Although the median existing-home sales price has managed to climb for a consecutive 88 months, the median luxury home sales price has failed to keep that same momentum according to Redfin’s Q2 2019 luxury home market analysis released on Tuesday.

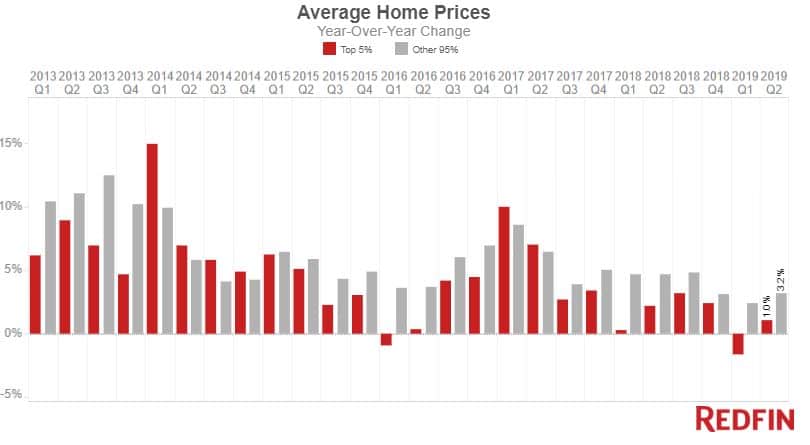

Redfin’s analysis of the 5 percent most expensive homes sold in more than 1,000 metros (excluding New York City) revealed that median luxury home prices managed to increase 1 percent year-over-year to $1.64 million — a slight turnabout from the three consecutive quarters of decreases.

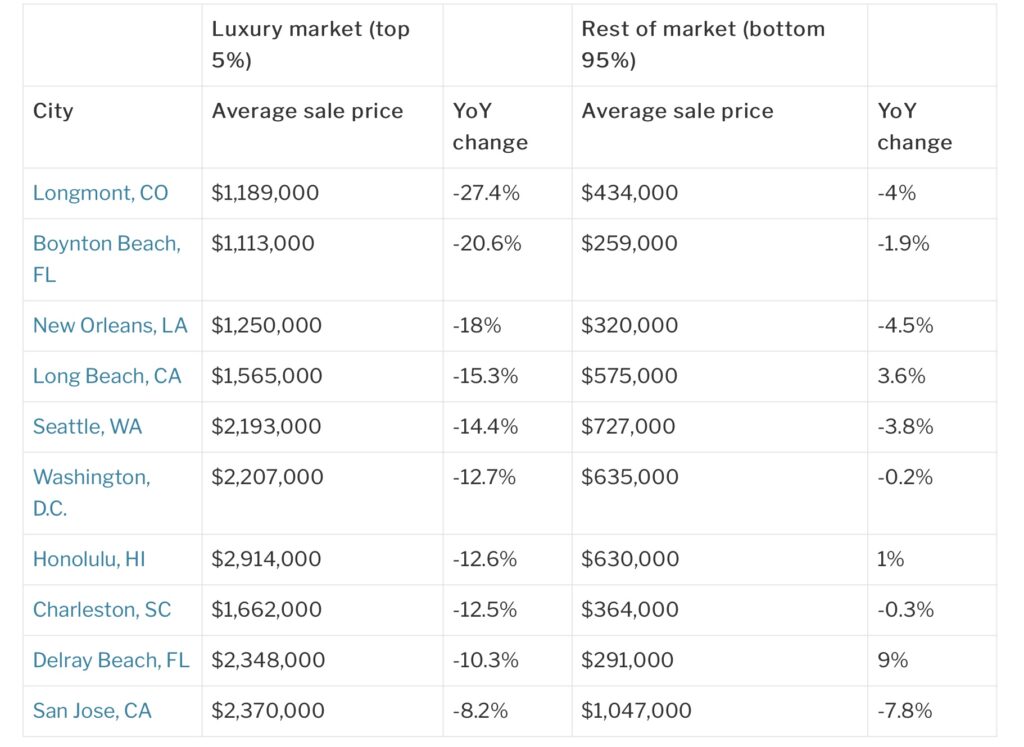

The study noted listings priced below $1.5 million took the biggest hit, with sales dropping 6.7 percent year-over-year. Meanwhile, listings priced above the $1.5 million mark declined 4.6 percent year-over-year. Notoriously expensive markets, such as Seattle, Washington, D.C., Honolulu and San Jose, experienced the biggest home price slump, with median luxury home prices declining anywhere from 14.4 to 8.2 percent.

The study noted listings priced below $1.5 million took the biggest hit, with sales dropping 6.7 percent year-over-year. Meanwhile, listings priced above the $1.5 million mark declined 4.6 percent year-over-year. Notoriously expensive markets, such as Seattle, Washington, D.C., Honolulu and San Jose, experienced the biggest home price slump, with median luxury home prices declining anywhere from 14.4 to 8.2 percent.

In the report, Redfin chief economist Daryl Fairweather attributed weakening home price growth to an abundance of inventory matched matched with a slowing sales pace, and luxury buyers’ fears about economic shifts and policy changes that could put their wealth and investments at risk.

“Luxury home sales have been relatively soft since early 2018 when the tax code overhaul made it so that people with big mortgages and those living in high-tax states and counties couldn’t deduct as much from their annual tax bill,” he said.

“But wealthy Americans who would otherwise be considering a multimillion dollar home purchase may now be a bit spooked that the economic expansion they’ve been enjoying for the past decade could soon be nearing its end.”

Beyond tax code adjustments, Fairweather says the Fed’s continual rate cuts are putting luxury buyers on edge because the cuts could interpreted as a last-ditch effort to stimulate a slowing economy.

Despite the fact that the economy at home is continuing to grow, these and other signs that a recession could be looming are likely causing well-heeled homebuyers to feel extra cautious about a big purchase or investment,” he added. “The Fed’s rate cut is unlikely to have a big impact on the course of the economy and especially on the luxury housing market, where buyers are the least rate-sensitive.”

“As a result, I expect to see continued caution in the high-end market as the future of the economy becomes more clear to those whose wealth is most closely tied to it,” Fairweather concluded.

Redfin isn’t the only one to notice a shift in the luxury housing market — according to a recent report from Crain’s Chicago Business, luxury home sales in one of the Midwest’s largest metros dropped 14.6 percent percent year-over-year. That translates to 105 less sales in the first half of 2019 (614 sales) compared to the first half of 2018 (719 sales).

Much like the Redfin analysis, Crain’s discovered that concerns about a looming recession are keeping luxury buyers on the sidelines as they seek to protect their assets.

“At the national level, people with the income to buy a million-dollar house know there’s a recession coming,” Americorp broker Matt Laricy told the publication. “Will it be late 2019, 2020, 2021? They don’t know, but they’ll wait it out.”

In an Inman report published on Tuesday, two economists said there’s palpable fear amongst buyers at all price points, and that sales could continue to shift downward if more people decide to hold off on homebuying plans.

“I think [buyers] have to be fairly certain of job certainty, the current state of the economy, the near-term outlook of the economy in order to make a purchase,” economist Rick Palacios told Inman. “So when you have any volatility, it causes some skittishness on behalf of the consumer and that’s rightfully so.”