What kinds of products are included in the real estate technology landscape? How much of their funding is invested, and how much of it comes from agents and brokers? Where will we see the most growth in the next few years, and which verticals seem to be simmering down? Inman dug into the numbers, researched the investors, surveyed readers and interviewed the experts. Here are our findings.

A homeowner thinking about selling starts searching for local home value information online and stumbles across an iBuyer platform — one that will let the prospective seller offload the property in a specific and exact timeframe.

Meanwhile, a renter across town starts browsing for a bigger place and finds a wealth of information on rentals and entry-level homes for sale, all available on a real estate portal.

And the real estate agent who services either buyer or seller (or both) uses an array of technology products to do his job — from lead management tools to platforms that power his website to transaction management streamliners — even as the broker who oversees him uses office management software and probably uses technology to check in on her agents, too.

Welcome to the world of real estate services in 2017, where just about every aspect of the process, from lead generation to close, involves some kind of technology. And that’s not looking likely to change: Investment in real estate technology is up so far this year from last year, which means people on Wall Street who know how to make money (and lots of it) are increasingly seeing opportunities in real estate technology services — to the tune of billions of dollars.

That’s not entirely surprising, considering that the global real estate value is estimated at $217 trillion, per CB Insights, and residential real estate accounts for $162 trillion of that amount.

It makes perfect sense, therefore, that there are quite a few tech companies trying to acquire some of those dollars by providing products or services to real estate agents, brokers, brokerages and franchisors — or consumers.

What kinds of products are included in the real estate technology landscape? How much of their funding is invested, and how much of it comes from agents and brokers? Where will we see the most growth in the next few years, and which verticals seem to be simmering down?

Inman dug into the numbers, researched the investors, surveyed readers and interviewed experts to try to figure out the answers to those questions. Here are our findings.

What falls under the ‘real estate technology services’ umbrella?

There are several different types or categories of products that can be considered part of the real estate technology services family — and not surprisingly, some of them are more attractive to investors than others.

We looked at the following real estate technology verticals:

- Agent tools — software, services and so on

- Listing portals and home marketplaces

- Virtual brokerages and hybrid brokerages

- Insights and analytics

- Investing tools

Two prominent verticals that we didn’t examine include proptech and fintech. Proptech includes the scope of property management technology — tools and software focused on leasing, rentals and property management.

Fintech includes the scope of financial technology — tools and software focused on crowdfunding or other investment sources to provide mortgage loan or down payment assistance services to consumers. Although both proptech and fintech involve critical aspects of the real estate industry, we chose to focus on the world of residential real estate sales technology services and tools.

According to Adi Pavlovic, technology strategist at Keller Williams International, the real estate industry is on track to do $3.5 billion in investment deals in 2017. That’s a big number — but although it’s big enough to attract the notice of a handful of giants in the investor world, those heavyweights are typically choosing one (maybe two) companies to invest in and seem to be more or less ignoring the rest of the real estate tech space.

That’s not entirely surprising to Mark Birschbach, managing director of the National Association of Realtors’ (NAR’s) Second Century Ventures fund and managing director of NAR’s REach program.

“If a technology is going to only service the real estate market, it’s really hard to get a venture-type return on that kind of a company,” he explained. “When you look at funds going into those kinds of companies, one of the key things that a venture/investor will look at is how big the company can get.”

Real estate is a large market from a property value standpoint — and also in terms of the sheer number of Realtors licensed in the country — so entrepreneurs might think there’s a huge opportunity to sell their product … and perhaps there is. But so far, some of the biggest success stories have surrounded products (like DocuSign) that provide a service for real estate and a number of other industries, too.

Agent tools

- Agent tools include a whole range of technologies that real estate agents use to manage their businesses and the transaction as a whole. This encompasses:

- CRMs (customer relationship managers)

- Listing marketing and display tools (such as 3-D listings or virtual reality solutions)

- Transaction management tools

- Website or marketing platforms

- Add-ons to other platforms (such as RealScout for real estate searches)

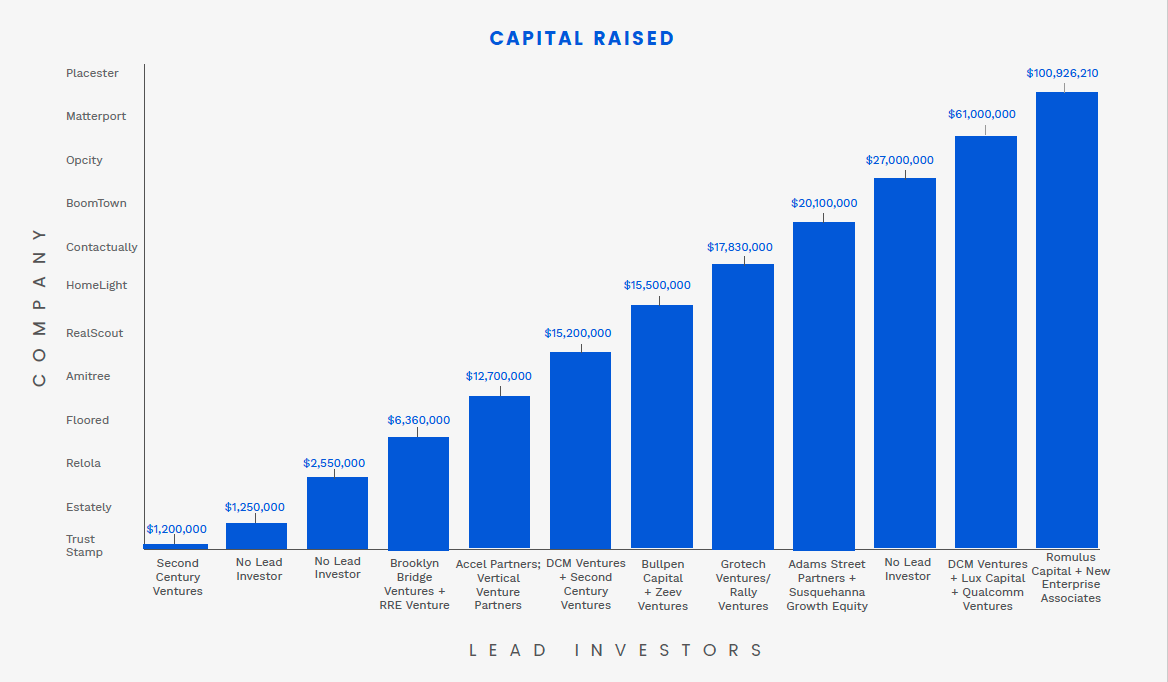

There are dozens — if not hundreds — of technologies that fall under the umbrella of agent tools, but the biggest real-estate specific tools that we identified (and their total capital raised to date) is as follows.

Placester has raised the most capital in the space — more than $100 million — followed by Matterport, with $61 million raised. Although they occupy different parts of the real estate agent tools vertical, both have acquired other companies on their growth journeys.

Agent tools represents a very fragmented vertical in the industry, opined Pavlovic. “There are so many tools, and it’s a little overwhelming for agents,” he noted.

“Our members aren’t spending thousands of dollars on technology solutions,” explained Birschbach. “Maybe some brokerages are and some high producers are, but when you really look at the numbers, there’s not enough money on the tools side of the equation where if you’re only servicing the real estate market, you can get a big return as an investor. So if you invest in this space, then in order to get that return, that tool has to be applicable outside of this space.”

“What’s interesting is that the trend is that an agent buys a CRM, and then usually the CRM has add-ons — you get an IDX website or transaction management, for example. They’re trying to be your one-stop hub,” Pavlovic added.

As a result, when one agent tool platform that has a solid foothold in one part of the market decides to expand into other areas, it can snatch market share away from existing participants.

“I talk to a lot of venture capitalists who want to understand how to do more in real estate tech,” Birschbach noted, “and I tell them that a real estate product that is real-estate specific has to have a really high percentage of the market to make it a worthwhile venture investment.” And it’s a competitive space, too, crowded with shiny objects.

One agent tools business model that Pavlovic thinks could pick up steam is lead nurturing or referral models, “where companies are buying leads online, nurturing them and selling them back to the agent with a referral fee,” he explained, noting that Referral Exchange is widely considered to have pioneered that model. “We’re seeing more and more of those companies — I’m not exactly sure why,” he said.

But one possible reason: “There might be a great deal of leads online that agents are struggling to sift through,” he noted.

Based in Boston, Placester was officially founded in 2011 by CEO Matthew Barba and COO/President Frederick Townes. It’s a clear investor favorite in the tools space, securing $100,926,210 in financing for its platform.

Placester offers an “all-in-one digital marketing platform” for real estate agents, which includes an IDX website, a CRM and lead management tools. It has products structured for individual agents, teams and brokerages.

As part of the Realtor Benefits Program, Placester gives Realtors a free IDX website, which it prices at a $240-per-year on its website. NAR members also get discounts on upgrades, which include everything from blogging, map search and lead capture to automated Facebook marketing and website maintenance.

An IDX website with lead management and drip marketing costs $150 per month for non-Realtors, and a premium package that adds lead nurturing, website setup and monthly content creation costs $400 per month for non-Realtors. Other add-ons include a “marketing accelerator” and an open home tool.

Placester acquired RealSatisfied, an agent review platform, on April 19, 2016.

It also acquired Homefinder.com, a home search platform, on March 5, 2016, but no longer owns HomeFinder as of February of this year, according to HomeFinder’s CEO.

Matterport was founded in 2011 by Matt Bell (currently the Chief Strategy Officer), Dave Gausebeck (currently the Chief Technical Officer) and Mike Beebe. Its mission is to establish 3-D and virtual reality (VR) models “as a primary medium for experiencing, sharing, and re-imagining the world,” and CEO Bill Brown was formerly the general manager of Converged Consumer Solutions at Motorola Mobility.

It lists four industries on its website as main areas of focus: residential real estate, multifamily real estate, engineering and construction, and travel and hospitality. It’s raised $61 million since its inception and launched a proprietary camera in 2014 that captures 360-degree images plus software that stitches those images into a full guided tour of any property or space.

Matterport also lists a network of 3-D photographers that branches to every state in the United States plus more than 70 countries globally. Those service partners are independent contractors that set their own rates for capturing 3-D images.

On July 14, 2016, Matterport acquired “360 virtual tour company” Virtual Walkthrough.

Listing portals and home marketplaces

When most agents and brokers think about disruption in the real estate industry, this is probably the vertical they’re picturing — containing such giants as Zillow and Opendoor, for example.

However, although Zillow in particular has become one of the biggest names in real estate, experts don’t believe that the search space will see much major activity from new players in the near future.

“The number of companies attacking search have declined substantially,” Pavlovic said. “Over the last three years, we had seen a lot of copycats enter the search space due to Zillow’s success and the IPO, and we’ve seen less and less of those companies.”

That doesn’t preclude established players deciding to dip their toes into the search waters, though, he added.

“Amazon and Nextdoor made some announcements,” he noted, “and we anticipate some other larger players might enter the space. But smaller players will be less likely.”

Companies solving a new problem are always welcome, Birschbach said — but they can’t keep tackling a problem that’s already been well-tackled.

“A RealScout is solving a different problem than a Zillow or realtor.com,” he explained.

Internationally, the amount of funding being pumped into search platforms is noteworthy — Chinese real estate portal Aiwujiwu (iwjw.com) has secured $305 million in capital, and Indian portal Housing.com raised $159.2 million — and comparatively speaking, American portals haven’t seen similar interest from investors. Trulia secured $32.8 million and Zillow $96.6 million in pre-IPO funding before teaming up and going public as Zillow Group.

Zillow Group, in fact, is one of the aforementioned established players seeking new territory — most recently the home marketplace territory with its Instant Offers announcement. That means that sooner or later, it will be competing for “iBuyers” with companies like Opendoor, which has secured a whopping $320 million in financing and is fully focused on the real estate transaction.

“There are a lot of tech companies and investors who think the homebuying and selling process is really inefficient — or that there’s a potential to, using technology, make that process more efficient,” Birschbach explained. “What they’re trying to facilitate is quicker closes, certainty of close and certainty of price, disrupting a sellers’ life potentially less than the typical process.”

For this kind of platform to work, he noted, the buyer of the property — the platform itself — is most likely assuming the risk of reselling it at a higher price in a specific window of time, and there will be a profit margin they need to hit on that sale.

“You have to have really efficient pricing mechanisms on the front side of it,” he said. Those pricing mechanisms might operate perfectly in a hot market — but, he asked, “what happens in marketplaces where housing isn’t great?

“Now you as an investor are really long in an asset class that you don’t want to be long in; how do you get out of that asset class or manage your portfolio of that asset class when the market isn’t good? Do all those investors lose a ton of money and disappear? That’s a real potential risk in the housing market,” he added.

Despite the potential risk of market upheaval, Pavlovic said that Opendoor’s fundraising efforts and Zillow’s launch of Instant Offers have sparked increased interest in these types of platforms. “We think it’s a domino effect,” he said, and “entrepreneurs are taking advantage.”

Founded by Rich Barton — a former Microsoft executive and also the founder of Expedia and Glassdoor — and Lloyd Frink, Zillow’s Series A in 2005 raised $32 million for the listing portal. In the 12 years since its Series A, Zillow went public in July 2011 before acquiring Trulia for $3.5 billion in stock to form listing portal powerhouse Zillow Group on July 28, 2014.

Zillow Group is currently helmed by CEO Spencer Rascoff and COO Amy Bohutinsky. The company has acquired a number of real estate technologies and platforms besides Trulia:

- Diverse Solutions, an MLS/agent IDX website platform, for $7.8 million on November 2, 2011 (sold in September 2016 to Market Leader, which Trulia acquired in May 2013 for $355 million and which Zillow later sold in September 2015 for $30 million)

- RentJuice, a rental relationship management service, for $40 million on May 2, 2012

- BuyFolio, a tool to streamline the homebuying process, for an undisclosed amount on October 31, 2012 (ceased operations March 2015)

- Mortech, a mortgage technology software company, for $12 million on November 6, 2012

- HotPads, an apartment and home rental search engine, for $16 million on November 26, 2012

- StreetEasy, a New York City-based listing portal, for $50 million on August 19, 2013

- Retsly, a platform for creating real estate software, for an undisclosed amount on July 16, 2014

- Dotloop, a transaction management platform for real estate agents, for $108 million on July 22, 2014

- Naked Apartments, an apartment rental matching service, for $13 million on February 3, 2016

Zillow Group has also ventured into other real estate verticals by means other than acquiring a new company; in 2008, it started the Zillow Mortgage Marketplace, where consumers can obtain quotes from lenders, and earlier this year it launched Zillow Instant Offers, which connects homesellers with investors (and potentially a real estate agent, too, if desired).

Zillow Group expects to pull in more than $1 billion in revenue this year, and most of its Q1 2017 revenue came from Premier Agent advertisers. It hopes to focus on growing its audience and its Premier Agent program this year. The company’s operating costs and its commitment to research and development funding means it’s usually operating at a loss — last year’s was $220 million and 2015’s was just shy of $150 million.

One of the first and certainly the most well-funded of the home marketplace entrants, Opendoor’s Series A was a comparatively mild $9.95 million — but in December 2016, it raised a Series D to the tune of $210 million.

Founded by current CEO Eric Wu along with JD Ross, Keith Rabois and Ian Wong, Opendoor caters to homesellers by offering convenience — they can sell those homes directly to Opendoor on whatever timeline is best for them. The company charges a service fee that it says typically ranges between 6 percent and 12 percent of the home’s price. For buyers, it offers all-day open houses and a similarly streamlined purchase process. It also has a subsidiary company,

Opendoor Mortgage, which provides home loans to buyers, quietly rolled out a title arm earlier this year, too. It’s operational in Phoenix, Dallas-Fort Worth, Las Vegas and Atlanta.

Although Opendoor’s funding to date is noteworthy — and the company has continued to expand since launching in July 2014 — critics note that it has only operated in a “hot” housing market environment and question its ability to sell homes for a profit quickly if (or when) the market slows down.

Overview: Virtual brokerages and hybrid brokerages

What’s the difference between a virtual brokerage or hybrid brokerage and a traditional brokerage?

A franchisor obviously has a particular slant, but Pavlovic defines them as “companies that are building technologies first and trying to recruit agents second.”

As one of the people responsible for managing Keller Williams’ technologies, he thinks this puts the hybrid model at a disadvantage because “you need to build tech with agents and have a good population to test things with and a large enough sample size across the country. Agents interact with technology differently across the country, and companies that invest in technologies first usually aren’t solving the problems they think they are.”

“In any successful business, if you can cost-effectively serve your client and they’ll refer more business to you, then you’re doing a really good job,” said Birschbach. “I think it really comes down to the consumer experience and the value being provided. Real estate is a hyperlocal business, and the more information you have about the local marketplace, the better you’re going to be able to service your clients,” and with tech-focused brokerages, that means it really comes down to how agents are using those tools.

“It’s a very challenging model with huge overhead,” Pavlovic added.

Still, with Compass’ valuation at $1 billion and Redfin recently going public, it’s a space that’s attracted quite a bit of investor attention — including a billionaire private investor, Takeshi Sekiguchi, who’s put at least $200 million into his own brokerage, SRE.

Without seeing the quarterly statements of any of these brokerages, it’s tough to see how well they’re doing in the marketplace, but virtual brokerage eXp Realty has posted a loss in the past couple of calendar years, and growing profits for public real estate companies like Realogy and Re/Max indicate that these traditional brokerage giants have no intention of giving up a slice of their market share without a fight. What’s more, Realogy’s profit margins mean that it can spend in excess of $150 million ($166 million, to be exact) on real estate agent technology products like ZipRealty.

Compass cofounder Ori Allon has a high-profile tech pedigree — after graduating with a PhD in computer science from the University of New South Wales in Sydney, Australia, he sold his patented thesis work, Orion, to Google (Orion is an algorithm to improve search refinements) before selling another company, Julpan, which analyzes real-time social media activity, to Twitter in 2011. Then he served as Twitter’s Director of Engineering before founding Compass alongside Robert Reffkin.

So it’s no surprise that the brokerage is known for its technology focus and has attracted investor attention from outside the real estate industry that would be impossible for most brokerages to manage.

Its $8 million seed round in December 2012 was paltry compared to its most recent fundraising round — $75 million in Series D funding.

Compass operates in a handful of high-price-point real estate markets around the country and is known for offering significant sums of money to established top-producing agents when it moves into a new region in order to hit the ground running in terms of market share and agent power.

You can find Compass agents and listings in:

- New York City

- Miami and Fort Lauderdale

- Greater Boston

- Aspen

- Santa Barbara and Montecito

- The Hamptons

- Washington, D.C.

- Los Angeles and Orange County

- The San Francisco Bay Area

The company also recently hired a “chief people officer” from Facebook and replaced its CFO.

At the end of fiscal year 2016 — on June 30, 2017 — Seattle-based Redfin announced its IPO, and that public offering launched less than a month later on July 28. The upstart real estate brokerage is operational in 44 states and provides technology to its agents (who service both homebuyers and homesellers) as well as a listing portal where buyers can save “favorites” and homeowners can claim their home via a dashboard (similar to Zillow’s) that alerts them to perceived value changes that Redfin’s algorithm detects.

Founded by David Eraker, Michael Dougherty and David Sellinger, Redfin is currently operated by CEO Glenn Kelman. Eraker founded Seattle brokerage Surefield after his Redfin days, and regulatory filings connected to Redfin’s IPO indicate that he is taking legal action against the company for alleged misconduct surrounding a patent application “that has not issued and does not cover our current products and services,” according to the filings.

In July, Redfin launched a test of an Opendoor competitor, which would give homesellers the opportunity to sell their properties directly to the brokerage.

Kelman has made a point during his CEO tenure to promote transparency regarding gender and minority gaps in pay, and Redfin has created several initiatives to track its own progress and promote better practices surrounding women and minority employees.

Insights and analytics

Real estate data is everywhere, but now that it’s become more publicly available, companies are sprouting up to aggregate that data and (in experts’ favorite examples) use it to predict how people are likely to behave. Also known as “big data,” it’s a space that Birschbach thinks is “already huge, and I think is only going to get bigger.”

But those companies need to go beyond aggregating the data and putting it in a dashboard. “What’s more interesting in that space is: I have all this data; it’s the best data out there, and my data scientists have run all sorts of programs and algorithms to figure out how to predict behavior based on the data we have.”

This is a tactic that retailer and consumer brands have been taking for a while now — in order to try and pinpoint what consumers might want to buy before they know.

“I think these kinds of companies are just scratching the surface on what predicts behavior,” Birschbach added. “What’s going to predict when a consumer’s likely to list their home, for what reason — and how do you get in front of that consumer at that time, or even before they know they want to list?”

Canadian tech-based real estate valuation company Real Matters launched its IPO in May of this year following seven years of investment rounds, one of which netted nine figures. It provides valuation and other services for mortgage lenders and insurers and claims to provide its services to 60 of the 100 biggest mortgage lenders in the United States and three of the five biggest banks in Canada.

Real Matters operates two subsidiaries:

- Solidifi, a real estate appraisal management company

- IV3CUS, a property inspection and risk assessment company

Both Solidifi and IV3CUS have made acquisitions in the past few years:

- IV3CUS was thusly named after Real Matters subsidiary IV3 Solutions acquired Canadian Underwriting Services and the joint entity was renamed

- Solidifi acquired appraisal management company Kirchmeyer & Associates in January 2013

- Solidifi acquired home equity lender servicer Southwest Financial Services in May 2015

- Solidifi acquired Linear Title and Closing in April 2016

Real Matters’ field agents help with valuations, inspections, title searches and closings in the real estate transaction sphere.

Investing tools

Another area of growth in the real estate technology space is investing tools — platforms that make it easy for consumers to invest in real estate themselves, typically through some kind of crowdfunding setup.

Turning those ideas into a lucrative business model can be “challenging,” said Birschbach, “because there are two sides of the equation, a supply side and a demand side — buyers and sellers.”

Sellers won’t pay much attention to platforms that don’t have a healthy population of buyers, and buyers feel much the same way; they have little interest in spending their time on platforms that don’t have a wide selection of inventory. “So there’s a chicken-and-egg problem with creating marketplaces — that’s problem no. 1.”

The second problem, he thinks, is that “real estate is one of those look-and-touch-and-feel asset classes.” Even though consumers can now easily invest in stocks, for example, “they go for the names they know — they’ll invest in Microsoft and Apple and Google and Facebook and these companies they know in their daily lives.”

As a result, “it’s hard to get consumers on a real estate platform because they don’t know enough about real estate as an asset class — and can you sell a building online or a piece of a building online when the investor, the consumer-type investor, doesn’t know the property, doesn’t live near it, doesn’t understand what the dynamics of the cash flows associated with the property are, and so on?” he asks.

And as far as the professional investors go, they’re usually using a platform that they already like. Why should they switch to a new one?

Investment marketplace Cadre has emerged as the best-funded among the real estate investment platforms available today — in June of this year, it received a $65 million infusion from Menlo Park notable investor Andreessen Horowitz (a16z), which has also given money to Facebook, Twitter, Groupon and other very high-profile tech platforms.

Cadre allows individual investors, larger groups and institutions and anybody in between to invest a minimum of $100,000 in a real estate transaction — primarily commercial real estate. It also has a managed account option that lets investors diversify their investments into more than one transaction.

On its website, Cadre says that it typically pursues “transactions requiring a minimum equity investment of $15 million” and that the hold periods are typically four to seven years.

What kind of return are agents seeing?

Inman’s reader survey found that although some readers are investing heavily in agent tools and portal advertising, few of them could articulate their return on investment (ROI).

“I think it’s hard to measure,” Birschbach said. “That’s really the challenge with measuring ROI on everything; 20 years ago when people were advertising in the newspaper, unless a client who called up said they saw the ad in the newspaper, you couldn’t measure an ROI on that.”

Of course, newspapers had distribution statistics and readership numbers, and today agents and brokers can get even more insight into their audiences by tracking clicks and IP addresses — but that doesn’t make ROI any easier to measure, “especially when there’s a halo effect to what you do,” he said.

Tips for tech companies seeking a foothold

To that end, there’s a real opportunity for tech companies who can help calculate ROI for users. “It helps give them a competitive advantage when selling their product,” Birschbach opined.

More broadly, Pavlovic says that he thinks real estate startups are going to find the most success in incubator models.

“I think those models are really good because one of the biggest challenges as a startup entering real estate is understanding the complexity of the industry you’re trying to solve — it’s challenging, and there are a lot of regulations around it,” he said. An incubator, however, “can take six months to hold their hand and introduce them to the industry.”

Birschbach also notes that real estate technology companies need to understand that their market capture strategy needs to extend beyond landing a few big names.

“At the end of the day our members are independent contractors; they can choose to use anything they want,” he explained. “So as a tech company, how do you get traction in this space? All the companies come in thinking ‘If I just go sign up Re/Max, Realogy and Keller Williams, I’m done.’

“What they don’t realize is that every single agent who works for those brands is an independent contractor; they don’t have to use anything that those large companies support,” he added.

“Even if they pay for it for all of their agents, there’s still a sale that has to take place at the user level, which is the agent level.”

As a result, he advises that instead of being all things to all people, “Why don’t you start being one really, really, really good thing to a lot of people — and then you can expand from there.”

Tips for agents (and brokers) looking to the future

Should agents be worried about the proliferation of online marketplaces? Experts largely think not.

“I hear real estate agents compared to stockbrokers,” Birschbach said. “At least across names of stocks, a share of a stock is a share of a stock is a share of a stock is a share of a stock. A home is not a home is not a home — they’re all different.”

In addition, a home is a much bigger asset than one stock, and that means many consumers are likely to be more cautious with it. “There’s no way these individuals can do what a typical buyer who’s working with one of our members would do — go in, see the home, walk through it, do the inspection, understand what the issues are, negotiate price and figure out what value it’s worth,” he added. “They’re using big data and predictive analytics to figure it out, take a bigger fee than agents would to build in this cushion, and taking price and resale risk on it, which makes it really important that my algorithms work to price the home correctly.

“My perspective is, I think they can do that in good housing markets — just like any market you’re going to invest in: Everything’s easy when you’re winning,” he added. “When it gets really hard is what happens if and when the market turns, because it always does.”

There will be some more disruptive technologies entering the marketplace, he thinks — but they’ll most likely be variations on new features already out in the marketplace in some form or another.

“There are all the big buzzwords — crowdfunding and big data and drones and all these cool things we were talking about two years ago, which wasn’t that long ago but seems like forever ago,” he noted. “Now it’s artificial intelligence and blockchain, the new buzzwords.”

Those are different from the software solutions, which always will find a foothold in the market if they solve a problem more efficiently or easily.

“If you look at it from a market saturation standpoint, you think the market is saturated and there can’t be any room for new players,” he explained, “but there can be room for new players that are solving a problem in a new and different way, and then existing players go away or adapt to the new player and make a better solution.” So that’s one place to look for disruption.

Another? Back to the buzzwords. “Artificial intelligence will affect not just real estate but every industry,” predicted Birschbach. “And we’re just scratching the surface on what blockchain is and what it can potentially be used for.

“There’s real stuff happening, but I think mass adoption of it is all hypothetical right now. We keep our eye on both,” he concluded.

PDF and graphs designed by Shimeah Davis.