Mortgage rates aren’t expected to come down as dramatically next year as economists had previously expected, which could keep home sales from rebounding in 2024 or limit the strength of a housing recovery, according to two closely followed forecasts.

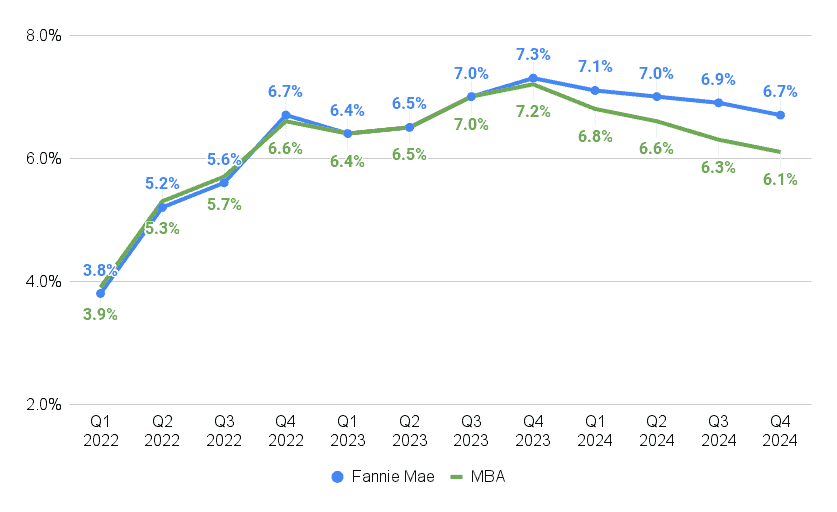

In releasing their latest forecasts, economists at Fannie Mae and the Mortgage Bankers Association (MBA) agreed that rates are likely to ease next year, but they disagree on exactly how much they’ll fall.

The MBA’s more optimistic outlook on mortgage rates helps explain why forecasters at the trade group expect home sales to rebound by 6 percent next year, while Fannie Mae economists expect 2024 home sales will be essentially flat.

In a forecast released Sunday in conjunction with the trade group’s annual meeting, the MBA said it expects rates on 30-year fixed-rate mortgages to fall by more than a percentage point next year, to an average of 6.1 percent during the fourth quarter of 2024.

Just last month, the MBA had predicted mortgage rates would fall well below 6 percent next year, to an average of 5.4 percent during the final three months of 2024. That was before a series of data releases showed the economy has not cooled as rapidly as expected in the face of Fed rate hikes, sending yields on long-term bonds and mortgage rates soaring to new highs.

Mike Fratantoni

“The Fed’s hiking cycle is likely nearing an end, but while Fed officials have indicated that additional rate hikes might not be needed, rate cuts may not come as soon or proceed as rapidly as previously expected,” MBA Chief Economist Mike Fratantoni said in a statement. “Lower rates should help boost both homebuyer demand and increase the inventory of existing homes, thereby supporting purchase origination volume in 2024.”

This month’s surge in rates prompted the MBA, the National Association of Realtors and other housing industry groups to urge the Federal Reserve to declare that it’s done hiking rates. NAR and two other lender groups also want the Fed to resume purchases of mortgage-backed securities that helped push mortgage rates to historic lows during the pandemic.

Mortgage rate forecasts diverge

Source: Fannie Mae, Mortgage Bankers Association forecasts.

MBA economists expect mortgage rates will slip below 6 percent in Q1 2025 on a steadily declining trajectory that would bring rates on 30-year fixed-rate loans back down to an average of 5.5 percent during Q4 2025.

Fannie Mae forecasters have a more cautious view of how far and how fast mortgage rates might fall. In a forecast released Monday, Fannie Mae’s Economic & Strategic Research (ESR) group predicted 30-year fixed-rate mortgages will only fall by about six-tenths of a percentage point over the next year, to an average of 6.7 percent during Q4 2024.

Doug Duncan

While Fannie Mae economists don’t think the Fed will hike rates again, “we continue to take the Federal Reserve at its word that rates will be ‘higher for longer’ until annual inflation stabilizes at the two-percent target,” Fannie Mae Chief Economist Doug Duncan said, in a statement.

Last month, Fannie Mae forecasters thought mortgage rates would fall to an average of 6.3 percent in the final three months of next year. Fannie Mae’s forecast does not attempt to predict where rates will be in 2025.

Duncan said the latest numbers on personal consumption show consumers remain resilient, raising the odds that the economy can achieve a “soft landing.” Nevertheless, Fannie Mae economists are sticking with previous forecasts for a “modest recession” in the first half of 2024. MBA economists are also predicting a “mild recession” in the first half of next year.

“The job market will likely slow as we enter 2024, with fewer jobs added and the unemployment rate increasing from its current rate of 3.8 percent to 5.0 percent by the end of 2024,” Fratantoni said. “Inflation will gradually decline towards the Fed’s 2 percent target by the middle of 2025.”

In their first update of their home price appreciation forecast since July, Fannie Mae economists said they no longer expect home price declines next year. Fannie Mae’s home price appreciation forecast, which is updated quarterly, projects national home price appreciation will cool to 2.8 percent by the fourth quarter of 2024. In July, economists at the mortgage giant said they expected national home prices to dip into the red by Q3 2023.

Home price appreciation expected to cool

Source: Fannie Mae, Mortgage Bankers Association forecasts.

“Despite higher mortgage rates and affordability pressures, the ongoing lack of listings available has continued to support house prices,” Fannie Mae economists said in commentary accompanying their latest forecast. “However, we expect home price growth to decelerate going forward, especially in light of the recent rise in mortgage rates.”

MBA forecasters, who analyze a different set of data — the Federal Housing Finance Agency’s Purchase-Only House Price Index — see home price appreciation cooling to 0.7 percent during the second quarter of next year before rebounding, with tight inventory supporting price growth.

Will home sales rebound next year?

Source: Fannie Mae, Mortgage Bankers Association forecasts.

With their more optimistic projections that mortgage rates will retreat in 2024, MBA forecasters also see more room for home sales to bounce back next year than their counterparts at Fannie Mae.

MBA economists expect home sales to grow by 6.3 percent next year, to 5.17 million, and continue rebounding in 2025 and 2026. Next year’s growth is expected to be driven by an 8.7 percent increase in sales of new homes, to 752,000, and 5.9 percent growth in sales of existing homes, to 4.42 million.

Joel Kan

“New home sales continue to be stronger than existing-home sales, as buyers increasingly turn to newly constructed homes given the dearth of existing home listings and how competitive the bidding process still is,” MBA Deputy Chief Economist Joel Kan said in a statement. “Data from our Builder Applications Survey have shown solid year-over-year gains in purchase applications in recent months.”

But Fannie Mae forecasters expect that after dropping 15.3 percent in 2023, to 4.805 million, home sales will remain at pretty much the same level next year (4.796 million).

“In many ways, the housing market experienced four years of business in a two-year period between mid-2020 and mid-2022,” Duncan said. “With ongoing affordability constraints and rising mortgage rates, much of that activity has essentially been given back. We expect the higher mortgage rate environment to continue to dampen housing activity and further complicate housing affordability into 2024.”

Home prices could boost mortgage originations

Source: Fannie Mae, Mortgage Bankers Association forecasts.

Fannie Mae’s more bullish outlook on home price appreciation helps explain why forecasters at the mortgage giant expect purchase mortgage originations to grow by 10 percent next year, to $1.44 trillion — even if home sales are flat. Fannie Mae economists expect refinancing volume to grow by 82 percent next year, to $456 billion, as rising home values give homeowners more leeway to cash out equity.

MBA forecasters expect prices to remain firm and for home sales to increase next year, driving purchase loan originations up 11 percent, to $1.47 trillion. The MBA forecasts mortgage refinancing volume will grow by 52 percent in 2024, to $478 billion.

But lenders are expected to continue cutting staff to reduce expenses into next spring, said Marina Walsh, the MBA’s vice president of industry analysis. The MBA estimates that independent mortgage banks and mortgage subsidiaries of chartered banks lost an average of $2,812 on each loan they originated in the last three months of 2022, pre-tax.

Marina Walsh

While losses shrank to $1,972 per loan during Q1 2023 and $534 per loan during Q2, “Excess capacity continues to be a challenge for mortgage lenders, with low productivity levels and high expenses per loan,” Walsh said in a statement. “Lenders have reduced their headcounts and gross expenses, but the record-low volume is a primary driver of these escalating per-loan costs.”

A year ago, the MBA estimated that the drop in production volume would force lenders to slash mortgage industry employment by 30 percent from peak to trough. The MBA now estimates that the industry “is roughly two-thirds of the way there.”

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.