- Redfin analyzed median incomes for households of different racial and ethnic backgrounds, then compared those to MLS listing prices in 30 major metro areas.

- Middle-class homebuyers are being priced out of homes for sale across the board, but results were especially acute for black and Hispanic median-income households.

When metro areas across the country are booming with economic growth, that should be a good thing for real estate sales — spurring homeownership because jobs are plentiful.

However, according to new research by Redfin — “Priced Out: The Housing Affordability Gap In America’s Largest Metros” — “no metro area gets a trophy” when it comes to providing affordable homes for median-income minority homebuyers, said Redfin’s chief economist, Nela Richardson.

Richardson noted that affordability is a problem for median-income and middle-class homebuyers of all colors, but that the problem is particularly pronounced for Hispanic and black families.

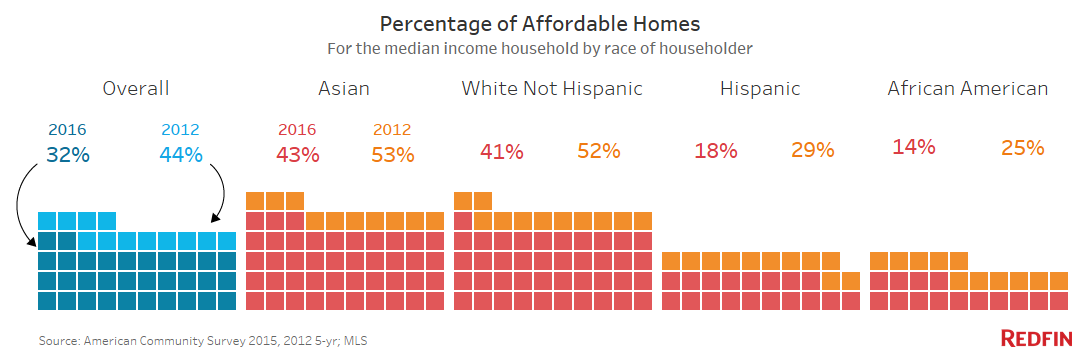

Redfin wrote in the study that home prices across the metro areas studied increased by 26 percent between 2012 and 2016, but “the median household income edged up just 1.6 percent nationally” in that same time period. So any family earning the area median income could afford 44 percent of homes for sale in 2012, but by 2016, that’s dwindled to 32 percent — a 12 percentage point drop.

And for black and Hispanic households, that affordability gap is even more pronounced. In 2012, median-income Hispanic households could afford 29 percent of homes for sale in the metro areas studied, and black households could afford 25 percent of homes for sale; those numbers dropped 11 percentage points apiece by 2016, when Hispanic households could afford 18 percent of homes in the metros in question, and black households could afford 14 percent.

Those numbers become even more acute in areas with red-hot markets.

“When I looked at Seattle and saw that African-Americans could only afford 6 percent of the listings in the metro area — I was blown away by that,” Richardson said, adding that in 2012, median-income black families could afford 13 percent of the listings in the Seattle metro area.

Comparing apples to apples

Redfin compared median household incomes by race and ethnicity based on the U.S. Census American Community Survey for 2015 and 2012 across the 30 largest metro areas for which data was available, then calculated the maximum monthly mortgage payment with a 3.4-percent interest rate and 20-percent down payment, using 30 percent of gross household income. The company also looked at active MLS listings as of October 1, 2016, and used the list price, current HOA dues and property tax rates for each listing to help calculate the estimated monthly mortgage cost.

Then Redfin did the same analysis for 2012 to make a four-year comparison.

The median income for black families in a specific metro area will likely be different than the median income for white families, and both will likely differ from the median income of Hispanic families, so this approach allowed them to compare apples to (income) apples.

Because it didn’t include the entire country, results can’t be extrapolated and applied everywhere — but they do show an increasingly ugly picture of affordability for minority families in many major metro areas.

The bigger picture

“There’s this myth in the atmosphere among the housing conglomerates that housing is more affordable than it’s been in a long time because mortgage rates are so low, and I think that’s kind of an urban myth,” said Richardson. “It doesn’t matter how low the rate is if you can’t get the mortgage and there’s nothing to buy.”

She said that it was difficult to figure out which cities to highlight in the report “because the numbers for every metro were so dramatic — there were so many stories.”

And she added that she wasn’t surprised by the results, but “I was surprised at the magnitude, especially for West Coast cities.”

St. Louis is the only metro among the 30 evaluated where Richardson said “minorities were gaining ground,” but “even in St. Louis, you see huge disparities in median incomes between minority and white families. That is telling about the challenges of the housing affordability gap.”

As a result, the diversity that has thrived in metro areas across the country for years could be ebbing away as minority families are compelled to seek housing — for renting or buying — further away from city centers.

“We also know that rents are climbing as house prices are rising,” Richardson explains. “The net effect is that middle-class families of all races will probably be priced out of homeownership and also priced out of the rental market. That does mean that surrounding suburbs will likely get more diverse, and we’re already seeing that.”

She adds that because these are the metro areas that are producing jobs, this is an especially troubling trend. “There is a problem in the labor market when people can’t move to where the good jobs are because it’s too expensive to live there,” she said.

What should be done?

Richardson has some ideas about what the industry could do at a high-level — politically speaking — to help ease affordability problems for median-income buyers across the board.

“The real estate industry has often lobbied for the mortgage interest rate deduction,” said Richardson. “We’ve in general been in favor of it as a way to increase homeownership, but it’s a fact that those subsidies are the largest in housing and they accrue mostly to the upper-middle-class families. I think it’s time for the real estate industry to reconsider its priorities in terms of boosting homeownership.”

There’s a lot that can be done on the agent level, too, she said.

“It is about helping middle-class buyers find the right places, and I think there are homes available, but learning that these homes are going to be very competitive and basically giving middle-class buyers the tools to compete with, maybe, investors or all-cash buyers will be important,” she noted.

“One of the things we tell our clients is to make sure they’re fully underwritten so all the bank has to do is put the value there. That helps get your bid seen. Giving the seller what they want beyond price — if you can’t escalate to crazy, which sometimes people do — maybe what the seller needs is to be able to rent back the home for a little while, or they need some flexibility in closing or to close really fast, so some more strategic tools to help the middle class wiggle their way into this market are helpful.”

And everyone in the industry should remember that this problem is solvable, she concluded.

“Most solutions now are local because that’s how we think of housing,” she said. “It starts at the local level with zoning and land use regulation. If we can increase supply, then we can also increase homeownership.”