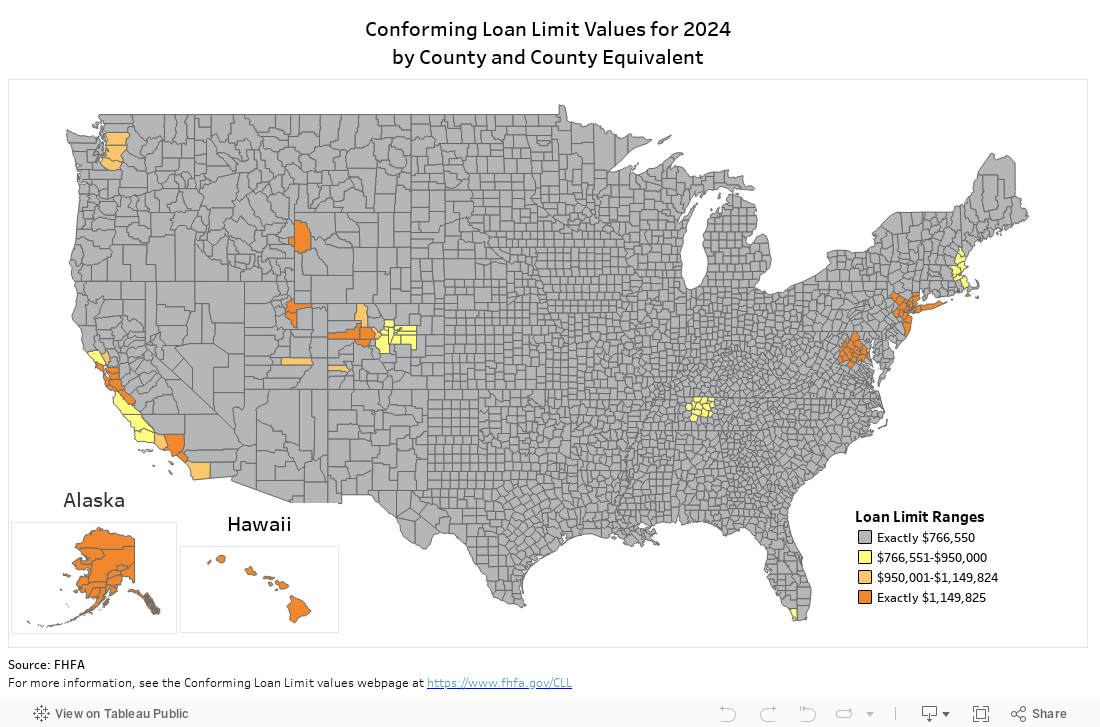

Mortgage giants Fannie Mae and Freddie Mac will be allowed to back mortgages of up to $766,550 in most parts of the country next year, sparing more buyers from having to apply for a jumbo mortgage.

The $40,350 increase in the baseline conforming loan limit announced Tuesday by the Federal Housing Finance Agency (FHFA) is the smallest increase since 2021, as annual home price appreciation continues to cool.

Fannie and Freddie’s upper limit will be higher in 152 counties and Census areas where homes are costlier, with a ceiling of $1,149,825 for one-unit properties in Alaska, Hawaii, Washington, D.C., and a number of high-cost markets in states like California, Colorado, Maryland, Massachusetts, New Jersey, New York and Virginia.

Congress has mandated that the conforming loan limit be tied to annual increases in FHFA’s seasonally adjusted, expanded-data House Price Index. That index, also released Tuesday, showed home prices were up 5.5 percent from a year ago as of Sept. 30.

That’s a considerable slowdown from the 12.4 percent annual home price appreciation registered at the same point in 2022. But home prices posted 2.1 percent annual growth from Q2 to Q3, the strongest performance in more than a year, FHFA economist Anju Vajja said.

Anju Vajja

“The rate of house price appreciation, that had started to slow down since the second quarter of 2022, reversed its trend in the third quarter of 2023,” Vajja said. “All nine census divisions also recorded positive annual house price growth. House prices continue to appreciate despite high mortgage rates, largely due to the low supply of existing homes for sale.”

Borrowers looking to take out loans that exceed the 2023 conforming loan limit, currently $727,200 in most parts of the country, may now be able to avoid applying for a jumbo mortgage exceeding that limit.

Because Fannie and Freddie can’t buy or guarantee mortgages exceeding the conforming loan limit, jumbo mortgages tend to have stricter underwriting and higher down payment requirements. Some borrowers may also pay higher rates than they would for conforming loans.

While the new limits don’t take effect until Jan. 1, lenders can treat loans that exceed the current limit as conforming by holding them on their books for a few weeks until the increase becomes official.

A number of lenders, including Rocket Mortgage, UWM and Guaranteed Rate, last month began treating mortgages of up to $750,000 as if they met Fannie Mae and Freddie Mac’s conforming loan limits, as the increase in the limit was expected.

Holden Lewis

“By increasing the maximum loan amount, the change means that more borrowers will be able to get conforming loans instead of jumbo mortgages, which often are harder to qualify for,” NerdWallet mortgage expert Holden Lewis said, in a statement. “It might open the door for homeownership just a touch wider for a few buyers who would have had trouble securing jumbo loans.”

But Lewis said he expects the increase will have only a small effect on home sales because mortgage rates are forecast to remain above 6 percent next year, and for-sale inventory is expected to fall short of demand.

2024 conforming loan limits for multi-unit properties

The baseline conforming limits for multi-unit properties for 2024 will be $981,500 for two-unit homes, $1,186,350 for three-unit homes, and $1,474,400 for four-unit properties.

The ceiling in high-cost markets will be $1,472,250 for two-unit properties, $1,779,525 for three-unit homes, and $2,211,600 for four-unit properties.

Baseline conforming loan limit, 2000-2024

Source: Federal Housing Finance Agency.

The conforming loan limit was increased by a record-breaking $98,950 in 2022, after drastic easing by the Federal Reserve during the pandemic pushed mortgage rates to historic lows, increasing borrowers’ buying power and pushing home prices up.

Before 2022, the biggest year-over-year increase in the conforming loan limit was registered in 2006, when easy access to mortgages fueled a buying boom that pushed the conforming limit to $417,000, up $57,350 from the year before.

The housing crash and Great Recession of 2007 through 2009 left the limit static at $417,000 for 11 years. While the conforming loan limit is increased whenever home prices go up, it’s not ratcheted back when home prices fall. Instead, it’s allowed to stay at the previous peak until home prices catch up, as was also the case from 1993-1996.

The Housing Policy Council, a mortgage indusry trade association, issued a statement warning that the higher loan limits “exacerbate the affordability crisis and increase the housing finance system’s over reliance on government backing.”

Noting that the baseline conforming loan limit is more than 10 times the 2022 median household income of $74,580, the group pointed to a 2013 proposal by the Obama administration to wind down Fannie Mae and Freddie Mac and “put private capital at the center of the housing finance system.”

“The current housing finance system, where the government guarantees more than 80 percent of all mortgages through Fannie Mae and Freddie Mac and FHA, is unsustainable,” the Obama White House said at the time. “A reformed system must have a limited government role, encourage a return of private capital, and put the risk and rewards associated with mortgage lending in the hands of private actors, not the taxpayers.”

A decade later, the latest increase in the conforming loan limit “continues the relentless march of our housing finance system away from relying on private capital,” the Housing Policy Council said.

“As we warned in 2022 and 2021, the question of the appropriate role of the government in the housing finance system has gone unanswered for far too long,” the group said. “The Housing Policy Council urges Congress and the Biden Administration to take up this question soon.”

In higher-cost markets, Fannie and Freddie are allowed to purchase bigger mortgages based on a multiple of the median home value, up to a ceiling that’s equal to 150 percent of the baseline conforming loan limit.

Next year, the conforming loan limit will exceed $1 million in 110 counties and Census areas concentrated in nine metro areas. The conforming limit will also be higher than the $766,550 baseline, but less than $1 million, in 42 counties and Census areas nationwide.

Editor’s note: This story has been updated to include comments from the Housing Policy Council, a mortgage industry trade association.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.