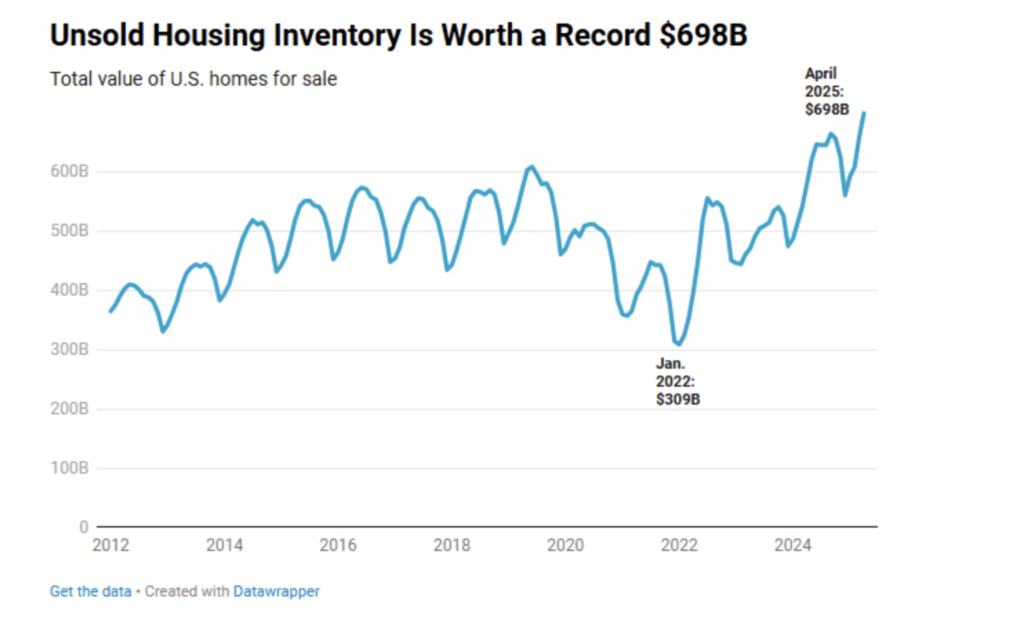

U.S. home inventory hit a record $698 billion in April — a 20.3 percent increase from the previous year — but sales aren’t keeping pace, a new analysis from Redfin shows.

While listings are rising, buyer activity remains muted, leaving many homes sitting unsold far longer than usual.

Redfin | Unsold Housing Inventory

In April alone, total listings jumped 16.7 percent year over year, the highest level in five years, while new listings rose 8.6 percent, hitting a three-year high, yet buyers haven’t followed. Redfin reports there are now nearly 500,000 more sellers than buyers nationwide.

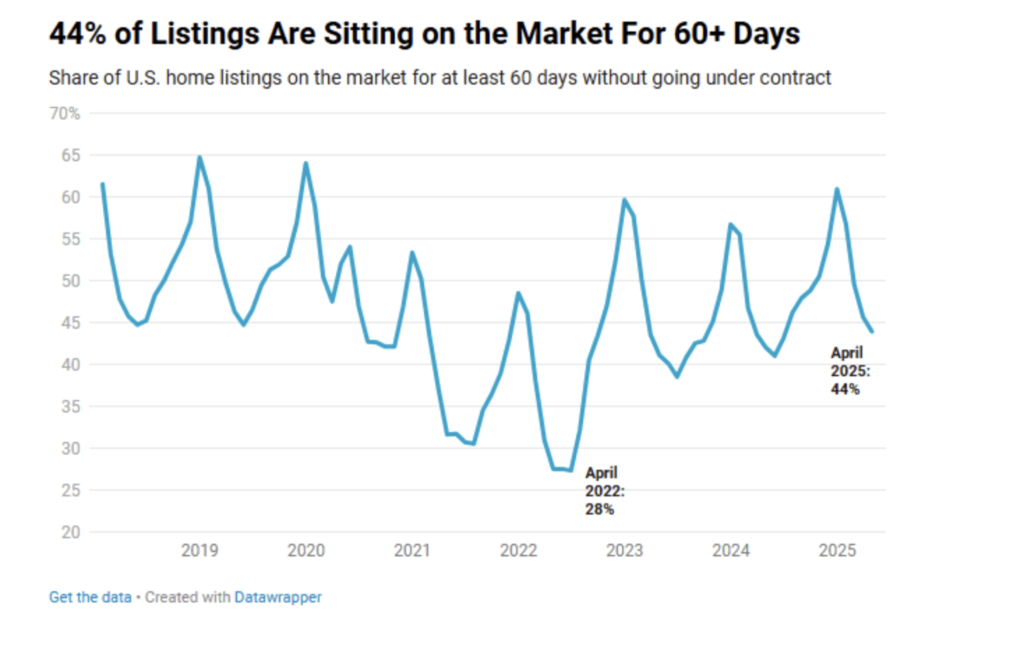

Homes are lingering on the market and getting stale. The typical home took 40 days to go under contract in April — five days longer than last year. More than 44 percent of listings were on the market for 60 days or more. That stale inventory alone accounts for $331 billion, nearly half the total market value.

Redfin

Chen Zhao | Redfin’s Head of Economics Research

“The record-high dollar value of all homes listed for sale is one way to quantify this buyer’s market,” Chen Zhao, Redfin’s head of economics research, said in Redfin’s analysis. “Not only are there more homes for sale than there have been in five years, but the value of those homes is higher than it has ever been.”

Contributing to this slowdown are record-high monthly housing costs, economic uncertainty and rising home-sale prices. The median U.S. home-sale price in April was up 1.4 percent from the previous year, but many sellers are now willing to negotiate.

“A huge pop of listings hit the market at the start of spring, and there weren’t enough buyers to go around,” Matt Purdy, a Redfin Premier agent in Denver, said. “House hunters are only buying if they absolutely have to, and even serious buyers are backing out of contracts more than they used to. Buyers have a window to get a deal; there’s still a surplus of inventory on the market, with sellers facing reality and willing to negotiate prices down.”

Matt Purdy | Redfin Premier Agent

In stark contrast to today’s slower market, inventory in early 2022 bottomed out at $309 billion. Mortgage rates hovered around 3 percent, and homes sold in a median of just 24 days. Now, with rates near 7 percent and affordability stretched thin, the stockpile of unsold homes keeps growing.

Zhao says there may be a silver lining for buyers as incomes continue to increase.

“We expect rising inventory, weakened demand, and the prevalence of stale supply to push home prices down 1 percent by the end of this year, which should improve affordability for buyers because incomes are still going up,” she said.