The pace at which homeowners are leaving pandemic forbearance relief programs behind has slowed — just as foreclosure protections are lifting. Among loans that are backed by private lenders rather than the government, there’s even been a slight uptick in loans in forbearance, according to a weekly survey by the Mortgage Bankers Association.

The survey showed that during the week ending Aug. 15, 3.25 percent of mortgage borrowers, or 1.6 million homeowners, remain in forbearance programs that allow them to take a break from making their payments.

Share of mortgages in forbearance, by investor type

Source: Mortgage Bankers Association Forbearance and Call Volume Survey for week ending Aug. 15, 2021.

Just 1.66 percent of mortgages backed by mortgage giants Fannie Mae and Freddie Mac are in forbearance. Loans backstopped by Ginnie Mae — including FHA, VA and USDA mortgages — have somewhat less restrictive underwriting requirements, and 3.92 percent are currently in forbearance.

Loans made by private lenders and either held in portfolios or bundled up into private-label securities (PLS) have loosest underwriting requirements and the highest forbearance rate — 7.15 percent, up from 7.05 percent during the week ending Aug. 8.

Mike Frantantoni

“The share of loans in forbearance was little changed, as both new requests and exits were at a slower pace compared to the prior week. In fact, exits were at their slowest pace in over a year,” MBA Chief Economist Mike Fratantoni said in a statement. “There were more new forbearance requests and re-entries for portfolio and PLS loans, leading to a 10-basis-point increase in their share.”

Among loans made by depository lenders like banks and credit unions, portfolio and PLS loans now account for almost half of loans in forbearance, Fratantoni said. Among independent mortgage banks, 40 percent of loans in forbearance are portfolio and PLS loans, “which highlights the importance of this investor category.”

About $42.4 billion in mortgages were packaged into private-label securities during the second quarter — the highest level seen during the pandemic, the Wall Street Journal reports, citing data collected by Inside Mortgage Finance. That’s close to the $42.7 billion in PLS issuance seen during the first quarter of 2020, a peak during the aftermath of the 2008 financial crisis.

A moratorium barring foreclosure proceedings against homeowners with federally-backed mortgages expired at the end of July. But that doesn’t mean loans servicers will be rushing to repossess homes. Before initiating foreclosures against borrowers who are 120 days behind on their payments, federal regulators expect loan servicers to reach out to borrowers and give them a chance to apply for assistance, such as a loan modification.

Forbearance plans typically give borrowers a 3 to 6 month break on their payments, that can be extended to up to 12 months. During the pandemic, some borrowers are eligible for up to 18 months of forbearance.

About 7.3 million homeowners relied on forbearance programs at one point or another during the pandemic. Although many kept making their mortgage payments and the vast majority no longer need help, data from Black Knight suggests that most of those who remain in forbearance will exhaust their eligibility in the the final months of this year. That could prove to be a “staggering” operational challenge for loan servicers tasked with helping borrowers, Black Knight warned.

On Aug. 10, the Consumer Financial Protection Bureau warned loan servicers that it’s monitoring their performance, and encouraged those that are lagging to improve their customer communication capabilities and outreach efforts.

“Many emergency mortgage protections are winding down, and servicers have had ample time to prepare for the millions of distressed homeowners who need their assistance,” said CFPB Acting Director Dave Uejio in a statement. “Today’s report should inform servicers’ own data reviews as they determine whether they are doing enough for borrowers. Servicers who find themselves at the bottom of the pack should immediately take corrective steps. The CFPB will hold accountable those servicers who cause harm to homeowners and families.”

The MBA’s latest forbearance survey shows that compared to the week ending Aug. 8, loan servicers were more likely to offer homeowners the opportunity to defer missed payments, and less likely to cancel their forbearance with no loss mitigation plan in place.

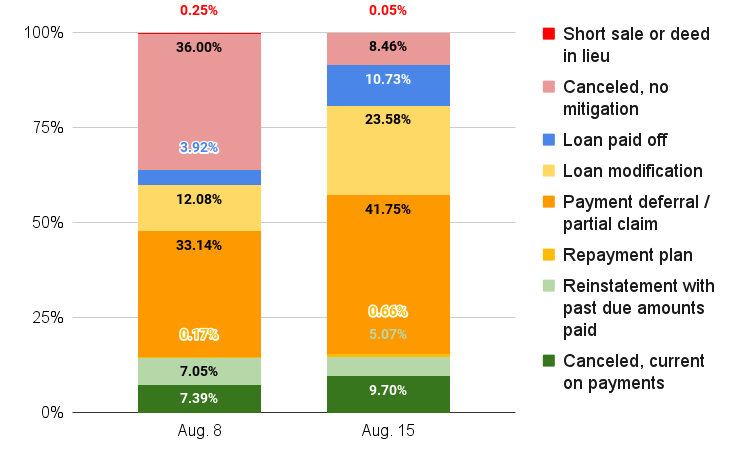

Reason for leaving forbearance

Source: Mortgage Bankers Association Forbearance and Call Volume Survey for week ending Aug. 15, 2021.

During the week ending Aug. 15, 41.75 percent of borrowers exiting forbearance were allowed to defer missed payments, compared to 33.14 percent the week before. The percentage of borrowers granted loan modifications nearly doubled, to 23.58 percent. While 8.46 percent of borrowers exited forbearance without a mitigation plan, that was down from 36 percent the week before.

Borrowers may leave forbearance without a mitigation plan because they didn’t contact their loan servicer to request an extension, or haven’t provided all of the documentation needed to determine if they qualify for a loss mitigation plan, the MBA said.

Under a deferral plan, missed payments are moved to the back end of the loan, and are paid when the borrowers sells their home, refinances it, or reaches the end of their loan term. That way, borrowers don’t have to make bigger monthly payments than they did when they entered forbearance.

In a loan modification, borrowers may be granted a reduced interest rate or an extended repayment term, which can help make their monthly payments more affordable.