After dipping below 6 percent last week for the first time in 2023 on hopes that the Fed is nearly done raising interest rates, mortgage rates are again on the rise, rebounding on the impact of last week’s strong jobs report.

Fed policymakers approved the smallest interest rate hike in nearly a year on Feb. 1 and signaled that the central bank was close to wrapping up its year-long rate-hike campaign. Bond market investors who fund most home loans responded enthusiastically, bringing mortgage rates to 2023 lows.

But the Feb. 3 jobs report surprised many economists, showing the U.S. added 517,000 jobs in January, up from 260,000 in December, helping keep the unemployment rate holding steady at 3.4 percent.

The report sparked fears that the Fed will need to stick to its guns and continue to raise rates — and keep them elevated for some time — to fight inflation. Federal Reserve Chair Jerome Powell confirmed those fears this week in a conversation with Carlyle Group co-founder David Rubenstein at the Economic Club of Washington, D.C.

“Had you known that the jobs report was going to be as strong, would you have done 25 basis-points, or something different?” Rubenstein asked Powell.

Powell confirmed that the jobs report was “certainly stronger than anyone I know expected” and “shows you why we think that this will be a process that takes a significant period of time.”

But Powell suggested that while bond market investors may have begun doubting the Fed’s conviction to continue raising rates, that was its message on Feb. 1 — one that he reiterated on stage with Rubenstein.

“We think that we’re going to need to do further rate increases, as we said, and we think that we’ll need to hold policy at a restrictive level for a period of time,” Powell said.

The Fed’s 25 basis-point rate hike on Feb. 1 brought the short-term federal funds rate to a target range of 4.5 to 4.75 percent.

The CME FedWatch Tool, which monitors futures contracts to calculate the probability of Fed rate hikes, puts the odds of another 25 basis-point increase in March at 91 percent, and calculates that there’s a 75 percent chance that Fed policymakers will raise rates by another 25 basis points in May.

But futures markets suggest that there’s only a one in three chance that the Fed will keep hiking into June, which would leave the target for the federal funds rate at 5.0 to 5.25 percent, up 50 basis points from today.

Mortgage rates hit 2023 bottom on Feb. 2

According to loan lock data tracked daily by Optimal Blue, rates on 30-year fixed-rate conforming mortgages briefly dipped below 6 percent on Feb. 2, the day after the Fed’s latest rate hike. But rates for 30-year fixed-rate loans have since climbed by more than 30 basis points, reaching 6.30 percent on Wednesday.

But from the perspective of homebuyers, the long-term trend has been positive, with rates steadily declining over the last three months from a 2022 high of 7.16 percent registered Oct. 24.

A weekly survey by the Mortgage Bankers Association shows demand for purchase mortgages was up a seasonally adjusted 3 percent last week compared to the week before, but down 37 percent from a year ago. Requests to refinance existing mortgages jumped 18 percent but were down 75 percent from a year ago.

Joel Kan

“Both purchase and refinance applications increased last week and have shown gains in three of the past four weeks because of lower rates,” said MBA Deputy Chief Economist Joel Kan in a statement. “Purchase activity that was put on hold last year due to the quick runup in rates is gradually coming back as rates ease and housing demand remains strong, driven by supportive demographics and the ongoing strength in the job market.”

Fed trimming balance sheet

As of Feb. 1, the Fed held $5.40 trillion of long-term Treasurys and $2.62 trillion in mortgage-backed securities. Source: Board of Governors of the Federal Reserve System, Federal Reserve Bank of St. Louis

While Powell continues to stress the Fed’s determination to keep short-term rates high, he did provide assurances this week that policymakers won’t be hasty in unwinding the support the central bank provided to mortgage markets during the pandemic by buying trillions in Treasurys and mortgage-backed securities (MBS).

The Fed has been trimming its balance sheet by letting those securities mature rather than selling them off. Through that process, the Federal Reserve is now reducing its holdings of mortgage-backed securities by $35 billion a month and its Treasury investments by $60 billion.

Powell said Wednesday that although the Fed could sell mortgage-backed securities if needed to fight inflation, “that’s not on the list of things that are being actively considered.”

The Fed is likely to be content to let maturing assets roll off its balance sheet for “a couple of years” before reassessing its strategy for trimming its debt holdings.

While the “quantitative easing” that the Fed undertook helped the economy weather the pandemic by keeping interest rates low, Powell warned that it can’t protect the economy if Congress does not raise the federal debt ceiling.

“Our only role in this is that we’re the fiscal agent of the Treasury Department. We’re not a policy maker on that,” Powell said. “And I will just say this, this really can only end one way — and that is with Congress raising the debt ceiling in a timely fashion so that the U.S. can pay all of its bills. That’s what has to happen. And if that doesn’t happen, no one should think that the Fed has the ability to shield the financial markets or the economy and the consequences of moving too slow.”

While the Federal Reserve is still worried about inflation, bond market investors’ lack of enthusiasm for short-term bonds could be a signal of an impending recession.

A closely watched indicator that’s predicted past recessions — the spread between 2-year and 10-year Treasury yields — is “deeply inverted” and approaching levels not seen since October 1981, MarketWatch reports.

Yield curve is ‘deeply inverted’

One view is that the economy could be heading into a period of “transitory disinflation” if recent easing of inflation turns out to be fleeting, MarketWatch‘s Vivien Lou Chan reports. Or, a “swift and surprising drop in inflation” could lie ahead with the U.S. economy unable to avoid a recession.

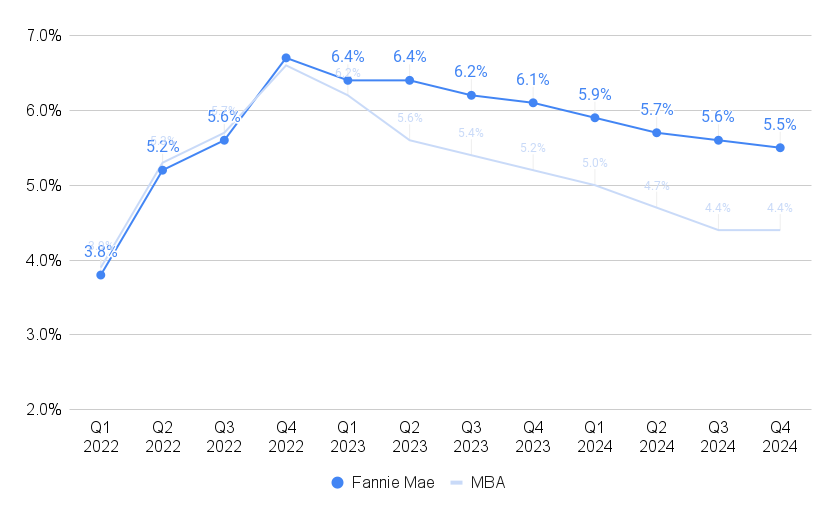

Mortgage rates expected to ease

Sources: Fannie Mae housing forecast, January 2023, Mortgage Bankers Association forecast, January 2022

Expectations that the Fed is nearly done raising short-term interest rates — and could even reverse course and lower them again if the economy slips into a recession — explain forecasts that mortgage rates will continue to decline this year and next.

In a Jan. 19 forecast, MBA economists projected rates on 30-year fixed-rate loans will drop below 6 percent during the second quarter of 2023 and below 5 percent next year. Fannie Mae economists don’t see mortgage rates falling below 6 percent until next year.

Get Inman’s Extra Credit Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.