- U.S. homeownership rates are hovering near a 50-year low due to a mix of affordability challenges.

- NAR plans to lobby hard for an environment more friendly to buyers.

Heidi Maierhofer

Heidi Maierhofer dropped everything to attend the National Association of Realtors’ (NAR) Sustainable Homeownership Conference at the University of California, Berkeley on Friday.

Struck by stories from colleagues who are facing low inventory issues across the country and her own experiences in the San Francisco Bay Area Peninsula, the principal at Keller Williams Bay Area Living had a sense of urgency.

Looking at the numbers from her MLS over the past 10 years, she said: “It was so clear to me that we are back down to recession levels in terms of levels of turnover.” As the listing supply shrinks, her agents are having to work harder to hold market share.

Meanwhile, her clients are tending to stay put and remodel. For now, the voter-backed Prop 13 measure that restricts tax hikes on properties until they’re sold and the capital gains tax, which puts a $500,000 cap on the profit homeowners can walk away with, are making it unattractive to move.

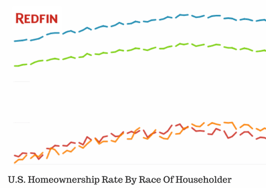

That’s the close-up perspective. From a bird’s eye view, U.S. homeownership hit a 50-year low in the second quarter of 2016, according to a new white paper presented at the conference — “Hurdles to Homeownership: Understanding the Barriers.” And despite marginal improvements in 2017, the mix of affordability challenges and the growth of minority and young households will put downward pressure on the homeownership rate for the foreseeable future without action.

The research identified five main roadblocks to homebuying. The list included post-foreclosure stress disorder, the psychological changes in decision-making for the nine million homeowners who went through foreclosure and the 8.7 million people who lost their jobs (or witnessed the struggles of family and friends). Mortgage availability, abnormal credit standards and the growing burden of student loan debt were also part of the picture.

Singling out single-family homes

According to the white paper, prepared by Ken Rosen’s Rosen Consulting Group (RCG) and jointly released by the Fisher Center for Real Estate and Urban Economics at the UC Berkeley Haas School of Business, single-family housing affordability is facing a particular gridlock driven by the lack of inventory, higher rents and home prices, and investors scooping up single-family homes for their portfolios.

And there aren’t enough new single-family homes going up — another barrier holding wannabe buyers back. The insufficient level of homebuilding has created a cumulative deficit of 3.7 million new homes over the last eight years. Difficulty finding skilled labor, higher construction costs and fewer property lots are also causing construction woes.

As a result, the recovery hasn’t materialized for next generation of homebuyers.

“Low mortgage rates and a healthy job market for college-educated adults should have translated to more home sales and upward movement in the homeownership rate in recent years,” said NAR chief economist Lawrence Yun. “Sadly, this has not been the case.

“Obtaining a mortgage has been tough for those with good credit, savings for a down payment are instead going towards steeper rents and student loans, and first-time buyers are finding that listings in their price range are severely inadequate.”

Plummeting recession homeownership rates fail to recover

This latest research gave some stark statistics for Realtors, stating that U.S. homeownership rates have plummeted following the Great Recession and failed to increase during the past decade, leaving one million fewer total homeowners in 2016 than in 2006, despite the addition of approximately 11.8 million new households.

The ability to accumulate wealth through property is being denied to millions of households, the report said.

“A healthy housing market is critical to the overall success of the U.S. economy,” said Rosen. “Too many would-be buyers have been locked out of the market by the factors found in this study, and it’s also one of the biggest reasons why economic growth has been subpar in the current recovery.”

Speaking at the conference, he added: “For me, it’s a mission. We don’t want 100 percent loans, but I think we can do it right. The irresponsible banks went bankrupt; now we are at the other extreme.

“Millennials are scarred; I’m hopeful that will change.”

What is NAR doing about it?

NAR president William E. Brown spoke strongly at the conference about the association’s plan of action. He stressed that NAR would be lobbying policymakers in Washington, D.C., among others to help make homeownership a reality for a younger generation.

Bill Brown

“The decline and stagnation in the homeownership rate is a trend that’s pointing in the wrong direction and must be reversed given the many benefits of homeownership to individuals, communities and the nation’s economy,” said Brown, a Realtor from Alamo, California.

“One of the things we do is advocacy,” he told conference attendees. “We will use these talking points to go to cities, states and the Federal government to advocate [for homeownership]. These initiatives will be given to politicians, to the public, to [media such as] CNBC to get the word out.”

At the end of the conference he vowed to make a difference. The best way to help the middle class into homeownership is through responsible lending and public policies that enable the middle class (and those just out of reach of the middle class) to buy homes, he said.

Let the Golden State be a lesson

Joel Singer

California has the second lowest homeownership rate in the country (53.9 percent) after New York. “We make the assumption that California will be a major renter state by 2025-2027,” said California Association of Realtors (C.A.R.) CEO Joel Singer. “Community resistance has become the norm in new housing.”

Singer, an active advocacy figure in California’s state capital of Sacramento, said that policy must shift to give homebuyers more flexibility.

A key argument coming from NAR’s previous white paper, “Homeownership in crisis: Where are we now?,” is that an underperforming real estate industry resulted in an economic lag. If the homebuilding industry had normalized, RCG estimates that more than $300 billion would have been added to the national economy in 2016, a 1.8 percent boost to GDP.

RCG now forecasts that affordability will fall by an average of nearly 9 percentage points across all 75 major markets between 2016 and 2019, with an estimated 5 million fewer households able to afford the local median-priced home by 2019.

“Declining affordability needs to be addressed with policies enacted that ensure creditworthy young households and minority groups have the opportunity to own a home,” the most recent white paper said.

While states such as Texas have an aggressive construction program — outlined by James Gaines, chief economist for the Real Estate Center at Texas A&M University at the conference — even Texas would face the same problems as California in 40 years time if things don’t change, Singer said.

Gaines said that even now, all is not well for the first homebuyer in Texas. There has been a shift in the market toward higher-priced homes.

While $150,000 to $200,000 used to be the common entry point for a subdivision, now nothing is being built for less than $300,000 in popular markets such as Dallas Fort-Worth.

Creative ideas welcome

Some drastic measures were called for on Friday. Matt Regan, senior VP of the Bay Area Council, which represents the area’s 300 largest businesses, suggested that the government “declare a housing emergency crisis.”

“The Governor has the authority to do this,” he said. “We tax housing to pay for housing. That’s the most backward public policy.”

From 2007 to 2015, the Bay area added 200,000 renter occupied units and just 2,000 occupier-owned units. “These data points are not happening in a vacuum; they are a result of policies, making it impossible to build homes in the Bay Area,” he said.

Regan is looking to C.A.R. to lobby hard at a state level for new homes for the area’s workers. Realtors were going to be critical in the conversation, he said.

Singer added that the solutions must include the revitalization of neighborhoods, change the incentive structure and improve the legal environment for developers.

Bridge loan revival?

At the client level, Maierhofer said she was seeing a return to bridge financing — or short-term loans that close the gap between a home’s sales price and a buyer’s new mortgage — and is hoping to see more of it.

In hot markets like hers, people want to buy first and then sell. “That’s finally coming back with some of the lenders,” she said.

“I would advise them to work closely with their lender/adviser to understand the cost and risk,” she added. “For a while after the financial crisis, it wasn’t even possible for a lot of move-up buyers to get ‘bridge’ financing, but those options have started to come back at a reasonable cost.

“When you think about the cost of selling first — potentially having to go into a short-term rental if you can’t find something right away — the cost of an extra move, the fear of the appreciating market running away on you, which at the pace it’s been going at, can mean thousands of dollars a month, the extra cost of a ‘bridge’ scenario is pretty minimal.”

A third NAR-commissioned white paper, which will highlight “creative policy ideas to promote safe, affordable and sustainable homeownership opportunities,” is planned for later this year.