We’ll add more market news briefs throughout the day. Check back to read the latest.

Most recent market news

Thursday, January 4

Freddie Mac Primary Mortgage Market Survey

- 30-year fixed-rate mortgage (FRM) averaged 3.95 percent with an average 0.5 point for the week ending January 4, 2018, down from last week when it averaged 3.99 percent. A year ago at this time, the 30-year FRM averaged 4.20 percent.

- 15-year FRM this week averaged 3.38 percent with an average 0.5 point, down from last week when it averaged 3.44 percent. A year ago at this time, the 15-year FRM averaged 3.44 percent.

- 5-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) averaged 3.45 percent this week with an average 0.4 point, down from last week when it averaged 3.47 percent. A year ago at this time, the 5-year ARM averaged 3.33 percent.

“Treasury yields fell from a week ago, helping to drive mortgage rates down to start the year,” said Freddie Mac’s deputy chief economist Len Kiefer.

“The 30-year fixed-rate mortgage fell 4 basis points from a week ago to 3.95 percent in the year’s first survey. Despite increases in short-term interest rates, long-term interest rates remain subdued.

“The 30-year mortgage rate is down a quarter of a percentage point from where it was a year ago and the spread between the 30-year fixed and 5/1 adjustable rate mortgage is the lowest since 2009. With the FOMC minutes showing continued support for gradual increases in policy rates from many participants and inflation rates remaining low, there isn’t much upward pressure on long-term rates at the moment. Whether that changes due to a tighter labor market and the economic impact of tax reform remains to be seen.”

Wednesday, January 3

- The 30-year fixed mortgage rate on Zillow Mortgages is currently 3.75 percent, down three basis points from this time last week.

- The 30-year fixed mortgage rate hovered around 3.80 percent for most of the last week before dipping to the current rate today.

- The rate for a 15-year fixed home loan is currently 3.15 percent, and the rate for a 5-1 adjustable-rate mortgage (ARM) is 3.33 percent.

- The rate for a jumbo 30-year fixed loan is 4.01 percent.

Current rates for 30-year fixed mortgages by state. Source: Zillow

“Mortgage rates were flat during the holiday-shortened week with markets very quiet between Christmas and New Year’s,” said Aaron Terrazas, senior economist at Zillow.

“The relative tranquility of the past two weeks should continue this week, even after Friday’s December jobs report. By most expectations, the employment data due Friday should show a strong U.S. labor market and keep expected interest rate hikes on track for the rest of 2018.”

News from earlier this week

Wednesday, January 3

Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey

- The Market Composite Index, a measure of mortgage loan application volume, decreased 2.8 percent on a seasonally adjusted basis from two weeks earlier. On an unadjusted basis, the Index decreased 42 percent compared with two weeks ago.

- The Refinance Index decreased 7 percent from two weeks ago.

- The seasonally adjusted Purchase Index increased 1 percent from two weeks earlier.

- The unadjusted Purchase Index decreased 40 percent compared with two weeks ago and was 3 percent higher than the same week one year ago.

- The refinance share of mortgage activity increased to 52.0 percent of total applications from 51.8 percent the previous week. The adjustable-rate mortgage (ARM) share of activity decreased to 5.3 percent of total applications.

- The FHA share of total applications increased to 10.4 percent from 10.3 percent the week prior.

- The VA share of total applications increased to 11.2 percent from 10.6 percent the week prior.

- The USDA share of total applications increased to 0.8 percent from 0.7 percent the week prior.

- The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($424,100 or less) remained unchanged from the week prior at 4.25 percent, with points increasing to 0.36 from 0.35 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans. The effective rate increased from last week.

- The average contract interest rate for 30-year fixed-rate mortgages with jumbo loan balances (greater than $424,100) decreased to 4.13 percent from 4.21 percent, with points increasing to 0.21 from 0.20 (including the origination fee) for 80 percent LTV loans. The effective rate decreased from last week.

- The average contract interest rate for 30-year fixed-rate mortgages backed by the FHA increased to 4.17 percent from 4.15 percent, with points increasing to 0.40 from 0.37 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

- The average contract interest rate for 15-year fixed-rate mortgages decreased to 3.65 percent from 3.66 percent, with points decreasing to 0.34 from 0.37 (including the origination fee) for 80 percent LTV loans. The effective rate decreased from last week.

- The average contract interest rate for 5/1 ARMs decreased to 3.40 percent from 3.56 percent, with points increasing to 0.73 from 0.46 (including the origination fee) for 80 percent LTV loans. The effective rate decreased from last week.

Tuesday, January 2

Mortgage rate forecasts for 2018

Here are several predictions from the largest housing and mortgage groups for the 30-year fixed-rate mortgage:

- The Mortgage Bankers Association predicts it will rise to 4.6 percent in 2018.

- The National Association of Realtors expects it be around 4.5 percent at the end of 2018.

- Realtor.com says the rate will average 4.6 percent and reach 5 percent by year-end.

Though rates are likely to rise, there’s still a window for homeowners to refinance if they haven’t done so already. Lenders typically say it’s worth it to refinance if you can lower your rate by half of one percent.

“The refinance market has more flexibility to time the market,” says Danielle Hale, chief economist for realtor.com. “For most of them, if it still makes sense to refinance, they should go for it because the long-term forecast suggests rates will rise.”

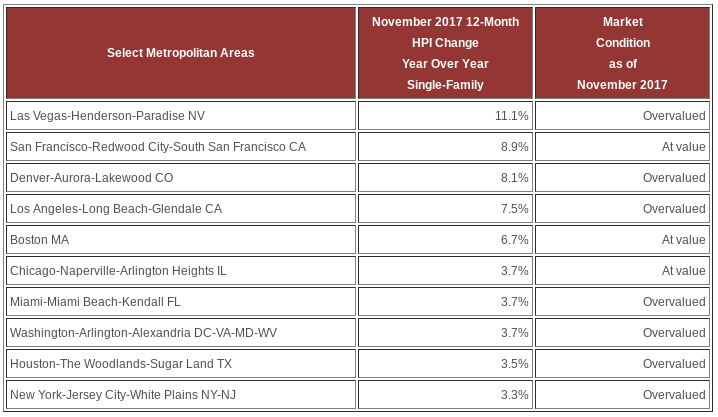

CoreLogic Home Price Index (HPI) and HPI Forecast for November 2017

- CoreLogic reports fourth consecutive month with more than 6 percent

- Home prices nationally increased year over year by 7 percent from November 2016 to November 2017, and on a month-over-month basis home prices increased by 1 percent in November 2017 compared with October 2017.

- Looking ahead, the CoreLogic HPI Forecast indicates that home prices will increase by 4.2 percent on a year-over-year basis from November 2017 to November 2018, and on a month-over-month basis home prices are expected to decrease by 0.4 percent from November 2017 to December 2017.

- Washington, Nevada, Utah and Idaho posted 12-month price gains of 10 percent or more in November.

- Lack of affordable housing stock keeps home price index high in many markets.

- According to CoreLogic Market Condition Indicators (MCI) data, an analysis of housing values in the country’s 100 largest metropolitan areas based on housing stock, 37 percent of metropolitan areas have an overvalued housing stock as of November 2017.

“Rising home prices are good news for home sellers, but add to the challenges that home buyers face,” said Dr. Frank Nothaft, chief economist for CoreLogic.

“Growing numbers of first-time buyers find limited for-sale inventory for lower-priced homes, leading to both higher rates of price growth for ‘starter’ homes and further erosion of affordability.”

Home price change and market conditions for select metropolitan areas. Source: CoreLogic November 2017

“Without a significant surge in new building and affordable housing stock, the relatively high level of growth in home prices of recent years will continue in most markets,” said Frank Martell, president and CEO of CoreLogic.

“Although policymakers are increasingly looking for ways to address the lack of affordable housing, much more needs to be done soon to see a significant improvement over the medium term.”

Email market reports to press@inman.com.