There’s an overwhelming amount of data and headlines circulating. This column is my attempt to make sense of it all for you, the real estate professional, from an overall economic standpoint.

Today, we will focus on last Thursday’s data release for U.S. existing-home sales activity in October, so let’s get straight to it.

If you still thought that the market was going to slow, you will have to wait a little longer. Existing-home sales rose for the fifth consecutive month to an annual rate of 6.85 million units — and that’s up 4.3 percent from September, and sales were 26.6 percent higher than we saw a year ago.

And it’s not just the annual rate that rose, as monthly sales came in at 573,000 – and that’s the highest monthly figure since the market “snapped back” in July following the initial COVID-19 shutdown.

With sales rising, so did prices, with the median price in October measured at $313,000 — and that’s up by a massive 15.5 percent from a year ago. We haven’t seen that pace of price growth since 2006, and it was also the 104th straight month of year-over-year price gains.

And we see these significant increases in prices not just because mortgage rates are low — though that certainly isn’t hurting — but also the more substantial reason is that there’s far more demand than there is supply.

If you remember your college economics classes, what happens to prices when you have limited supply but net new demand? That’s right, they rise.

And as you can see here, there were fewer than 1.4 million homes for sale in October — now, I must add that I seasonally adjust my numbers, and the National Association of Realtors doesn’t, but even if you use its figures, there were just over 1.4 million homes for sale last month, so it’s not much better.

And with tight supply and net new demand, there are only 2.7 months of inventory at the current sales pace — and that’s an all-time low.

A balanced market — depending on where in the country you are, is between four and six months, so we are a long way from balance.

And to give you a different way to see how competitive the market is, there was an average of almost 3.5 offers for every deal written last month.

Additionally, 7 out of 10 homes sold within four weeks of being on the market, and the median market time coming in at just 21 days — it was 36 days a year ago.

Regionally, sales rose the fastest in the small Northeast region, but all areas saw sales up by over 20 percent.

And when we look at sale prices, again, there are very significant increases across the board. I would note that the Northeast saw the most significant price increases for single-family homes — up 21.7 percent. Condo prices rose the most in the Southern states, where prices were up by 13.9 percent year over year.

Well, that’s the big picture, but you know me, I do love to dig into the dark corners of these data releases, and when I did, I found some pretty exciting nuggets there, too.

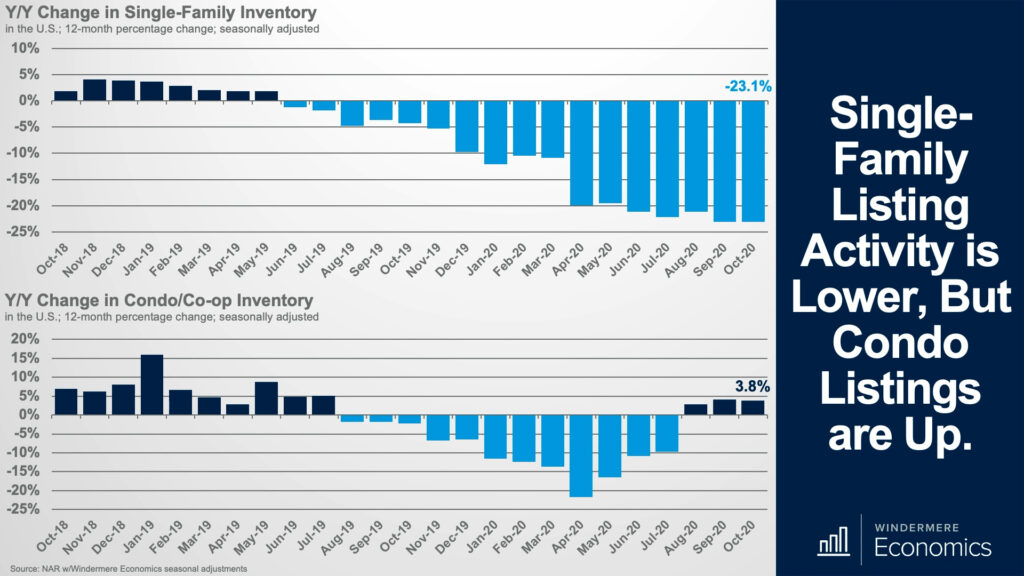

I mentioned single-family and multifamily price growth a moment ago, and when we break out the data, the supply numbers were impressive.

Here is the year-over-year change in available inventory, and it’s not surprising to see the number of single-family homes for sale way down, but look at condos. Inventory is higher than it was a year ago.

Now, I think it’s too early to suggest that this is wholly due to COVID-19 and families flocking away from our urban centers, but I will be watching to see if this is an anomaly or the start of a trend.

And my first reason for not being overly concerned about the condo market is this: Sales are still rising — up by 5.8 percent versus September and up by 25.9 percent year over year — even in the face of increasing inventory.

Single-family sales were up by just a little more — 26.7 percent year over year, but the month-over-month pace of single-family sales was lower than condos and came in 4.1 percent higher than in September.

And finally, condo prices are still trending higher after turning negative at the outset of COVID-19 — up 10.3 percent year over year to $273,600. Not quite the pace of price growth seen in the single-family world where the median sale prices were up by 16 percent to $317,700, but not bad at all.

There you have it, and I think you’ll agree that these were pretty impressive numbers across the board. Indeed, no sign of a slowdown, but as I suggested earlier, I will be watching the multifamily market to see if inventory levels continue to rise.

And if they do, we might see price growth starting to slow even if the single-family market continues its upward trajectory.

Again, I must reinforce my view that this pace of price growth is not sustainable. Of course, very favorable mortgage rates are still in place.

The 30-year hit another all-time record low last week at 2.72 percent, but I still believe that we are close to the lows that we’ll see in this cycle — we’re just not there yet.

Housing continues to outperform, with first-time buyers still out in force (32 percent of all sales went to them). Demand for second homes appears solid too — they accounted for 14 percent of all sales, a figure that matches October 2019. No visible signs of COVID-19 stress there either.

The bottom line is: Something has to give.

I’m not saying that prices will retreat. Instead, the pace of growth has to slow even with very significant demand, and it will happen because of one of two reasons or maybe a combination of both.

Either we will hit an affordability ceiling, which will slow the price increases that we are experiencing, or we will see additional supply that will temper prices.

Though I find it highly unlikely we will see a significant increase in the number of resale homes coming to market, I do see builders stepping up and developing more homes.

Builders are getting bullish, and we know this from the National Association of Homebuilders Market Index, which hit another all-time high earlier this month.

I believe that this optimism will lead single-family starts to stay well above 1 million units next year and rising even more after that, which will be a relief to some buyers who remain very frustrated by the limited inventory available.

The housing market is still performing — COVID or no COVID — and this will continue as we close out the year even if we see some states slowing their economies as new coronavirus cases spike.

But I am getting ahead of myself. Please join me again in two weeks for my 2021 U.S. housing market forecast.

To get the big picture including all of the data, watch the full video above.

Matthew Gardner is the chief economist for Windermere Real Estate, the second largest regional real estate company in the nation.