Better Home & Finance and Coinbase have funded the first Fannie Mae-backed mortgage collateralized by Bitcoin in the United States, the companies announced last week, and plan to make the product available to qualified borrowers nationwide by this summer.

The loan closed on behalf of a couple in their early 30s in Ann Arbor, Michigan, a software engineer and a graduate student who had accumulated meaningful savings in Bitcoin but lacked the cash for a conventional down payment.

Rather than liquidate their holdings and incur capital gains taxes, they pledged the crypto as collateral and closed on a home purchase. Better did not disclose the loan amount or the value of the Bitcoin collateralized.

“Buying our first home has always been the goal, but I wasn’t willing to give up a decade of investing to get there,” said Joe, Better’s first token-backed mortgage customer, whose last name was not disclosed in the press release. “With this mortgage, I didn’t have to choose. We closed on our home, and my Bitcoin stayed intact.”

The product launch is aimed squarely at a mismatch Better says it sees constantly in its pipeline: 41 percent of the company’s pre-approved customers qualify on income and credit but fall short on cash for a down payment.

Meanwhile, the median age of a first-time homebuyer hit a record high of 40 in 2025, according to the National Association of Realtors, as high mortgage rates, elevated prices and thin inventory have pushed traditional homeownership further into middle age.

‘A direct path to homeownership’

The product initially supports Bitcoin and USDC as collateral, with plans to expand to additional digital assets. Coinbase handles custody and compliance infrastructure on the back end. Better CEO Vishal Garg framed the product as a structural fix rather than a novelty.

“The 30-year fixed mortgage was designed for a generation that kept its savings in a bank account and built equity through a single employer,” Garg said. “That’s not the financial reality of millions of qualified buyers today that are building real wealth in digital assets.”

Better’s pitch to Fannie Mae almost certainly ran through Coinbase’s compliance and custody infrastructure. The exchange serves more than 150 government agencies and over 300 institutional clients, per the announcement. That’s a meaningful footnote for a product that needed a GSE’s blessing to exist.

“Tens of millions of Americans have built real wealth in digital assets,” said Mark Troianovski, Coinbase’s head of consumer and platform partnerships. “That wealth now has a direct path to homeownership, creating new opportunities for the next generation of homebuyers.”

For real estate agents working with younger, tech-sector buyers who’ve accumulated crypto over the past decade, the product is worth tracking, if only to understand when it might apply to a client who’s asset-rich but cash-constrained.

Bitcoin’s worst week since FTX

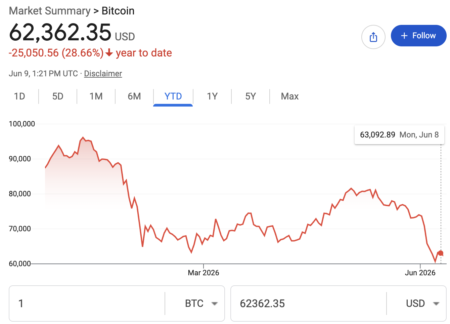

Bitcoin dropped below $60,000 last Friday, capping its worst week since the collapse of Sam Bankman-Fried’s FTX exchange in November 2022.

The proximate cause is that markets are repricing the interest rate outlook. Strong U.S. jobs numbers and an unresolved U.S.-Iran conflict have shifted Fed expectations from cuts to potential increases in some corners of the market.

Higher borrowing costs drain capital from speculative assets first, and crypto, perennially, is where that repricing shows up loudest.

The current correction is still, by historical standards, mild. Bitcoin has fallen roughly 50 percent from its peak. Prior crypto bear markets have seen drawdowns of around 80 percent.

After its 2021 top, Bitcoin took more than a year to find a bottom and another 15 months to reclaim its highs.

The timing is notable for Better, Coinbase and their Bitcoin-backed mortgage product. The product is built on a premise that makes intuitive sense in a bull market: Bitcoin holders who don’t want to realize capital gains can still access homeownership.

But a 50 percent drawdown, and the prospect of more, tests that premise. If collateral values fall fast enough, borrowers face margin-call dynamics that don’t exist with a conventional mortgage.