- The CFPB's silence on Zillow leads to lenders has sparked agent uncertainty about what constitutes a potential violation of a federal anti-kickback law.

Are the agents and lenders who participate in Zillow’s lender co-marketing program violating a federal anti-kickback law?

The Consumer Financial Protection Bureau (CFPB) has not issued any guidance in regards to whether participating in Zillow’s lender co-marketing program violates RESPA, which has promoted uncertainty among agents and lenders across the country. And recent videos from real estate video blogger Brian Stevens have reignited this years-long, ongoing debate.

In a video posted March 8 on his MortgageShots blog, Stevens asserted that examiners from the CFPB had been asking loan officers if they were buying Zillow leads.

According to Stevens, the message was that if so, they were violating Section 8 of the Real Estate Settlement Procedures Act (RESPA).

This is reportedly because “Zillow is taking the information from the customer and then directing that lead to a mortgage company, which is an endorsement, which is a referral, which makes it non-compliant,” Stevens said.

Section 8(a) of RESPA forbids settlement service providers — which includes lenders, real estate agents and real estate brokers, among others — from paying or receiving any fees or other items with the understanding or agreement that business will be sent their way.

RESPA’s Section 8(b), prohibits settlement service providers from splitting charges made or received for performing a real estate settlement service other than for services actually performed.

The CFPB has demonstrated an increasing willingness to go after those accepting payments for mortgage referrals — as evidenced by fines leveled at real estate brokerages last month — which will likely impact more real estate brokers in the future.

Zillow’s co-marketing program, launched in June 2013, allows “Premier Agents” who pay for advertising on Zillow to invite lenders to share marketing costs by paying Zillow to appear as “Premier Lenders” in advertising alongside the agent on the portal.

Agent uncertainty

When agents at Albany, New York-based real estate firm Monticello saw Stevens’ video, they asked their broker for advice on what to do next.

Alexander Monticello

“I’ve gotten questions from a few of the agents in my office who had seen some of the online chatter about the questions of the legality of sharing advertising costs,” real estate broker-owner and attorney Alexander Monticello told Inman in an interview.

“For a newer agent who doesn’t have as much of a revenue stream, sharing advertising costs can really help support the agent,” he added.

He said that “out of an abundance of caution” he recommended his agents not participate in Zillow’s co-marketing program until the CFPB can issue guidance.

“Any guidance from the CFPB would be incredibly helpful to the thousands of agents across the country who are probably wondering about this,” Monticello said.

He wondered aloud: If Zillow’s co-marketing program is really a violation of RESPA, “why have they let it go on for so long?”

CFPB responds — sort of

When asked whether CFPB examiners had been telling loan officers that receiving leads from Zillow violates RESPA, the federal agency did not affirm or deny the report and declined to offer a position on Zillow’s co-marketing program or on whether agents and lenders should be participating in it.

“We’ll decline to comment on any specific company,” said CFPB spokesman Samuel Gilford in an emailed statement.

“More generally, the CFPB enforces RESPA and has been consistent in reminding the industry that any agreement that entails exchanging a thing of value for referrals of settlement service business likely violates federal law.”

Gildford also pointed Inman to an October 2015 compliance bulletin on marketing service agreements (MSAs).

In the bulletin, the CFPB noted that determining whether an MSA violates RESPA requires a review of the facts and circumstances in each individual case, which makes issuing guidance difficult as the facts of one case may be completely different from another case.

Some RESPA experts felt the bulletin was too vague, and others felt it went too far because the agency seemed to deem all MSAs as illegal under RESPA, former Inman staff writer Amy Tankersley wrote at the time.

‘Not cracking down on Zillow specifically’

In a follow-up video on March 9, MortgageShots’ Stevens said different CFPB examiners may be taking varying approaches toward leads from Zillow.

In the video, he notes that a Zillow representative told a loan officer that the CFPB wasn’t cracking down on Zillow specifically, according to an email that Stevens received from said loan officer.

Rather, the Zillow rep reportedly said, the CFPB was cracking down on lead forwarding between agents and lenders, lenders having their credit card on an agent’s account, and a single lender covering more than 50 percent of an agent’s ad spend on Zillow — which is also against Zillow’s program rules.

The Zillow rep also reportedly said “that it’s fine if an agent sends a lender a client after they have spoken and lets a consumer know that the lender will be calling. It is not OK to forward leads directly from an agent to a lender with no conversation to a consumer.”

Inman sent several questions to Zillow Group for this story, including:

- Is Zillow Group aware of such inquiries from CFPB examiners?

- Is Zillow Group aware of any CFPB investigation into whether receiving leads through Zillow Group’s Premier Agent ad forms or through Zillow’s lender co-marketing program violates RESPA?

- Has Zillow Group had any discussions with the CFPB about whether participating in these Zillow programs could violate RESPA?

- Is Zillow Group seeking any sort of declaratory ruling or opinion on this?

- Is the information attributed to a Zillow rep in Stevens’ second video accurate?

“The practice of agents and lenders advertising together has long been a focus of the CFPB, and we, like the rest of the real estate industry, are very focused on this issue,” said Zillow Group spokeswoman Amanda Woolley in an emailed statement, in response to Inman’s inquiries.

“We take into careful consideration all applicable laws and regulations when designing our products. We always evolve our products as the regulatory environment changes to provide the best experience for our real estate industry partners.”

When asked if Zillow Group had changed its lender co-marketing program or any of its other products as a result of any input from the CFPB (or if its statement was simply indicating Zillow Group’s willingness to do so if the CFPB gave guidance to that effect), Zillow Group declined to comment further.

Zillow changes language around lender ads

But there is some evidence that Zillow has at least modified some of the language around lender ads appearing next to Premier Agent ads and on Premier Agent profile pages.

In December 2014, a Zillow inside sales consultant filed a lawsuit against the company alleging it had retaliated against him for notifying upper management about what he called a “pay for play” arrangement between lenders and real estate agents participating in Zillow’s co-marketing program.

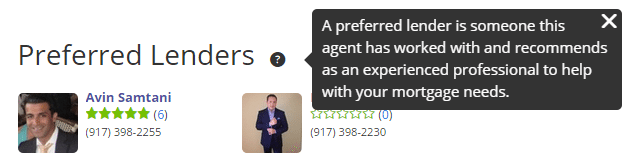

That suit settled in May 2016, but here is what a lender ad looked like on an agent profile page at the time the lawsuit was filed:

Zillow lender ad on agent profile page in December 2014

Here is what a similar ad looks like now:

Zillow lender ad on agent profile page in March 2017

No longer is a lender listed as a “Preferred Lender,” now appearing as a “Premier Lender” instead. And while the older ad explicitly said the agent recommended the lender, the more recent ad explicitly says that neither Zillow nor the agent recommend or endorse Premier Lenders.

The newer ad also points out the financial relationship between the agent and the lender and the fact that they both pay to advertise on Zillow.

Zillow Group declined to comment on when or why it made these changes.

Don’t expect help from the CFPB

In his second video, Stevens said his goal was not to “harm Zillow,” but rather to inform agents and lenders so they can make better decisions for their businesses.

“My point was for you to be cautious going forward because what we know from the CFPB is that they engage in policy through punishment, meaning we know what the new policy is when a punitive action is taken against a lender,” Stevens said.

“The concern is, you don’t want to be that lender.”

Ken Trepeta

Ken Trepeta, executive director of the Real Estate Services Providers Council (RESPRO), agreed.

“The bureau has a lot of power” and “they certainly have had a more stringent way of looking at RESPA than others have in the past, including the courts,” Trepeta told Inman in an interview.

He does not expect the CFPB to issue any guidance in regards to Zillow’s co-marketing program or other similar lead generation programs, noting that historically, CFPB’s guidance “has come out in their consent orders.”

Trepeta advised real estate firms to hire an attorney that specializes in RESPA.

“If I was planning on initiating a practice of buying these leads, I would consult a good RESPA attorney and see what they have to say about it,” he said.

“If I was going to go forward, I would make sure I had their blessing on the manner in which I was going to go forward.”

Compliance hinges on whether it looks like a lender is paying for a referral, and several factors can go into analyzing that, he added, including:

- What type of a success rate do the leads have? “The more likely the lead is going to pan out, the more likely that it looks like a referral,” Trepeta said.

- How much of an agent’s ad spend is the lender covering and is the lender’s advertising exposure proportional to how much the lender spent?

- Does the ad make some distinction as to whether the agent is endorsing the lender?

It could be the CFPB is waiting for litigation between it and mortgage lender PHH to be resolved before saying more in regards to RESPA, according to Trepeta. PHH won an appeals court ruling deeming the CFPB’s structure unconstitutional and the CFPB is appealing the decision. PHH alleges that the CFPB has misinterpreted RESPA and is overstepping its role.

“It will all shake out,” Trepeta said, but in the meantime, agents and lenders will have to tread carefully to avoid the CFPB’s attention.

“People just want to be cautious and avoid anything that could get them in trouble, rightfully or wrongfully,” Trepeta said.

“I think they’ll be temporarily in trouble even if a year from now it turns out that the bureau’s interpretation was completely inconsistent with the letter of the law. But who wants to spend a lot of money finding that out?”