In any normal year in the last half-century, this would be the week in which markets and media became pre-occupied with the Fed — especially housing market participants, and even politicians.

This is the week in which the Fed’s new hiking cycle began to bite. Mercifully for new chair Jay Powell, fog and smoke billowing from other parts of government make perfect cover for the Fed, for a little while longer. The Fed’s hikes have not yet affected the real economy, but when mortgage rates pierce 5.00%, a whole lot of people will notice.

The Fed’s ideal public profile is irrelevance, if not complete invisibility. It dropped the overnight cost of money to “0%-.25%” ten years ago. Five years ago it began to threaten rapid hikes which never happened, a combination of hold-us-back and “Wolf!” which gradually bored markets into not paying attention.

The Fed did at last begin to raise the cost of money at the end of 2015. By .25% to 0.50%. And then waited a whole year to go to 0.75%. Yawn.

Last month it went to 1.75% — and promises to be at least 2.25% by the end of 2018. So help me, markets did not react until this week, and at that only in the most sophisticated way (yield curve slope). A few civilians are snorting to wakefulness, their ARM-reset letters this month jumping to 5.00% for both Libor- and T-bill-based adjustable mortgages.

“Well! Harrumph. I’ll just refinance.” Uh-huh. How does 4.75% sound — while it lasts?

Historically, housing is central to Fed cycles. We are the first to overheat, the first to faint when the Fed hikes a lot, which marks the onset of recession, and the first to recover. Today, only one problem: we have no recognizable housing cycle. Housing overheating is one of the good reasons for the Fed to tighten — overbuilding makes recessions deep, and Fed interception is a good idea. However, today we have no overbuilding, except apartments in a few markets.

Is it in the Fed’s or the nation’s interest to thump housing while in a state of chronic under-supply? The Fed’s standard down-the-nose: “Monetary policy is unable to assist individual segments of our economy.” Um… not even the sector most sensitive to interest rates? Unfortunately, down-the-nose is correct. Feels lousy, though.

Traditionally and accurately, its rate “hikes” are synonymous with “tightening,” as in credit harder to get. Not this time, not yet. The Fed has already made cash the most expensive in ten years, but no sector reports that loans are harder to get.

Here’s the fun part. How high will the Fed have to hike before it is “tight?” Nobody knows. To slow the economy to a sustainable pace (GDP growth sub-2%, less than 100,000 jobs monthly), will the Fed have to choke credit, or just hike far enough? The most basic calibration of Fed altitude is the cost of money relative to the “neutral rate of interest,” known in econ-ese as r*, spoken as “r-star.” Higher than r*, the Fed is tight.

Where is r*? We Fed economists don’t know, so we say that r* is “not observable.” But when we went to 1.75% in March, we said we were still “accommodative,” meaning below r*, wherever it may be. Get your Ph.D, and then you can sound authoritative while guessing by saying “not observable.”

If all is so hazy, how do I get off with announcing in paragraph two, above, that this week the Fed’s hikes have begun to “bite”? On that we have good, solid data. The Fed has been oh-so-gradually pushing up on the cost of money, an overnight rate, but only this week has that up-pushing (from “underneath” as traders would say) moved long-term rates, specifically the 10-year T-note, which defines mortgages and a lot else.

Long-term rates go up and down with inflation. For the Fed by itself to alter long-term rates in the absence of material shift in inflation requires a lot of effort. To push down required an immense QE program. To push up gets a grudging response. In the months before and after the Fed’s last hike, both the Fed telltale 2-year T-note and 10-year froze — even though everyone heard the Fed’s intention to hike farther. 2s began to move up just ten days ago, to price-in the next hike. The 10-year did not move until two days ago. That lag is the marker of the Fed pushing up — nothing else happened to cause the move, just the Fed. That is a form of “tightening,” and the first in this cycle.

During that lag the spread between 2s and 10s reached the most narrow since the last recession, 2s at 2.32%, 10s at 2.73%. In this last week, 2s rose to 2.44% and 10s to 2.94%, the spread opening a bit. At some unknown moment 2s will rise above 10s — an “inversion” — and we’ll have the next recession.

I am a card-carrying Fed Fan. It is a lot of fun to tease them about unknowns, in the black humor of trading desks. Little that they do gets under my skin.

However: overconfidence is intolerable. Powell and new vice-chair Clarida are first-class appointments who are fully aware of how little they can know for sure.

My current least-favorite is John Williams, who got himself slid sideways from the San Francisco Fed to New York president, much higher prestige, will now vote at every meeting and is supposed to be the watchdog over markets. Williams on Tuesday exceeded all of my poor expectations, and invited fate to the party: “The flattening of the yield curve that we’ve seen is so far a normal part of the process, as the Fed is raising interest rates, long rates have gone up somewhat — but it’s totally normal that the yield curve gets flatter. My own forecast would be that interest rates are going to move up gradually, smoothly. It’s going to be like a 747 landing and people don’t even realize that they can turn their phones on.”

The gods of money are not pleased. He spoke the day before Southwest 1380.

————————————

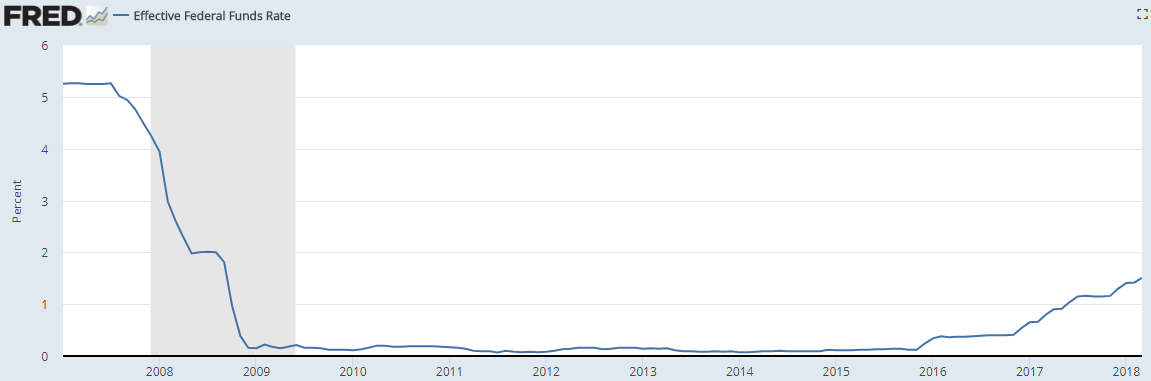

The Fed funds rate since 2007. Anybody would get sleepy:

Since 2013, the 10-year T-note in red, Fed funds in blue, the yield curve “flattening:”

In fine timescale, the 10-year in just the last year. The post-February stall is clear, as is the re-touch of the 2.95% February top. We’re back on alert for breaking 3.00%, and 5.00% 30-fixed mortgages.

Credit: The Wall Street Journal

To watch the Fed, watch the 2-year T-note (NOT, not ever, the Fed funds futures market). 2s also stalled into April, but the last ten days are unmistakable, and ahead of 10s.

Credit: The Wall Street Journal