Braden Crooks | Designing the WE

The federal government put it in writing.

Area descriptions attached to 1930s neighborhood risk maps used language like “detrimental influences: negro infiltration” to justify cutting off entire communities from federally backed home loans, Braden Crooks, co-founder of Designing the WE, told an audience at the National Association of Realtors’ 2026 Legislative Meetings in Washington, D.C.

TAKE THE INMAN INTEL INDEX SURVEY

The FHA’s own underwriting manual instructed lenders to assess whether “incompatible racial and social groups” were present and to predict whether a neighborhood might be “invaded” by such groups, he said.

“There’s no mincing of words,” Crooks said. “There’s no hiding anything.”

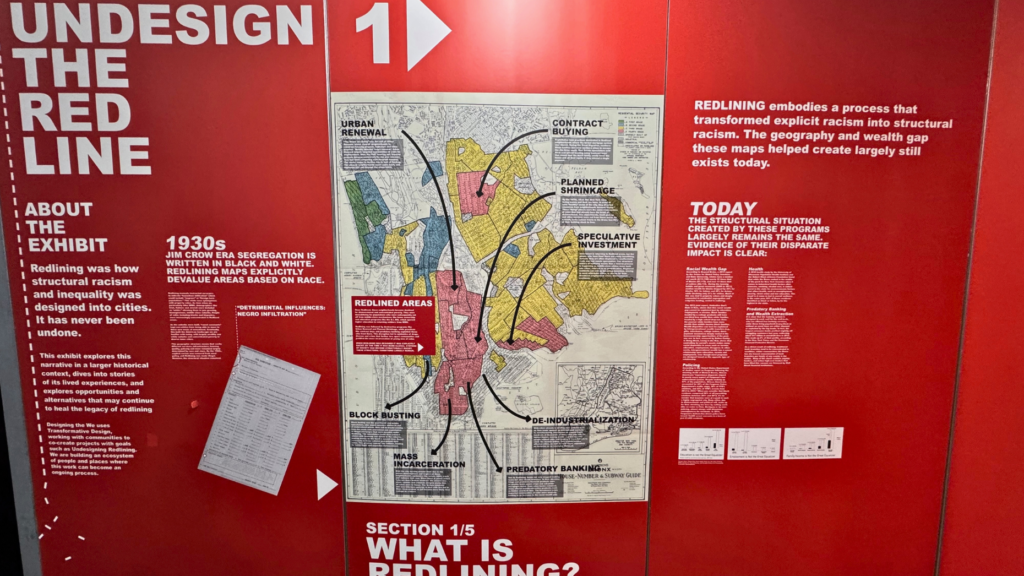

Crooks was presenting “Undesign the Redline,” a traveling exhibit Designing the WE brought to the NAR Expo at the Walter E. Washington Convention Center. The exhibit traces the history of redlining and its effects from Depression-era federal housing policy to the affordability crisis, wealth gap and appraisal bias that define today’s market.

A section of the display highlighted NAR’s fair housing advocacy work and examples of local associations taking action on affordable housing and fair housing across the country.

The maps that graded neighborhoods by race

The exhibit centers on maps produced by the Home Owners’ Loan Corporation in the 1930s and 1940s, which assigned color-coded risk grades to neighborhoods across 239 American cities. Green meant lend freely. Red meant hazardous.

The FHA used the same framework to determine where it would insure mortgages, effectively cutting off red- and yellow-coded neighborhoods from the loan products that built the American middle class, Crooks said.

The consequences were not incidental. Crooks stated that the geography of American cities today, with concentrated poverty in urban cores and wealthier, whiter suburbs surrounding them, has been a direct product of those policies. Property values in red-coded neighborhoods were sent on a cycle of decline, he said. Banks pulled out and businesses closed.

The Federal Reserve Bank of Chicago later showed that integrated neighborhoods before redlining had, in many cases, carried higher property values, Crooks said, meaning the property-value argument used to justify the maps was not only discriminatory but also false.

Private real estate reinforced the system

Private real estate reinforced the system. Crooks read from a private real estate textbook of the era, which argued that Black homebuyers should “forgo their desire” to live outside established districts because their presence caused “economic disturbance” in white neighborhoods.

A developer in Detroit, he said, built a six-foot concrete wall along Eight Mile Road to physically separate his all-white subdivision from a nearby Black neighborhood after the FHA initially declined to insure the project because it sat too close to the racial dividing line. The FHA approved the project after the wall went up, Crooks said. That wall, known as the Birwood Wall, is still standing today.

“Once this thing gets implemented into national policy, and they’re requiring banks, underwriters, mortgage issuers to look for racial composition, it becomes a self-fulfilling policy,” Crooks said. “Now race and real estate value are connected. And here we are.”

Decades of compounding damage

The damage compounded over decades. Crooks walked the audience through blockbusting, urban-renewal demolitions, highway construction through residential neighborhoods and what he called “planned shrinkage” — a budget strategy used by cities, including New York, in the 1970s that pulled services from redlined neighborhoods to preserve resources for green ones.

The first cut, he said, was fire departments. In parts of the South Bronx, Crooks said, nearly 80 percent of the built environment was lost within a decade.

The wealth effects persist, Crooks said. He cited data showing that, today, 80 percent of young first-time homebuyers receive family help with a down payment — a figure he connected to intergenerational wealth that accumulated or failed to accumulate along the lines redlining drew. Appraisal bias, he said, remains a documented present-day expression of the same logic.

“Still today, you have appraisal bias,” Crooks said. “These ideas get implemented in policy and are not completely debunked.”

What local associations can do now

The exhibit closes with examples of NAR, local associations and organizations working on fair housing, affordable housing and community reinvestment. Crooks said Designing the WE has localized the exhibit for specific communities and encouraged attendees to bring it to their own markets.