website.

“It does so by providing affordable insurance to property owners and by encouraging communities to adopt and enforce floodplain management regulations,” the website adds.

That could disappear on September 30, which is when the NFIP is set to expire. NAR does not want that to happen.

A Facebook infographic that NAR put together about the National Flood Insurance Program.

The association is asking members to “urge Congress to pass a multiyear reauthorization with needed private market reforms to avoid adding uncertainty to real estate markets.”

Talking points include:

- “Long-term reauthorization is critical” — NAR says that “each lapse costs 40,000 property sales per month” and that without reauthorization, 22,000 communities where flood insurance is required for a mortgage could find themselves without any available flood insurance policies.

- “Accurate flood maps are essential” — “The current method of flood mapping and amendment is inefficient,” NAR says; it wants members to encourage NFIP to “use modern mapping technology to produce building-specific risk assessments.”

- “Risk mitigation keeps rates affordable” — $1.4 billion a year is spent on grants to property owners to repair flood damage, NAR says, and “mitigating, elevating or relocating these properties would save taxpayers $4 for every $1 spent.” The association also encourages NFIP to change rules that say property owners can’t access mitigation grant dollars until after the property floods.

- “Private market options must be included” — “There is a considerable and growing private market that is offering better coverage at a lower cost than the NFIP,” NAR says, and proposes allowing homeowners to meet federal requirements with a private market insurance plan.

On the other hand, why should the NFIP be allowed to lapse? NAR gave these “opposing viewpoints” and suggested responses to them.

Why is the federal government involved in flood insurance, anyway? Shouldn’t we privatize the NFIP?

NAR doesn’t believe that the private market could guarantee access to affordable flood insurance for all 5 million NFIP policies.

Why does NFIP map floods, anyway? Can’t the private sector do that?

NAR responds that “the current maps are developed by the private sector” and that without any maps, we wouldn’t know where to build, lend or buy properties.

Won’t private insurers “cherry-pick” the low-risk properties from NFIP?

“The private market is targeting high-risk, subsidized properties that are net revenue losers for the NFIP,” responds NAR.

Why should we invest taxpayer dollars into flood-prone properties?

It’s a little late to be asking this question, is the essential response — at this point it’s not a question of whether we’ll spend money on flood-prone properties but how much we’ll spend. “U.S. taxpayers are already spending billions on repairing flooded properties,” NAR notes, “and elevating or relocating those properties would be more cost effective.”

Sustainable homeownership

Another legislative focus for the association this year is the mortgage market and energy-efficiency loans.

NAR is requesting Congressional action on the secondary mortgage market “to ensure that the qualified borrowers have access to safe, affordable mortgage financing.” It’s also urging Congress to “ban the use of mortgage guarantee fees to offset the cost of legislation unrelated to housing” and to apply consumer protection laws to loans that are used to pay for energy efficiency home improvements.

Talking points include:

- “Responsibly reform our nation’s secondary mortgage market” — NAR states that “the current conservatorship of Fannie Mae and Freddie Mac is unsustainable” and asks the government to refrain from dismantling them “without identifying a viable replacement” or omitting “an explicit federal guarantee.”

- “Ban the use of guarantee fees as a Congressional piggybank” — Lenders are charged guarantee fees, or “g-fees,” to guarantee principal and interest payments on mortgage-backed securities. “G-fees are passed on to consumers in the form of higher interest rates,” NAR says, noting that Congress has proposed increasing these fees to pay for things like tax cuts or transportation spending. The association urges constituents to “strongly oppose” the use of g-fees “for any use other than housing.”

- “PACE loans should not hurt the very homeowners they aim to help” — Property assessed clean energy, or PACE, loans are intended to help homeowners improve energy efficiency. “However, consumers are unable to make prudent housing decisions due to the lack of proper consumer disclosures,” states, NAR, and wants Congress to make these PACE loans “subject to the same consumer disclosure laws that apply to mortgages.”

What are some counterarguments to these talking points? NAR offered these opposing viewpoints and responses.

Won’t free-market competition provide better pricing and access to credit for consumers than Fannie Mae and Freddie Mac?

“A purely private mortgage market may provide these benefits, but only for a select few,” rebuts NAR.

But g-fees are necessary to lower the budget deficit — we need every possible source of revenue!

“Deficit reduction should not be done on the backs of middle-class homebuyers,” responds NAR, also stating that diverting this revenue is problematic for the “safety and soundness of the U.S. housing market.”

Are the problems with PACE loans really that bad — and aren’t some of those financial decisions offset with lower utility bills and more energy-efficient homes?

Not every homeowner with a PACE loan got the full details of the terms of that loan when they took it out, responds NAR — and because of that, “there are homeowners with PACE loans who are in trouble.”

Tax reform

Did you think NAR had said everything it had to say about tax reform? Not quite!

“Members of Congress and their staffs need to be reminded that tax reform must not dilute the current real estate tax provisions vital to the housing market and the economy,” state the talking points. “We need tax reform, but it must first do no harm.”

Talking points include:

- “Homeowners must be treated fairly in tax reform” — NAR cites analysis from PricewaterhouseCoopers (PwC) of “a blueprint-like tax reform plan,” which shows that homeowning families with incomes between $50,000 and $200,000 a year would face average tax hikes of $815 in the year after enactment. Conversely, non-homeowning families in the same income range would see an average $516 tax cut. “Homeowners already pay 83 percent of all federal income taxes, and this share would go even higher under similar reform proposals,” NAR states.

- “We must reverse the decline in first-time homebuyers” — In 2016, the homeownership rate was at a 50-year low, notes NAR, and states that limiting interest and property tax deductibility would discourage homeownership rather than encourage it.

- “We cannot afford another housing crash” — “Proposals limiting tax incentives for homeownership would cause home values everywhere to plunge,” NAR stated. PwC analysis estimated that “values could fall in the short run by more than 10 percent if a blueprint-like tax reform plan were enacted,” and that high-cost areas could see more significant value drops than 10 percent. We all know what this leads to: underwater mortgages, defaults, foreclosures and short sales.

- “Like-kind exchanges must be preserved” — We aren’t yet sure what would happen to Section 1031 under the proposed tax reform. Currently, 1031 exchanges “encourages growth by permitting real estate held for investment to be exchanged for property of a like kind on a tax-deferred basis,” and eliminating them could stifle commercial real estate growth (including multifamily growth), according to NAR.

There are a lot of reasons why tax reform could be good for real estate, too — to which NAR offers these rebuttals.

The proposed tax code is simpler, which is better for housing. And the mortgage insurance deduction (MID) disproportionately benefits high-income homeowners right now, so why not eliminate it?

“Eighty-eight percent of those claiming MID earn less than $200,000” responds NAR. “Limiting or repealing current housing tax incentives would hurt the housing sector and unfairly harm homeowners who already pay 80-90 percent of all federal income tax.”

Getting rid of state and local tax deductions will help streamline governments and eliminate subsidies for high taxes — that’s a good thing, right?

Getting rid of property tax deductions, however, “would unfairly cause double taxation of the same income,” responds NAR.

Itemized deductions complicate the tax system — won’t getting rid of them simplify everything?

“The small reduction in complexity achieved by raising the standard deduction would come at too high a price,” NAR rebuts. That price is “the loss of tax incentives for owning a home.”

Those 1031 like-kind exchanges are just loopholes for people who are wealthy enough to have an investment property. How can getting rid of them hurt?

Cutting back or repealing the provision would be bad for economic growth and job creation, responds the association.