In these times, double down — on your skills, on your knowledge, on you. Join us August 8-10 at Inman Connect Las Vegas to lean into the shift and learn from the best. Get your ticket now for the best price.

Mortgage rates have room to ease after Federal Reserve policymakers stuck to the script Wednesday, approving the smallest interest rate hike in nearly a year and signaling that the central bank is close to wrapping up its year-long rate-hike campaign.

Stocks surged as investors welcomed the modest, 25 basis-point increase approved by Fed policymakers at their first meeting of the year, which brings the short-term federal funds rate to a target range of 4.5 to 4.75 percent.

After kicking off an inflation-fighting campaign last year with a 25-basis point increase in March, the Fed quickly accelerated the pace of rate hikes, increasing the federal funds rate by 50- and 75-basis points at a time.

A basis point is one-hundredth of a percentage point. So the 75-basis point hikes approved in June, July, September and November brought rates up by three-quarters of a percentage point at a time — three times greater than the increase approved Wednesday.

“In light of the cumulative tightening of monetary policy and the lags with which monetary policy reflects economic activity and inflation, [Fed policymakers] decided to raise interest rates by 25 basis points today, continuing the step down from last year’s rapid pace of increases,” Federal Reserve Chairman Jerome Powell said at a press conference.

“Shifting to a slower pace will better allow the [Fed] to assess the economy’s progress toward our goals, as we determine the extent of future increases that we require to obtain a sufficiently restrictive stance,” Powell said. “We will continue to make our decisions meeting-by-meeting, taking into account the totality of incoming data and the outlook for economic activity and inflation.”

In a statement, policymakers serving on the Federal Open Market Committee said they anticipate “that ongoing increases in the target range will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time.”

In a note to clients, Pantheon Macroeconomics Chief Economist Ian Shepherdson said there’s a good chance that the Fed is done hiking rates for now. But policymakers won’t make their intentions known until they see more data, Shepherdson said.

“In short, the statement recognizes that things are changing for the better, but the Fed is taking baby steps,” Shepherdson wrote. “Policymakers know that a ton of data is coming before the March meeting, including two months of CPI [consumer price index] and employment/wages data. We remain of the view that the chance of a pause in March is about 70 percent, but Chair Powell will go nowhere near that idea in the press conference.”

For now, Powell is suggesting that one more increase in March is inevitable but that future moves will depend on data.

The so-called “dot plot” released after December’s meeting — a poll of committee members’ projections of how much more rates will have to go up to combat inflation — suggested that the Fed saw the need to keep raising rates this year until the federal funds rate is just above 5 percent. That would imply one more 25 basis-point increase in March.

“We will be looking at the incoming data between the March meeting and May meeting,” Powell said. “I don’t feel a lot of certainty about where that [inflation] will be. It could be higher than where we are running down right now. If we come to the need to move rates up beyond what we said in December, we would certainly do that.”

The CME FedWatch Tool, which monitors futures contracts to calculate the probability of Fed rate hikes, puts the odds of one more 25 basis-point increase in March at 86 percent.

Some bond market investors are betting that the Fed will not only stop raising rates but bring them back down later this year if signs of a recession emerge. If the Fed pauses in March instead of May, that might be an indication that a recession is on the horizon, said Marty Green, principal with mortgage law firm Polunsky Beitel Green, in a statement.

“Most of our clients are forecasting another 25-basis point increase at the March meeting before the Federal Reserve pauses,” Green said. “But as inflationary data continues to show the economy is rapidly slowing, there is growing hope that the Fed might be in a position to pause interest rate hikes in March rather than in May. While interest-rate-sensitive businesses like auto sales and mortgage companies may welcome this development, it could indicate that the long-predicted recession may be here sooner rather than later.”

Despite rates declining for the fourth straight week, demand for purchase loans was down a seasonally adjusted 10 percent last week compared to the week before and 41 percent from a year ago, according to a weekly survey of lenders by the Mortgage Bankers Association.

“Overall application activity declined last week despite lower rates, which is an indication of the still volatile time of the year for housing activity,” MBA Deputy Chief Economist Joel Kan said in a statement. “Purchase activity is expected to pick up as the spring homebuying season gets underway, bolstered by lower rates and moderating home-price growth. Both trends will help some buyers regain purchasing power.”

Yields on 10-year Treasurys — a useful barometer of where mortgage rates are headed next — dropped sharply after the Fed’s announcement.

With the Fed thought to be nearing the end of its interest rate hike campaign, the wide “spread” between 10-year Treasury yields and mortgage rates could return to something closer to historical norms.

“The spread between mortgage rates and the 10-year Treasury has been abnormally wide since early 2022,” Kan said. “Further narrowing of that spread is expected to put downward pressure on mortgage rates in the coming months.”

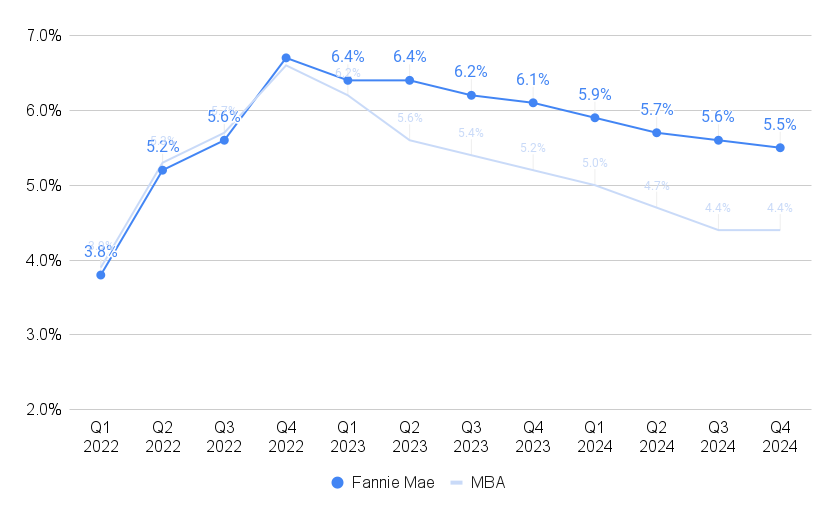

Mortgage rates expected to ease

Sources: Fannie Mae housing forecast, January 2023, Mortgage Bankers Association forecast, January 2022

In a Jan. 19 forecast, MBA economists projected rates on 30-year fixed-rate loans will drop below 6 percent during the second quarter of 2023 and below 5 percent next year. Fannie Mae economists don’t see mortgage rates falling below 6 percent until next year.

Fed policymakers also agreed to continue “quantitative tightening,” in which the central bank continues to unwind the massive debt purchases it made during the pandemic to keep interest rates low. The Fed is now shedding $35 billion in mortgage-backed securities and $60 billion in Treasurys each month.

Fed trimming balance sheet

As of Jan. 25, the Fed held $5.44 trillion of long-term Treasurys and $2.62 trillion in mortgage-backed securities. Source: Board of Governors of the Federal Reserve System, Federal Reserve Bank of St. Louis.

Since the Federal Reserve’s holdings of mortgage debt and Treasurys peaked at $8.5 trillion in April 2022, the central bank has trimmed its balance sheet by $442 billion.

Get Inman’s Extra Credit Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.