In these times, double down — on your skills, on your knowledge, on you. Join us Aug. 8-10 at Inman Connect Las Vegas to lean into the shift and learn from the best. Get your ticket now for the best price.

Report after report makes it clear: rent growth is in a free-fall across the U.S.

After an unprecedented spike in price in 2020 and 2021, rent growth crested in February 2022 and has fallen like a rock ever since.

Make no mistake, it’s still rising each month. But a number of factors are lining up to create welcome news for renters who faced two years of rapid rent growth and trouble for many investors. But that outlook has soured quickly, with one economist predicting a 40 percent drop in commercial real estate prices and another forecasting an impending “shitstorm.”

Markets across the country are now facing a possibility of rent falling year over year amid a negative outlook for apartments and commercial real estate broadly, paired with new units that were started years ago and will soon be finished and available to rent.

“Our market will be impacted in two geographies,” said Dejan Eskic, senior research fellow and scholar at the Kem C. Gardner Policy Institute at the University of Utah, referring to urban and suburban markets in Salt Lake City.

Dejan Eskic | Senior research fellow at the Kem C. Gardner Policy Institute

Salt Lake City is one market in which the total inventory of housing near its urban core is growing faster than nearly any other market in the country, according to data shared by the rental data firm RealPage. That new supply is starting to come online, and it’s giving renters more choices and power over how much they can choose to pay in rent each month.

While those new housing units are being rented out, it will drive up the vacancy rate, which could drive down the cost of rent, Eskic said.

“Downtown, you’ll see negative year-over-year rents. In the suburban markets you’ll probably see flat rents, maybe a little bit of year-over-year decline,” he said. “Downtown you can say north of 5 percent (decline) isn’t a reach, just because you have all that supply.”

After things looked rosy for the builders and owners of rental housing, things are shifting quickly. Here’s how.

How much is rent falling?

Keep in mind, when economists talk about rent falling, they’re typically talking about rent growth slowing. But that’s starting to change as rental markets that were hot during the early year of COVID have quickly cooled.

Molly Boesel | Principal economist at CoreLogic

“I do like to say what’s kind of lost in that narrative of decreasing rents or slowdown in rents is that they’re still increasing at double the rates that they were during that long period of 2010-2020,” said Molly Boesel, principal economist at CoreLogic.

Rent is still rising month after month in most markets across the U.S., and at rates that are higher than what was typically seen before the pandemic.

Rent historically rises by around 2-5 percent each year, depending on whose metric you’re looking at. CoreLogic found single-family rent was growing at a 5.7 percent year-over-year rate in January, according to the latest data available. (The figure is 2.6 percent for apartments, according to Apartment List.)

That’s the lowest level of appreciation for both types of housing since the spring of 2021, and the outlook for the foreseeable future is more of the same as apartments that are being constructed today come online tomorrow and landlords try to fill them amid stiffer competition.

“If demand is cool and there’s a lot of vacancies, property owners aren’t really going to have that same bargaining power to be increasing rents,” said Chris Salviati, a senior housing economist at Apartment List.

A number of markets are already seeing asking rents fall year over year thanks to a rush of new supply and a slowdown in renter demand.

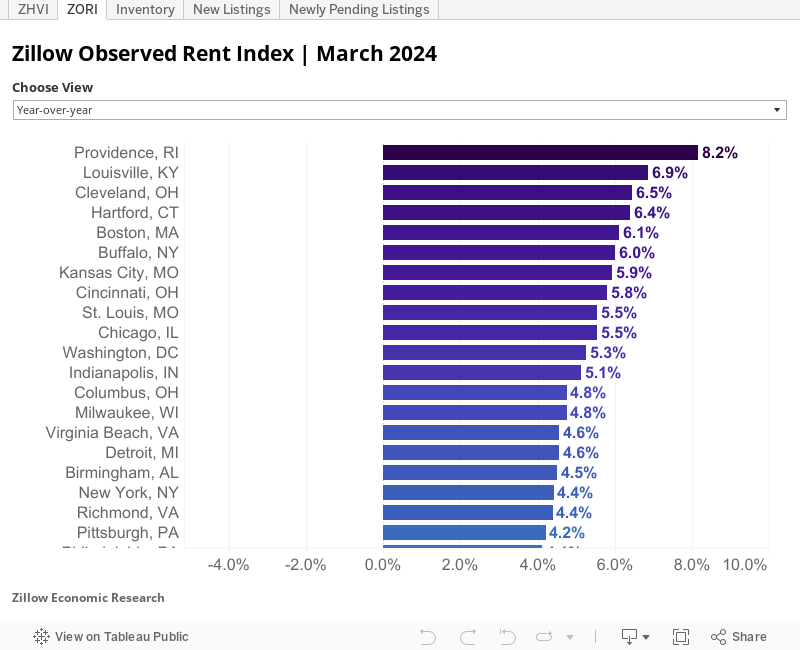

Las Vegas is the first market tracked by the Zillow Observed Rent Index to see rent lower in March 2023 than it was in March 2022, falling by nearly 1 percent. And more markets appear to be close behind.

Rent in Phoenix, which grew by 27.3 percent in 2021, fell by 0.8 percent in 2022 and is down 0.7 percent in 2023, according to Apartment List.

The rush of new inventory

Incoming inventory is hitting at a time of decreased demand for new leases.

There were fewer than 20,000 net new renters looking for a place to live in the first three months of this year nationwide, according to RealPage. At the same time, builders wrapped up over 95,000 new units.

The first quarter of the year was the softest in terms of demand since 2013, according to RealPage, and it comes after demand was soft throughout most of 2022.

That pullback from people forming new households or looking for a new lease comes after builders embarked on a very busy time.

Nashville, Tennessee, shouldered 26,757 new units under construction in January 2023. Once completed, that will represent a 15.4 percent growth in the city’s total inventory.

In Charlotte, North Carolina, builders are adding 32,476 new units, or 15.1 percent of the city’s inventory.

Across the country, markets are seeing builders every month wrap up more rental housing than at any point in the past 36 years, according to the U.S. Census Bureau and Department of Housing and Urban Development.

Chris Salviati | Senior Housing Economist at Apartment List

That all points to a rise in vacant rentals, which in turn gives renters more choices and makes it more competitive for landlords and property managers to fill homes and units.

“Even though we’re back to that normalized pre-pandemic level [in rent growth], it isn’t the case that we seem to be leveling off there,” Salviati said. “This upward trajectory of the vacancy rate hasn’t shown any signs of slowing down yet.”

“We’ve got this record level of new inventory in the pipeline right now,” he said. “As more and more of that hits the market, I think that is going to continue to drive the vacancy rate up.”

The ‘chicken and the egg’

It wasn’t just the single-family housing market that slowed significantly in 2022 after the initial frenzy of the COVID housing years.

The owners of rental apartments also saw a rapid slowdown in demand in yet another blow to the rental market.

Sales of multifamily buildings have slowed to the lowest point since the middle of the Great Recession. The volume of apartment buildings sold in the first three months of the year hit $13.9 billion, down 88 percent from a peak of $115.5 billion in the fourth quarter of 2021.

And there may be more pain ahead.

Just last week, economists with Morgan Stanley Wealth Management predicted a 40 percent drop in commercial real estate prices, which would be a steeper drop than the fallout that occurred during the Great Recession.

A standoff between apartment buyers who can’t or won’t make offers based on the current outlook for commercial real estate and owners who won’t sell for lower prices has yet to break.

Carl Whitaker | Director of research and analysis at RealPage

“Interest rates are probably the single biggest lever holding back property trades right now,” said Carl Whitaker, director of research and analysis at RealPage. “Not only the nominal rate itself, but the steepness at which that rate increased paired with uncertainty of ‘how much more could it rise?’ is causing lots of tepid acquisitions behavior today.”

During economic uncertainty, Whitaker added, tomorrow’s landlords are pushing the brakes.

Data from CoStar shows sale of apartment buildings slowed to a halt in the first three months of 2023.

What happens next?

Economists have been waiting to see if the rental market is falling back to a pattern of seasonal norms, when renter demand rises in late spring and summer before falling in the colder months.

Inflation has remained stubbornly high, in large part because rent and housing costs are the biggest single factors in inflation figures.

The Federal Reserve has shown a willingness to keep rates high as long as inflation is high and the labor market is red hot, and so far those haven’t cooled down.

But the uncertainty for what happens next may have an ongoing impact on the rental market, economists said.

“You might get households doubling up. Where I live it’s very unusual for a person in their mid-20s to have their own place,” Boesel said. “There could be more doubling up. Maybe pulling back on a little demand.”

RealPage’s Whitaker expects rent growth to fall back in line with historical norms, between 2-4 percent throughout the rest of the year.

But the mid-term outlook for much of the new rentals — many of which are considered high-end, ‘Class A’ units — looks a bit more dire for the next 1-2 years.

“We’re a little less optimistic on Class A in the coming 12 to 18 months as this massive wave of supply gets absorbed,” Whitaker said. “Because of that, we’re more optimistic on the Class B outlook through 2023 and into 2024.”

Eskic, from the University of Utah, had a different term for the upcoming period when the rush of new supply hits the market.

“All that stuff kind of starts, the majority of it starts leasing,” Eskic said, “that’s when you’re going to see the shitstorm come.”

Get Inman’s Property Portfolio Newsletter delivered right to your inbox. A weekly roundup of news that real estate investors need to stay on top, delivered every Tuesday. Click here to subscribe.