- A recent analysis by the National Association of Realtors says that areas with high costs and high usage rates of FHA loans are hardest hit by the mortgage insurance premium reduction repeal, and that the FHA's healthy bottom line plus increases in mortgage interest rates warrant another look at the rate reduction.

January’s administration change left some homebuyers with the somewhat unexpected side effect of whiplash. The source? An 11th-hour mortgage insurance premium (MIP) rate reduction — and then a stroke-of-midnight repeal of that reduction.

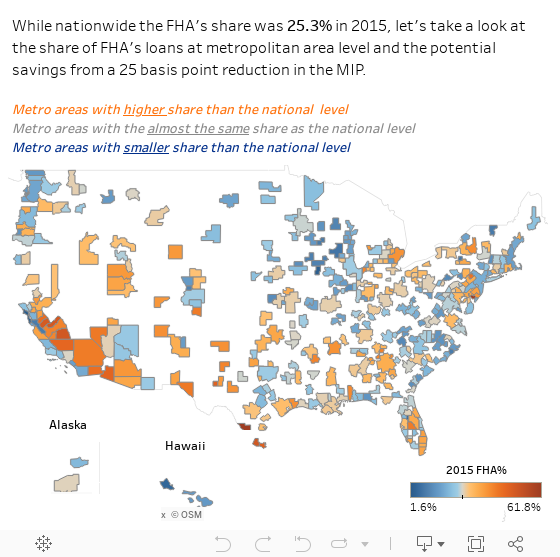

It’s politics as usual on one hand, but on the other hand, this reduction-and-repeal dance had a real impact on some markets where lots of buyers are leveraging Federal Housing Administration (FHA) loans — or where housing costs are unusually high. That’s what some new numbers show, courtesy of National Association of Realtors (NAR) economists.

What happened?

In January, the FHA announced that it planned to cut mortgage insurance premium rates by a quarter of a percentage point (25 basis points), from 0.85 percent to 0.60 percent, starting January 27. Borrowers whose down payment is less than 20 percent of the appraised value of the property must pay mortgage insurance on the loan — some FHA loans allow borrowers to put down as little as 3.5 percent.

The rate reduction was in line with NAR recommendations, says Ken Fears, NAR’s director of regional economics and housing finance.

“We first took a look at this last spring,” Fears noted. “A year ago, we began to push for a reduction; we didn’t necessarily specify a particular number, but we gave a window of 10 to 25 basis points.”

At that point, as NAR’s analysis from last year notes, the FHA’s books were looking healthy enough to give consumers a bit of a break.

“The health of the FHA’s Mutual Mortgage Insurance Fund, which pays FHA lenders when borrowers default on FHA-insured mortgages, has improved for four straight years, gaining $44 billion in value since 2012, according to HUD. The fund’s capital ratio now stands at 2.32 percent of all insurance in force,” Inman reported in January.

And because mortgage rates had been at near-historic lows for a while, it was reasonable to expect they’d eventually go up — which has officially happened, and mortgage rates could see further increases still — so it made further sense to consider a mortgage insurance rate reduction.

“If you reduced the fee slightly, it would benefit consumers — and as long as the rate remained above the break-even level, you’d continue to add to the reserves,” Fears added.

However, a week before the new mortgage insurance premium rate was supposed to kick in, on January 20, President Donald Trump indefinitely suspended the rate reduction.

Who’s hurting?

Fears says his findings for where consumers are feeling the effects of this rate reduction repeal are pretty much in line with his expectations:

- Buyers in high-cost markets

- Buyers in markets with heavy FHA loan utilization

“A lot of the areas that are impacted are what turned out to be the President’s base in the selection,” said Fears. “Pennsylvania, Ohio, smaller markets in Illinois — a lot of those are very heavy users of FHA loans.”

What next?

“With time, the FHA’s books are just going to continue to improve in the near term — that’s going to raise the onus more and more on why we are keeping those rates high,” predicted Fears. “We’ll have a lot more clarity, and there will be an incentive to change it.”

He adds that the Trump administration “has signaled that it’s going to review a number of policies that it’s frozen on implementation,” so there is hope that the rate reduction will be implemented at some point.

However, don’t wait for it, is his advice.

“People need to keep in mind that we don’t know when and if this will occur, so don’t wait to try and time it,” Fears said. “At the end of the day if you find a great opportunity to put someone in a house that they can afford and will enjoy, that’s what’s really the most important thing.”