A proposal floated by the Trump administration over the weekend to address homebuyer affordability by allowing mortgage giants Fannie Mae and Freddie Mac to back 50-year mortgages has been met with widespread disdain by mortgage and financial planning experts, who are panning the idea as a bad deal for borrowers.

President Trump teased the idea Saturday in a Truth Social meme, which was quickly confirmed by Federal Housing Finance Agency Director Bill Pulte, who said Fannie and Freddie “are indeed working on the 50 year-mortgage — a complete game changer.”

Spreading out borrowers’ payments over 50 years instead of 30, the option most homebuyers choose today, would provide a slightly lower monthly payment — but stick borrowers with a higher interest rate and leave them with a much smaller ownership stake in their home after making 10 years of payments, critics noted.

“As you extend the term of a loan, you often agree to pay more annual interest (due to a higher interest rate) and pay less in REQUIRED principal,” John Downs of Vellum Mortgage Inc. posted Monday in one typical response on LinkedIn.

There might be an argument for such a product if borrowers were able to get the same rate on a 50-year loan as a 30-year loan, Downs said (other experts on mortgage finance said 50-year loans would most likely carry higher rates, unless subsidized by the government).

“Let’s see how all this plays out,” Downs said. “But to my first comment, I think this is a big nothingburger.”

The idea of a 50-year mortgage didn’t sit well with some conservative commentators either, like Christopher Rufo, author of “America’s Cultural Revolution: How the Radical Left Conquered Everything.”

“The idea behind the 15- and 30-year mortgage is that you eventually own the home you live in, whereas the 50-year mortgage abandons this pretense altogether and fully embraces the idea of housing as a speculative asset,” Rufo posted on X. “Not good, unless you’re a bank.”

Facing a barrage of criticism and detailed breakdowns of unfavorable borrower repayment schedules on the social media platform X, Pulte followed up with reassurances that a 50-year mortgage is not viewed as a silver bullet solution to housing affordability.

“We hear you,” Pulte posted Sunday on X. “We are laser focused on ensuring the American Dream for YOUNG PEOPLE and that can only happen on the economic level of homebuying. A 50 Year Mortgage is simply a potential weapon in a WIDE arsenal of solutions that we are developing right now. STAY TUNED!”

Pulte then revealed that Fannie and Freddie are also “evaluating how to do assumable or portable mortgages, in a safe and sound manner,” and “working on ways to give relief in the 5-year mortgage, the 10-year mortgage, and the 15-year mortgage.”

Trump and Pulte last month said they intend to leverage the government’s tight control over Fannie Mae and Freddie Mac to spur homebuilders into action and speed up construction on vacant lots — an idea that’s left some housing policy experts and investment analysts who cover homebuilders scratching their heads.

How loan terms impact borrowers

As Downs and other mortgage experts note, shorter loan terms are a better deal for borrowers because they get a better interest rate and pay down loan principal faster — a concept known as “amortization.”

Since most homebuyers sell their home or refinance their mortgage within seven to 10 years, the question is how much interest and principal they pay during that period — and how much of their home they actually own.

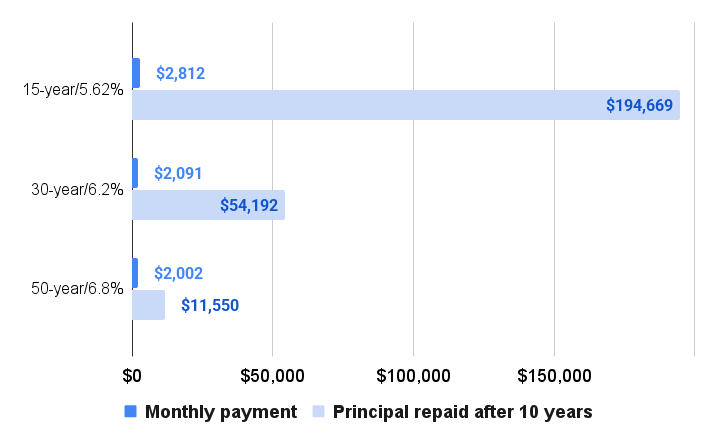

Using actual rates as of Nov. 7 for 15-year and 30-year mortgages, and an estimated rate for a (currently nonexistent) 50-year mortgage, a homebuyer taking out a $341,440 mortgage after putting 20 percent down to purchase a median-priced home would pay:

- $2,812 a month for a 15-year mortgage at 5.62 percent interest, and have retired $194,669 in principal after 10 years

- $2,091 a month for a 30-year mortgage at 6.2 percent interest, which would pay off $54,192 in principal after 10 years

- $2,002 a month for a 50-year mortgage at 6.8 interest, which would pay off $11,550 in principal in the first 10 years

Principal repaid after 10 years, by loan type

Monthly payment and principal repaid after 10 years for a homebuyer purchasing a median-priced home of $426,800 with 20 percent down payment, taking out a 15-, 30- or 50-year mortgage.

So a homebuyer opting for a 50-year mortgage would lower their monthly payment by $89, but owe $42,642 more when they’re ready to refinance or buy another home after 10 years.

“A 15-year is better than a 20-year … a 20-year is better than a 30-year,” Downs said, “if your definition of ‘better’ is less interest and more principal paid.”

But most homebuyers go with a 30-year mortgage because the monthly payments are more affordable, Downs said, and “it gives them the chance to experience the stability in life, which is often only achieved with homeownership.”

Opendoor CEO Kaz Nejatian offered a contrarian view on X, calling the prospect of 50-year mortgages “probably the most pro-homeowner government policy of the last two decades.”

“What this does is massively broaden the base of buyers who right now can’t buy because of student loans,” Nejatian elaborated. “It allows you to get in earlier and start owning and then you can increase your payments later once you’ve paid off student loans.”

One factor not found in amortization tables that could help homebuyers gain equity even with a 50-year mortgage is home price appreciation.

But home prices can also fall, and in those situations, what little equity 50-year borrowers might have amassed would be more easily erased — leaving them “underwater” on their loans and at higher risk of foreclosure.

Mortgage rates are determined by supply and demand by bond market investors who fund most home loans. The longer the loan term, the higher the return investors demand to compensate them for the risk that borrowers will default or refinance before the loan is paid off.

Rates on 50-year mortgages would be higher for another reason — they are not considered “qualified mortgages” with less risky features, which Congress has rewarded with safe harbor protections from lawsuits that are attractive to investors.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.