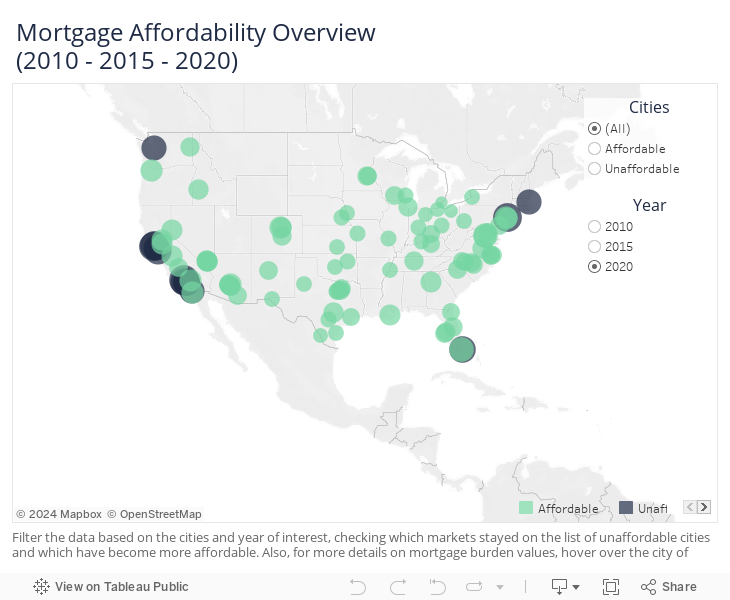

2020 was a year of record-low mortgage rates, but pandemic-fueled homebuyer demand and sharp drops in inventory sent home prices soaring, eroding mortgage affordability in more than half of the country’s largest cities, according to a report from real estate listing site Point2Homes.com.

The report examined mortgage affordability in the 100 largest cities in the U.S. between 2010 and 2020. Unaffordable cities were those where homeowners spend more than 30 percent of their income to cover the mortgage alone.

The study found that mortgage affordability worsened in 51 of the 100 cities in the past decade, meaning homeowners are spending a bigger share of their income on the mortgage now than in 2010. Not surprisingly, during the same period home prices rose faster than wages in 53 of the 100 largest cities. Incomes rose faster than home prices in 45 cities.

The number of unaffordable cities rose from 13 in 2010 to 15 in 2020. Most of those cities are on the West Coast where, in the past decade, the median home price crossed the $1 million threshold in three cities: San Francisco, Fremont and San Jose. Price increases drove Fremont, San Jose and Santa Ana to the unaffordable list in 2020.

“In Fremont’s case, prices nearly doubled compared to 10 years ago,” the report said. “As a result, even with today’s low interest rates, buying the median home in these cities would still require a monthly mortgage payment between $4,000 and $5,000 — assuming that the homebuyer could afford the standard 20% down payment.”

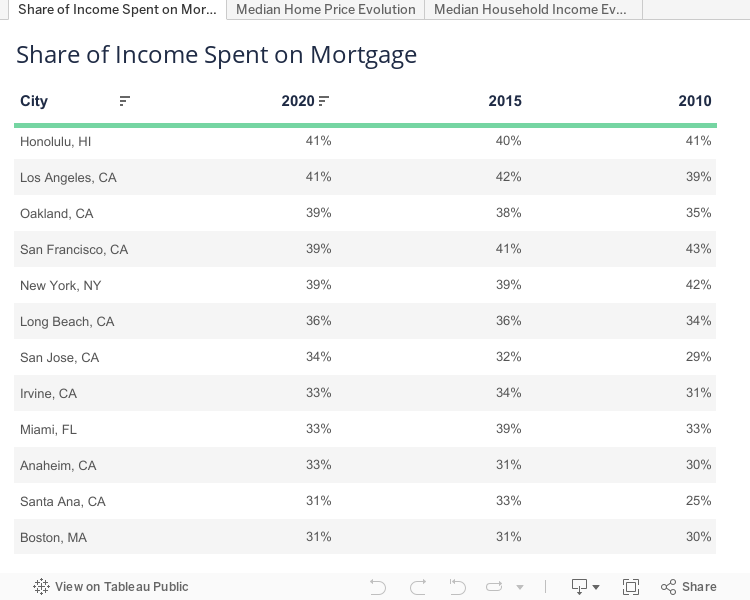

However, the most unaffordable city was Honolulu, Hawaii, where homeowners spent 41 percent of their median income on the mortgage in 2020.

“Honolulu is the only city where mortgages have taken up more than 40% of homeowners’ incomes in 2010, as well as in 2015 and 2020,” the report said.

Source: Point2

Homebuyers in San Francisco, the fourth-most unaffordable city, would need the biggest boost in income to pay less than 30 percent of it toward their mortgage: $43,567. Homebuyers in Seattle, the 15th most cost-burdened city, would need the least amount of extra income: $1,882.

Source: Point2

Incomes jumped the most in San Francisco and Seattle in the past decade — 80 percent and 78 percent, respectively — but overall incomes have not kept pace.

“[S]ome of the cities that saw their home prices skyrocket in the last decade are also the cities where incomes are lagging behind the most,” the report said. “This makes buying a house and getting a mortgage a double whammy, with potential homebuyers having to choose from a pool of increasingly expensive homes with a budget that can’t quite keep up.”

North Las Vegas saw the biggest gap between its rise in home prices (104 percent) and its rise in household income (29 percent) in the last decade, followed by two other Nevada cities: Las Vegas and Paradise. All three are in the state’s Clark County.

Source: Point2

Only Newark, New Jersey, exited the unaffordable list in the past decade. Mortgages there took up 27 percent of homeowner incomes in 2020, down from 34 percent in 2010. There were six cities where mortgages accounted for 10 percent or less of homeowners’ income in 2020: Memphis, Tennessee; Laredo, Texas; Fort Wayne, Indiana; Toledo and Cleveland, Ohio; and Detroit, Michigan.

Source: Point2

Out of the 100 cities, only two saw home prices decline between 2010 and 2020: Cleveland and Toledo.

“[W]hile home price declines are not necessarily a good sign, a market that self-corrects or a city where incomes are not outrun by skyrocketing property values could offer residents a better chance at homeownership,” the report said.

“The opposite of unaffordable markets, the U.S. cities where mortgages take up less than 30% of household income reflect the balanced conditions that most homebuyers and homeowners would welcome.”

See where your city stacks up:

Email Andrea V. Brambila.

Like me on Facebook | Follow me on Twitter