2017 will be remembered as the year the water came.

Hurricane Harvey dropped as much as 60 inches of rain on parts of Houston, shattering American meteorological records. Hurricane Irma was the strongest tropical storm ever recorded outside the Gulf of Mexico and the Caribbean Sea, and plowed through Florida in early September, turning Miami’s main drag into a raging river.

And Category 4 Hurricane Maria pulverized Puerto Rico with 150-mph winds, leaving the island in darkness and ruin. Altogether, the three storms will cost the U.S. more than $200 billion, which would make 2017 the most expensive hurricane season on record.

Yet there is every reason to expect that the towns and the cities hit by the hurricanes of 2017 will be rebuilt — even, eventually, devastated Puerto Rico. Thank the federal government — when a storm or flood strikes a community, Washington is there with generous disaster relief, either through billions of dollars in direct aid or through the cushion of federally-subsidized flood insurance plans.

The confidence in the federal government’s backing keeps lenders sending money to disaster-hit communities, which encourages residents to stay put and rebuild, rather than flee for safer areas. This in turn ensures that tax money keeps flowing to local governments.

That’s why New Orleans, more than 10 years after suffering through one of the worst hurricanes on record, now has a tax base twice as large as it did before Katrina, and why the South Florida city of Homestead is nearly three times as populous as it was before Hurricane Andrew flattened it in 1992.

But disaster aid and insurance are meant to respond to occasional catastrophes. What will happen as the seas rise and major flooding goes from the occasional to the near constant? What will happen when climate change remakes the coastal communities where 39 percent of Americans now live? What happens when the water comes to stay?

New York City housing risks due to sea-level rise in a 2017 Zillow report. Credit: Zillow

Rising seas, looming crisis

A growing number of experts fear that sea level rise and flooding will devastate coastal real estate values, which in turn could cause the U.S. housing market to suffer a crash worse than 2007-2008 financial crisis.

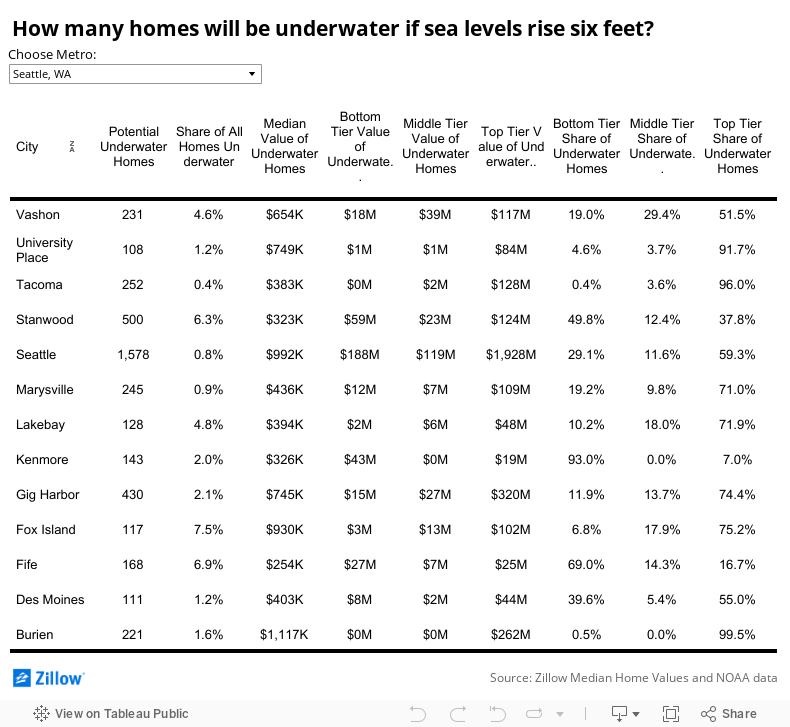

As seas continue to rise — with levels projected to increase by as much as six feet by the end of the century — flooding will become more common and more devastating. (A recent Zillow report found a six-foot rise in sea level by 2100 would likely submerge 1.9 million homes.)

Eventually insurers could begin to pull out of coastal markets altogether, as could lenders who fear that homes won’t be able to retain their value through the lifespan of a 30-year mortgage. Unable to get insurance to repair their repeatedly flooded properties — and tired of navigating the now constant risk of water–homeowners might end up desperate to sell, only to find that no one wants to buy.

Flooding in South Beach, Miami. Credit: maxstrz/Flickr/CC-by-2.0

The result would be a wave of defaults — while homeowners tried to keep paying their mortgages when their homes were financially underwater during the crisis, they’re more likely to give up if their home is actually underwater. They would know that there would be no hope their flooded homes would ever regain value.

“All of a sudden we’re going to reach a tipping point and no one will touch these mortgages,” says Edward Golding, a fellow at the Urban Institute and the former head of the Federal Housing Administration. “At some point it becomes undesirable risk and people start pulling out from entire regions.”

When that happens, coastal communities will enter a death spiral, as property taxes vanish even as the cost associated with responding to ever more frequent floods rises. “You don’t need to be too smart to figure out how this affects your tax base,” says Philip Stoddard, the mayor of South Miami. “No one is going to buy or invest in the community after that. This is not going to be pretty.”

We can’t say we haven’t been warned. According to Zillow’s recent report on sea level rise, in Miami alone, 30 percent of the city’s homes could be underwater — sinking over $16 billion property value.

And the impacts of sea level rise would be felt far earlier than the end of the century — a recent study by the Union of Concerned Scientists (UCS) estimates that the number of communities facing chronic inundation from rising seas will nearly double in some 20 years — less than the lifespan of most mortgages. (The environmental group classified “chronic inundation” as flooding that occurs at least 26 times a year over 10 percent or more of a community’s usable, non-wetland territory.)

No less than Freddie Mac’s chief economist Sean Becketti raised the alarm in 2016 with an article raising concerns that the housing market wasn’t prepared for the day when rising seas would puncture a coastal real estate bubble. “We can see this coming and take steps to make sure it’s not a crash,” says Rachel Cleetus, a senior economist at UCS. “But we have to stop putting our heads in the sand and pretend this isn’t coming.”

Yet that’s exactly what’s happening. Despite the warnings about sea level rise — and the object lessons of Hurricanes Harvey, Irma and Maria — coastal real estate is still hot, and the number of Americans living on the coast has increased nearly 45 percent since 1970.

A recent report by Attom Data Solutions found that the riskiest 20 percent of U.S counties have the most homes, the highest average home values and the greatest price appreciation in recent years. Since the end of 2010 media home prices in and around Miami have risen 120 percent, three times the national rate. Nor is this merely a matter of sunny Floridian optimism. New York City, which is just coming off the fifth anniversary of the devastating Superstorm Sandy, has welcomed continued development along its vulnerable waterfront.

Never mind that a recent study projects that within the next three decades, New York could be experiencing Sandy-like flooding every five years. “In general we underestimate the risk from sea level rise even when we can calculate it,” says David Titley, director of the Center for Solutions to Weather and Climate Risk at Penn State University and a former rear admiral in the U.S. Navy.

The difficulty of risk-assessment in coastal regions

It doesn’t help that it’s difficult for ordinary homebuyers to properly calculate the future risks from flooding and sea level rise. The Federal Emergency Management Agency (FEMA) maintains flood insurance rate maps, and if a property falls within what FEMA defines as a high-risk area for floods, a mortgage borrower must obtain a flood insurance policy — most likely one administered by FEMA itself under the National Flood Insurance Program (NFIP). (Most private insurers do not offer flood insurance, and many coastal communities would already be in dire financial straits without the net of subsidized government flood insurance, which is already billions of dollars in debt.)

But as a recent investigation by Bloomberg showed, many of FEMA’s maps are woefully out of date. That’s one of the reasons why less than 20 percent of Hurricane Harvey victims had flood insurance, even though the region had been repeatedly pummeled by tropical storms.

Sellers may be motivated to hide past flooding on a property or community — disclosure laws vary from state to state, but the National Association of Realtors (NAR), the nation’s largest real estate trade group, says that brokers and agents should disclose “actual knowledge” of previous property flooding or flood insurance purchases to buyers.

In any case, the very nature of climate change means that the past is no longer a reliable guide to future risk. “The Realtors get paid at closing and the builders get paid at closing, but the tail risk is with the homeowner who has equity in a property,” says Golding.

Hurricane Irma damage on Summerland Key, perhaps the hardest hit Key. Credit: Dan Chapman, USFWS.

That uncertainty can put potential buyers in a bind, as Diana Goulet discovered recently. Goulet, a California-based real estate investor, came to the coastal Florida town of Fort Pierce this summer to close on a $2.5 million piece of commercial property.

Goulet’s timing was less than ideal — just a few days before Hurricane Irma was due to strike the state. Incoming hurricanes have a way of concentrating the mind, and she was worried that sea level rise might leave property vulnerable to future storms. Those she talked to in Fort Pierce dismissed her worries, but she wanted to know more about the risks, and quickly. “I had a deadline to go ahead or pull the plug,” she says. “But there is a dearth of information out there.”

In the end Goulet was able to connect with Coastal Risk Consulting, a South Florida-based startup. Founded by Albert Slap, a retired environmental lawyer, and the climate scientists Leonard Berry and Brian Soden, Coastal Risk Consulting uses data from the Army Corps of Engineering and the National Oceanic and Atmospheric Administration (NOAA) to provide projections on risk from hurricanes, tides, and flooding on a property by property basis, for as little as $149 for single-family homes.

The company’s report convinced Goulet that her property was safe to buy, and she went ahead and closed. But while she’s glad for the peace of mind, she wonders how ordinary buyers who lack her resources and expertise might have managed. “I don’t think individual home buyers are savvy enough to recognize the risks, let alone try to mitigate them,” she says.

How coastal regions can prepare and mitigate

Firms like Coastal Risk Consulting are trying to give homeowners in vulnerable areas more information and more options around what will be the most important and valuable purchase they are likely to make in their lifetimes.

But while homeowners can take steps to protect their properties by raising elevations and moving vulnerable equipment out of flood-prone basements, Coastal Risk founder Slap is skeptical about the future of coastal communities on the front line of sea level rise. “We’re not going to see how bad it’s going to be until the virtual day it happens,” he says. “Flooding is inescapable because it creeps up on people.”

Smart coastal cities will begin borrowing and spending now to pay for defenses against the sea level rise to come. This Election Day voters in Miami supported a plan to tax themselves to pay for a $400 million bond, nearly half of which will go to pay for flood and sea rise protection. New York has a $20 billion plan in place that mixes recovery from Superstorm Sandy with infrastructure upgrades designed to protect the city’s nearly 600-mile long coastline from sea level rise and storms.

Superstorm Sandy damage in Rockaway, Queens, NY. Credit: Spencer Platt/Getty Images

Other coastal cities would be wise to follow those examples — soon. Credit ratings giant Moody’s made headlines last month when it released a report saying it will begin downgrading municipal bonds — which cities sell to investors to raise money — in places vulnerable to the effects of climate change, but not adequately addressing the risks. Moody’s cited Texas, Florida, Georgia and Mississippi as examples, but did not call out specific municipalities.

And as Henry Grabar pointed out recently in Slate, right now coastal cities like Miami can borrow money at low rates because lenders don’t seem to be worried that sea level rise and flooding will impinge on their ability to pay back those loans. If cities aren’t smart enough to take advantage of those rates to build up their defenses, their future could end up looking like Detroit’s — broke and too poor a credit risk to borrow enough to protect themselves from threats that worsen every day.

But even if richer cities can try to spend enough to protect themselves, that will still leave countless poorer communities in harm’s way. The Zillow study that looked at sea level rise found that a third of the homes that would be underwater by 2100 would be valued in the bottom third nationally. These are homes in often sprawling suburban and rural communities that lack the tax base now to pay for meaningful sea level rise defenses — let alone after constant flooding eats away at property values.

“You can easily use up every municipal budget doing the upgrades that need to be done,” says Stoddard, the mayor of South Miami. These are the homes that will wash away — and with them, the equity and dreams of hundreds of thousands of Americans.

It’s worth noting that in Florida, median home prices with the highest flood risk have risen more slowly over the past five years than those in cities with the lowest flood risk. But for now, the draw of the sun and the ocean will be enough to keep Americans living on the coast — and keep attracting more of them.

While mortgages may be for 30 years, the average home buyer only stays put for 13 years, which means that even if a homeowner is aware of the coming risk from sea level rise, they may believe they’ll have moved on by the time the water comes. But even if that’s true, the risk is merely being moved around, a shell game with the multi-trillion dollar housing market.

“It’s this slow moving disaster,” says Cynthia McHale, the director of insurance at Ceres, a sustainability nonprofit that works with investors. “No want wants to be left holding the bag. They want to party up until the ball drops on midnight.” But all indications are the party is coming to an end — soon.